How Cheap Are Value Stocks?

Despite the strong recovery for value stocks since late 2020, they are still priced at historically cheap levels – comparable to their level at the peak of the tech bubble. That is especially true for small-value stocks.

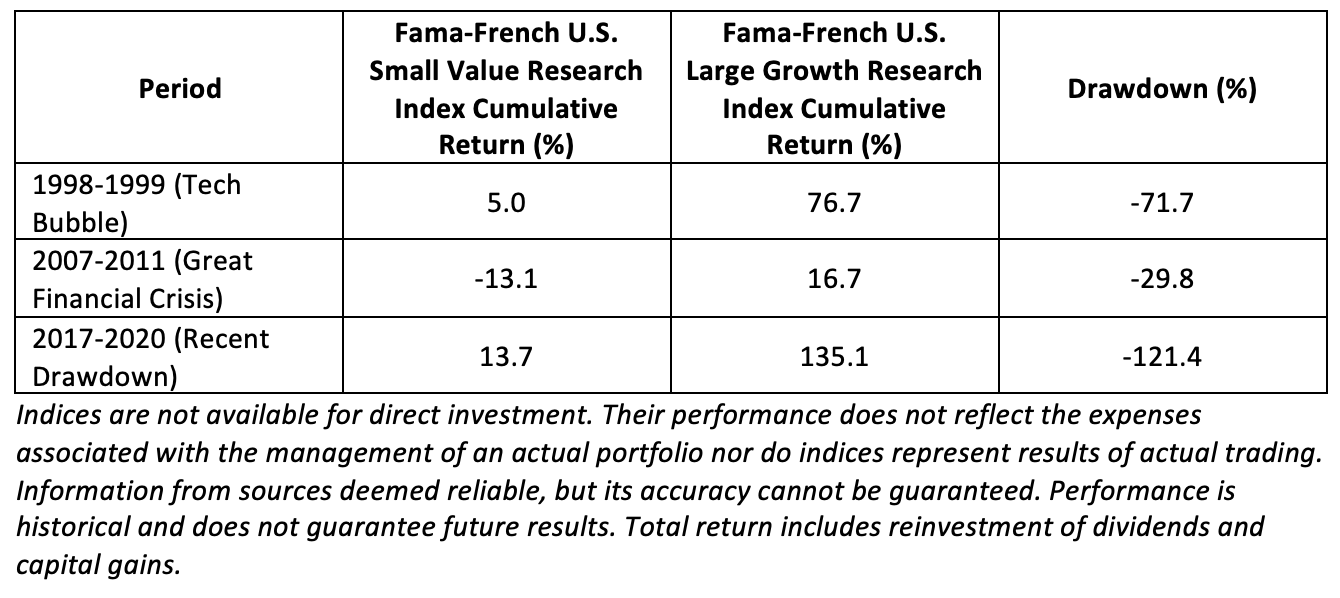

For the period 1927-2020, the Fama-French U.S. Small Value Research Index returned 13.9%, outperforming the Fama-French U.S. Large Growth Research Index, which returned 9.9%, by 4 percentage points a year. This outperformance led many investors to “tilt” their portfolios to small-value stocks (overweight them relative to their share of the total market). However, over the 23-year period 1998-2020, investors in U.S. small-value stocks have been disappointed, as the Fama-French U.S. Small Value Research Index slightly underperformed, returning 9.7% versus 9.9% for the Fama-French U.S. Large Growth Research Index. That disappointing performance was caused by three large drawdowns for small value relative to large growth, with the most recent drawdown being of historic proportions.

Small-value stocks began a dramatic recovery in late 2020. Using the last 12 months of available data (October 2020-September 2021), the Fama-French U.S. Small Value Research Index returned 87.9% versus the 27.1% return of the Fama-French U.S. Large Growth Research Index, an outperformance of 60.8 percentage points. Using live funds, we have access to more current data. Using Morningstar data, over the one-year period ending November 17, 2021, the Bridgeway Omni Small-Cap Value Fund (BOSVX) outperformed the iShares Russell 1000 Growth ETF (IWF) by 31.8 percentage points. However, despite that dramatic outperformance, BOSVX’s performance still trailed IWF’s over five- and 10-year periods by significant margins, 14.6 percentage points and 6.5 percentage points, respectively.

With that said, BOSVX’s valuation relative to the market indicates that small-value stocks are still trading at historically cheap levels – despite the fact that interest rates are much lower, and their earnings are growing faster as they recover from the cyclical lows caused by the pandemic.

Using Morningstar data, BOSVX had a P/E of just 9.3. At the end of 2013, before the expansion of the P/Es of growth stocks, BOSVX had a P/E of 11.0. Thus, small-value stocks are trading cheaper today than they were back in 2013, while the valuation of the market overall, and growth stocks in particular, have significantly increased. For example, in 2013 the S&P 500 earnings were about 105 and the index closed at 1782, a P/E of 17. The current full-year forecast for S&P 500 earnings is about 205. As of this writing, the S&P 500 was at about 4,700, producing a P/E of about 23. While BOSVX’s valuation has fallen 9%, the valuation of the S&P 500 has risen by 26%. As Adam Zaremba and Mehmet Umutlu, authors of the 2019 study, “Strategies Can Be Expensive Too! The Value Spread and Asset Allocation in Global Equity Markets,” demonstrated, the valuation spread provides information as to the future expected premium – the wider the spread, the larger the expected outperformance.

Valuation spreads at historic highs

Thanks to the research team at AQR, we can examine how the current spread between value and growth stocks compares to historical spreads. AQR’s hypothetical value composite includes five value measures: book-to-price, earnings-to-price, forecast earnings-to-price, sales-to-enterprise value and cash flow-to-enterprise value, and spreads are measured based on ratios. To achieve industry neutrality, their value spreads are constructed by comparing the value measures within each industry, which are then aggregated to represent an entire portfolio. AQR examined the current percentile ranking for large-cap stocks over the period 1984-October 2021 and found that in both the U.S. and emerging markets, value stocks were trading at the 100th percentile. In developed international markets, they were trading at the 99th percentile.

In other words, despite their strong recovery that began in late 2020, value stocks all around the globe are trading about as cheap as they have since 1984 relative to growth stocks.