Here’s My Top 4 US Dividend Growth Stocks For 2016

At the end of 2014, I claimed I was bullish for 2015. It has been a tougher year than anticipated, mainly due to the China stock market crisis. Between June 12th and August 25th, the Shanghai 180 lost 43.4%.

The North American markets usually don’t follow the Asian ones but this time, the panic wave hit all markets. Fortunately, we all went back to earth with the quarterly earnings in October. The US stock market recuperated all losses and as of the end of November (the time where I wrote this), the S&P 500 was back in positive territories year to date. We experienced a similar situation to October 2014 where the market was back on solid ground after a few month of higher volatility.

However, results weren’t that impressive in Q3 and the stock market didn’t post double digit returns for 2015. On the other side, the economy is going on the right side. As the unemployment rate was around 6% last year, we are now down to 5%. Job creation stats are on a uptrend and new construction is well over a million (annualized) now. Even better, we even started to see some core inflation rising (inflation without food and gas price included). Latest core inflation report in November shows a 2% increase. The FED is now expected to raise its interest rate in December, 6 months after what we expected a year ago. This is to show you how fast things evolve and how they are unpredictable. This news was positively accepted by the markets as it is a clear sign that the US economy is going toward the right direction.

2015 was punctuated by currency headwinds hurting many companies’ revenues. Global economy slowdown didn’t help sales growth either. Finally, we all expected the American consumers to benefit from a drop in the gas price to spend more. This is what history tells us about oil price going down; consumer spending is going up. Once again, we had a great proof that past events don’t guarantee the future as consumers decided to pay off their debts instead of buying a new Ford and going on vacation to Disney World.

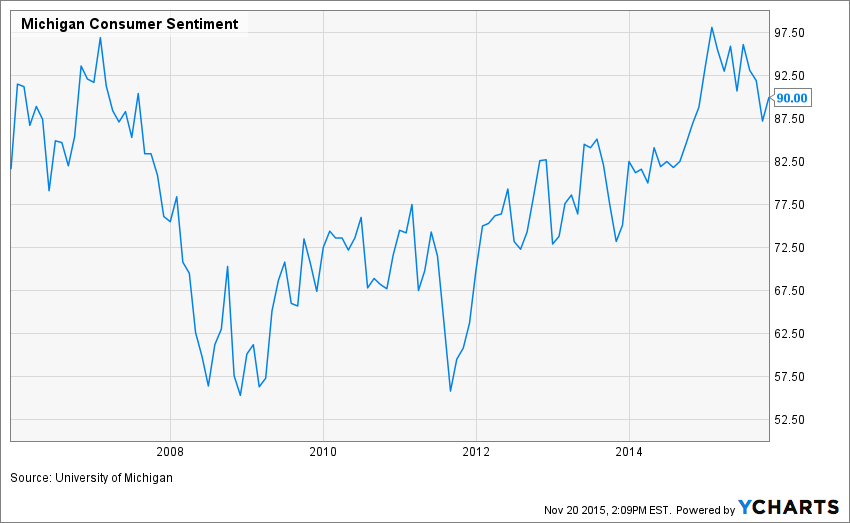

Fortunately, the wind is starting to turn again as consumers spend more and gain in confidence. In fact, we have reached in 2015 a 10 year highest level of consumer sentiment:

Looking forward, I believe 2016 will be a positive one on the US stock market. The US economy will continue to support the world’s economy and Canadians should escape their short recession by selling more to the US. Consumer spending will rise again and will lead to stronger local sales. I am bullish for the US stock market for 2016.

In order to benefit from this bullish market, I’ve identified four dividend growth stocks that should have a good year:

Union Pacific Corporation (UNP)

WHAT IT MAKES IT A GOOD COMPANY

Union Pacific is a transportation company focus in railroads. It’s Union Pacific Railroad covers 23 states across the western 2/3 of the USA. UNP shows a great diversification in term of sectors: 10% for Automotive, 17% Agricultural products, 17% Chemicals, 20% Intermodal, 19% Industrial products and 17% Coal.

INVESTMENT THESIS

The reason to purchase UNP today is simple; go past the short-sight challenging environment and look at the big picture. Low oil price will only last so long and truckers industry will not stay as fierce competitors over the long run. In the meantime, management teams is doing a fabulous work to continue improving the company productivity with longer and faster trains along with controlling costs. This is a strong dividend payer with a relatively good yield (2.50%).

POTENTIAL RISK

There are many risks that may affect UNP price in 2016. First, the low price of fuel put back truckers on the competitors map. Second coal commodity doesn’t have the spot light at the moment and suffer from the overall cheap energy commodities environment. Third, it was a bad year for intermodal sectors as the fracking industry slowed down drastically, following the oil price. However, it will be a strong holding for the future.

COMPANY METRICS

| Dividend Yield | 2.79% | P/E Ratio | 13.61 |

| 5yr Div Growth | 24.57% | ROE | 24.13% |

| Payout Ratio | 45.67% | 1yr Sales Growth | 9.22% |

| 5yr EPS Growth | 25.14% | 5yr Sales Growth | 11.15% |

COMPANY VALUATION

| Calculated Intrinsic Value OUTPUT 15-Cell Matrix | |||

| Discount Rate (Horizontal) | |||

| Margin of Safety | 8.00% | 9.00% | 10.00% |

| 20% Premium | $258.17 | $129.56 | $86.67 |

| 10% Premium | $236.66 | $118.76 | $79.45 |

| Intrinsic Value | $215.15 | $107.97 | $72.22 |

| 10% Discount | $193.63 | $97.17 | $65.00 |

| 20% Discount | $172.12 | $86.37 | $57.78 |

Microsoft (MSFT)

![]()

WHAT IT MAKES IT A GOOD COMPANY

Microsoft is a regular on this list. Microsoft is the best known and most important software company in the world. Along with its famous line of software products, Microsoft also offers various services such as servers (including cloud systems), business solutions (support and consulting), entertainment (Xbox) and other online services.

INVESTMENT THESIS

Microsoft finds another niche to dominate; here’s why the cloud business will push this giant higher. We all know the strength of Microsoft lies with all businesses using their services (Windows, Office series but also servers and business services). Since the cloud is the next big thing for most companies, Microsoft can expect huge growth from this segment in the future. Plus, this relatively new niche is a perfect complement for MSFT current business.

POTENTIAL RISK

A few years ago, I wasn’t as confident in Microsoft’s future; the Xbox wasn’t doing that well, BING seemed like just another Yahoo! trying to compete with Google and Windows’ sales weren’t impressive. However, a few years later, BING generates revenues, Xbox is a strong player in the gaming industry and cloud services came out of nowhere with great growth potential. I guess this summarizes the risk you face while investing in a techno stock. This tells you how fast things evolves in the techno sector!

COMPANY METRICS

| Dividend Yield | 2.32% | P/E Ratio | 37.27 |

| 5yr Div Growth | 16.64% | ROE | 14.28% |

| Payout Ratio | 81.89% | 1yr Sales Growth | 7.77% |

| 5yr EPS Growth | -6.90% | 5yr Sales Growth | 8.41% |

COMPANY VALUATION

| Calculated Intrinsic Value OUTPUT 15-Cell Matrix | |||

| Discount Rate (Horizontal) | |||

| Margin of Safety | 9.00% | 10.00% | 11.00% |

| 20% Premium | $119.46 | $78.91 | $58.67 |

| 10% Premium | $109.51 | $72.34 | $53.78 |

| Intrinsic Value | $99.55 | $65.76 | $48.89 |

| 10% Discount | $89.60 | $59.18 | $44.00 |

| 20% Discount | $79.64 | $52.61 | $39.11 |

Autoliv (ALV)

WHAT IT MAKES IT A GOOD COMPANY

Autoliv is a designer and manufacturer of safety products for the automobile industry. Their product offering includes air bags, seatbelts, steering wheels, passive safety electronics and active safety systems such as radar, night vision and cameras. ALV owns 7% of all automotive patents for its side-impact air bags. The company spends around 6% of its sales on research and development to stay ahead of their competition.

INVESTMENT THESIS

ALV had to suspend its dividend in 2009 due to the car industry crisis. Since then, the dividend payment has grown by 58% CAGR from 2010 to 2015. The idea of investing in Autoliv is to select a company that is in the right place at the right time with the car industry growing and the demand for additional safety. If car makers want to reach 4 and 5 star safety ratings, they will need Autoliv products to achieve their goal. The company has seen double digit growth in many countries such as Europe, Japan and the rest of Asia.

POTENTIAL RISK

An important risk associated with this company is that ALV doesn’t have any incredible competitive advantage. It is true they invest massively in R&D and the benefit of a good reputation. However, the company continuously faces fierce competition where car makers request volume discounts and reduced prices for product agreements.

COMPANY METRICS

| Dividend Yield | 1.75% | P/E Ratio | 26.85 |

| 5yr Div Growth | 62.01% | ROE | 12.39% |

| Payout Ratio | 46.41% | 1yr Sales Growth | 4.97% |

| 5yr EPS Growth | 111.51% | 5yr Sales Growth | 12.53% |

COMPANY VALUATION

| Calculated Intrinsic Value OUTPUT 15-Cell Matrix | |||

| Discount Rate (Horizontal) | |||

| Margin of Safety | 9.00% | 10.00% | 11.00% |

| 20% Premium | $82.94 | $65.97 | $54.68 |

| 10% Premium | $76.03 | $60.47 | $50.12 |

| Intrinsic Value | $69.12 | $54.98 | $45.57 |

| 10% Discount | $62.21 | $49.48 | $41.01 |

| 20% Discount | $55.30 | $43.98 | $36.45 |

Lockheed Martin (LMT)

WHAT IT MAKES IT A GOOD COMPANY

Lockheed Martin (LMT) is the world’s largest defense contractor earning 61% of its sales from the US Department of Defense, 21% from other US government agencies and 18% from international clients. Heavy regulation, years of symbiosis with the US Defense and their know-how are three key elements protecting most of LMT’s business. Let’s just say you can’t start building military aircraft and missiles in your basement to compete with this defense behemoth.

INVESTMENT THESIS

With terrorists’ treats growing in importance, we can expect LMT to share its expertise in defence across the planet. This could be a very good way for LMT to diversify its source of income. The acquisition of Sikorsky helicopter operations will also add more growth perspective in the future. The company’s leadership in the defense sector will play a very important role in the upcoming years as several treats are rising.

POTENTIAL RISK

LMT has always been dependent of the US Government budget for defense. It has been discussed at several occasions that those expenses have to be cut. Hence, LMT suffers directly from such events.

COMPANY METRICS

| Dividend Yield | 2.81% | P/E Ratio | 19.39 |

| 5yr Div Growth | 14.15% | ROE | 103.42% |

| Payout Ratio | 53.16% | 1yr Sales Growth | 0.53% |

| 5yr EPS Growth | 7.74% | 5yr Sales Growth | 0.72% |

COMPANY VALUATION

| Calculated Intrinsic Value OUTPUT 15-Cell Matrix | |||

| Discount Rate (Horizontal) | |||

| Margin of Safety | 9.00% | 10.00% | 11.00% |

| 20% Premium | $311.09 | $245.52 | $201.99 |

| 10% Premium | $285.16 | $225.06 | $185.16 |

| Intrinsic Value | $259.24 | $204.60 | $168.32 |

| 10% Discount | $233.32 | $184.14 | $151.49 |

| 20% Discount | $207.39 | $163.68 | $134.66 |

None.

Some good picks here, I am not sure I share the same opinion about 2016 being a good year considering what is happening to oil prices, China's decline, and global industrial slowdown. Any thoughts on telecommunications and tobacco as dividend picks? These 2 areas famous for high dividends. Examples include: Vodaphone (5.3%), AT & T (5.7%), Altria Group (3.8%), and Philip Morris (4.7%)

Great picks, I happen to be looking at these myself.