Hold? Fold? Buy?

“Davidson” submits:

Fundamentals matter! Price trend investors dominate market thinking with widely accepted serious misperceptions. These misperceptions are even held by the most highly respected on Wall Street and who are often quoted in the media. One must look longer-term to locate the market’s fundamental underpinnings and separate out belief from reality to visualize investment opportunities.

Misperceptions are as broad as they are embedded. The data available today reveals a different reality than accepted wisdom.

1) Markets are believed to lead economic activity-In reality markets follow, they do not lead or predict economic activity

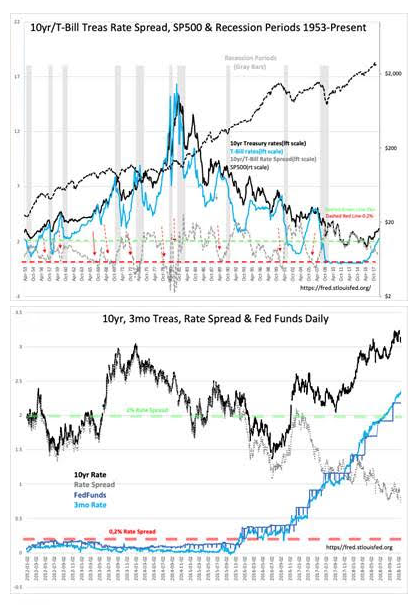

2) The Fed is believed to control rates and business cycles-In reality the Fed does not control rates, the Fed follows T-Bill rate shifts

3) A strong US$(US Dollar) is believed positive for US economic activity-In reality periods of US$ strength are detrimental to the US economy

4) The consensus is market cycles cannot be times-In reality market cycles can be anticipated with a fairly simple indicator

5) The consensus is that market cycles repeat in known patterns-In reality the factors behind market cycles never repeat.

6) The consensus long accepted is that investment sectors are correlated to previous economic trends-In reality every company is unique with only 3% of companies worth investment which can be simply identified. The R3000 produces ~100 names.

7) The consensus is that market prices are rational following a mathematical relationship to some fundamental measure -In reality market prices are short term psychological responses to anticipated events. There is no mathematical or algorithm solution possible for market analysis.

Knowing the differences between misperception and economic reality leaves one with the knowledge of when to hold them, when to fold them and when to buy some more. Fundamentals matter! The shift towards short-term investor market perception seeking results with less risk in shorter time-frames with computer algorithms has disconnected fundamentals from market prices. Investors have come to expect immediate price responses to anticipated fundamental reports. When the anticipated price response does not occur, literally within seconds, algorithms shift into the opposing response. Managing capital based on anticipated short-term market responses produces sharp movements which have often been opposite what one might deem logical. We have witnessed recent declines of 5%-10% within minutes of positive reports which did not receive an immediate positive price rise. The algorithms not registering an immediate positive price response to ‘Good News’, are programmed to treat a lack of positive response as ‘risk’ and initiate an immediate sell program to be the ‘early mover’. Only months afterwards, as it becomes evident that a particular positive report is one of a series of positive reports, do share prices rise in response to fundamentals. The opposite holds for negative reports which do not receive an immediate negative market response. Algorithms make markets appear illogical when in reality what we are witnessing are price shifts caused by short-term trader perception vs. pricing impact from longer-term investor perception to a series of fundamental reports.

We tend to think of markets as cohesive and logical. Every blip seems to find someone providing a logical explanation behind each. In reality, what we see is an interplay of short-term vs. long-term perception, some believing in mathematical models while others invest using broad themes. Each influences prices using different contexts. It is very confusing! One needs to identify key measures on which markets operate to be successful over the long-term.

Even with every market cycle having unique drivers, the best overall market cycle indicator over time is theT-Bill/10yr Treasury Rate Spread(see charts monthly and daily). This indicator is both an indicator of lending activity and a good market psychology measure. The wider the spread, the wider the net interest margins and the propensity to lend to businesses and individuals. As long as financial institutions are open to lending, economic activity expands. Even loans which prove to be underperforming can be refinanced to avoid default with the belief that given enough time they will be repaid in full. Default becomes an issue when the T-Bill/10yr Treasury Rate Spread narrows to 0.2% or less. When the spread narrows to this level, lending profits no longer justify additional credit extension and defaults suddenly rise and an economic correction ensues.

The T-Bill/10yr Treasury Rate Spread can also be viewed an indicator of market psychology. The wider the spread, the greater the economic and market pessimism. The historical range vs economic and market cycles from 1953 is 0.2% and less – 2% and higher. Equity markets are lowest when investors are most pessimistic and T-Bill/10yr Treasury Rate Spread is the widest. Equity markets peak 12mos-18mos after the T-Bill/10yr Treasury Rate Spread falls below 0,2% as lending stalls and defaults rise. The reason behind the T-Bill/10yr Treasury Rate Spread falling below 0.2% is investor euphoria shifting funds into equities seeing higher returns. This pattern occurs every cycle as John Templeton said, “Bull markets are born on pessimism, grown on skepticism, mature on optimism, and die on euphoria.” The current level is 0.75% or just under mid-range.

The questions we need to answer multiple times in every market cycle is, “When to hold them?”, “When to fold them?” and “When to buy some more?” The answer based on the fundamentals of the T-Bill/10yr Treasury Rate Spread is now is the time to “Buy more!” As to what specifically to buy and avoid requires discussion and balancing one’s decisions to one’s individual circumstance. There is no investment mix which can fits every investor. I do not favor ETFs or Financial Planning which are based on a form of ‘group think’ and have their basis in mathematical models.

Disclosure: The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or ...

more