US equity futures reversed an earlier loss and traded at session highs even as bonds around the world fell, briefly sending the 10Y Treasury to 4.04% and JGBs to 0.57%, well above the previous 0.5% cap and the highest since 2014, after the Bank of Japan - the only major central bank not to have begun reversing ultra-easy monetary policy - surprised investors by tweaking its control of market rates, in a market test to how far it can go without explicitly starting normalization. But in the end, the tweak ended up being less hawkish than some feared and as a result, futures are now reversing much of yesterday's sharpo losses.

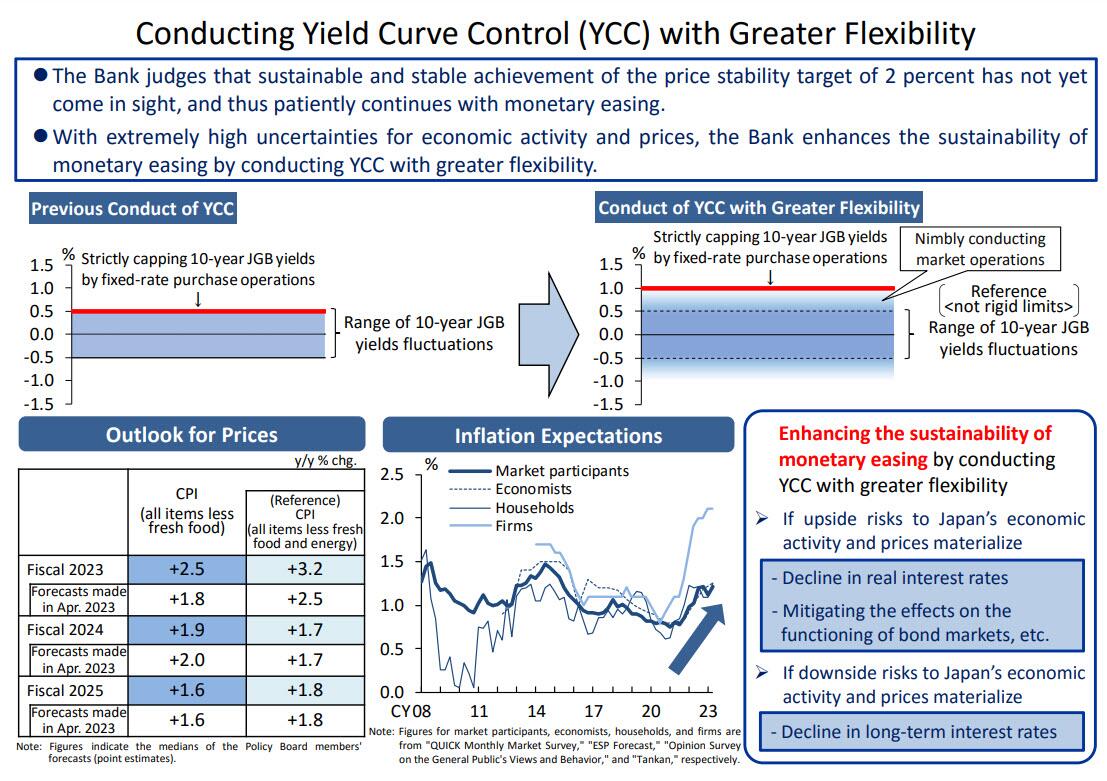

Having previously capped bond yields at 0.5% in a bid to stoke borrowing and its economy, the central bank said today it now regarded that level as a reference point rather than a rigid limit, and instead of intervening to keep rates capped at 0.5% it would only do so firmly at 1.0%, while deciding whether and where to intervene in the 0.5% to 1.0% band (the BOJ graphic explaining the change is below).

(Click on image to enlarge)

The BOJ pledged to show more flexibility over its yield curve control policy, though governor Kazuo Ueda insisted the bank was still far from the point where it could raise rates, and by then global deflation will have returned anyway.

In stock markets, the busiest week in the earnings calendar was drawing to a close, with sentiment supported by forecast-beating results and conviction that interest rates in the US and euro zone are near their peak. As of 7:30am ET, S&P futures traded 0.5% higher, reversing some of yesterday dump which was sparked, ironically, by a planted story in the Nikkei previewing the BOJ's action, which however turned out to be less hawkish than expected, and thus the equity market overreacted on Thursday, and rebounded today as 10Y yields traded down to 3.96% after rising as high as 4.04%

(Click on image to enlarge)

In premarket trading, Enphase Energy shares plunged 15% after the solar-equipment manufacturer reported second-quarter revenue that missed estimates. Analysts found the results to be disappointing, and noted that the third-quarter revenue outlook also failed to meet expectations. On the other end, First Solar shares jumped as much as 9% after the solar technology company results beat estimates and announced plans for a new manufacturing facility in the US, which analysts took as a sign of confidence in demand. Brokers also highlighted strong bookings and average selling prices. Here are some other notable premarket mover:

Ford shares drop 2% after the automaker said it now expects to see losses from electric vehicles hit $4.5 billion this year. While Ford’s other segments performed well, Morgan Stanley sees major changes to the EV strategy possibly being necessary.

- Homology Medicines shares surge 17% after the biotech said it will evaluate strategic alternatives and cut 87% of its workforce, citing the current financing environment and Homology’s anticipated clinical development timelines. RBC said that the decision to preserve cash was “pragmatic.”

- Intel shares are rise as much as 8% in premarket trading on Friday after the chipmaker reported second-quarter results that beat expectations as its PC business was starting to recover. The company’s CEO says Intel remains on track to meet its of target of regaining manufacturing leadership by 2025.

- Roku shares rise nearly 10% after the streaming-video platform company reported second-quarter revenue that was much stronger than expected. While analysts were positive about the results, they warned that Hollywood strikes would turn into a headwind if they prolong.

- Solar stocks fell in US premarket trading after Enphase Energy reported second-quarter revenue that missed the average analyst estimate, and gave lower-than-anticipated third-quarter revenue guidance.

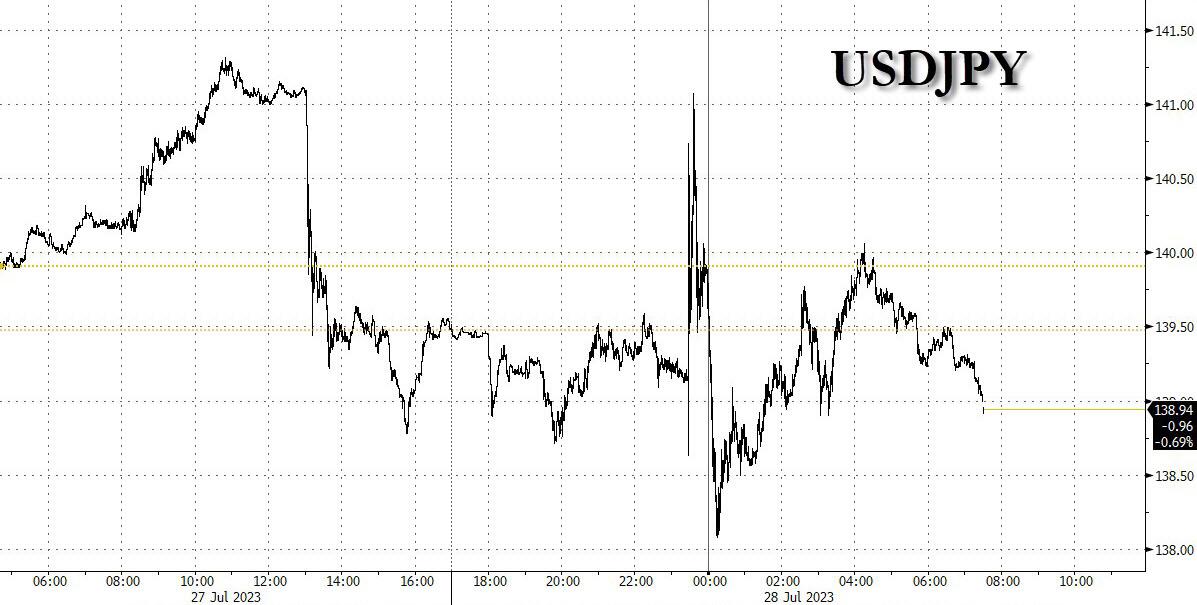

The BOJ move also sparked speculation it marked the first step towards the end of extraordinary stimulus after the recent surge in inflation. It also triggered big swings in the yen, sending it as much as 1% lower and higher at one point against the dollar, before trading largely unchanged compared to the pre-BOJ announcement. Despite the rollercoaster move, the yen was still headed for its best month since March, with gains of almost 3.5%.

(Click on image to enlarge)

“The BOJ decision is an invitation to short dollar-yen,” said Kenneth Broux, currency strategist at Societe Generale SA. “Higher Japanese yields reduce the spread versus US Treasuries and German bunds.” He added however that dollar downside could be limited, given Thursday’s strong US data that could imply further Fed tightening; furthermore sticky rate differentials mean that those who are stuck in a short USDJPY will suffer brutal bleeding thanks to the 5.50% difference between the BOJ and the Fed, a difference which will remain for a long time.

Markets elsewhere reacted to the possibility that higher yields at home will persuade Japanese investors, who own sizable amounts of US, European and Australian bonds, to reduce overseas debt holdings. As noted above, US Treasury yields rocked as high as 4.04% - first after a Nikkei news report that Japan was poised to tweak its yield-curve control policy, and then after the BOJ indeed tweaked it - but then yields dipped back down to 3.96% after markets digested the announcement realizing that it is not as hawkish as some had feared.

(Click on image to enlarge)

Elsewhere, the German 10Y Bund increased as much as 5 basis points, and Australia’s climbed 20 basis points at one point.

"This is a big week as it signals we are pretty much at the end of hiking cycles globally,” said Peter Kinsella, head of currency strategy at asset manager Union Bancaire Privee UBP SA. The “BOJ is effectively saying the top of the yield range is now 1% so that implies 50 basis points in potential steepening. So it’s slow gradual normalization, but yes, it’s normalization BOJ style,” he added.

European stocks are in the red with technology leading declines while banks rise. While the Stoxx 600 is down 0.3%, European bourses were still set for their third straight weekly gain. Here are the most notable European movers:

- AstraZeneca gains as much as 4.8% after reporting second-quarter sales and profit that beat estimates and announcing the $1 billion acquisition of a portfolio of rare disease gene therapies from Pfizer

- Hermes shares jumped as much as 4.3% after the French luxury group outperformed its rivals during the second quarter with unabated demand for its high-end purses, notably in the US and China

- Standard Chartered shares rise as much as 6.7% in London, the most since March, after the bank reported better-than-expected pretax profit for the second quarter

- Eni shares rise as much as 1.8% after the Italian oil and gas giant’s second-quarter profit beat consensus estimates, with the analysts flagging a strong performance at its Global Gas & Lng Portfolio (GGP) unit

- Euronext shares jump as much as 7.1%, most since March, after the exchange operator reported revenue for the second quarter that beat the average analyst estimate and announced a €200m buyback

- Ams-OSRAM shares rally as much as 19%, their biggest one-day climb since 2020. The company says it will exit non-core and lower-performing semiconductor businesses, a move that analysts say will help facilitate a turnaround and its debt refinancing

- Sanofi falls as much as 4.1%, the most since May 30, after the French drugmaker reported its latest earnings, which analysts say is a mixed bag, as overall sales missed slightly and growth for its key drug Dupixent only arrived in line

- Air France-KLM shares fall as much as 6% after analysts noted headwinds including elusive profit guidance and a higher unit-cost forecast, even as the company posted a strong 2Q operating income beat

- Signify shares fell as much as 5.1%, the biggest drop since May 18, after the lighting maker cut its adjusted Ebita margin forecast for the full year and reported revenue for the second quarter that missed the average analyst estimate

- Atos shares sink as much as 20% after the French IT firm recorded a negative free cash flow of €969m in the first half, a figure that is well below analyst estimates and is about three quarters of the stock’s market value

- Vanquis Banking shares slumped as much as 29% to their lowest level in over 30 years, after the specialist lender reported a loss and a decrease in its net interest margin

- Evotec falls as much as 11%, the most since November, after the German biotech cut its full-year forecast as the effects from the cyberattack earlier this year continues to impact the firm’s earnings

Earlier in the session, Asia’s equity benchmark held steady as a rally in Chinese stocks was offset by losses in Japan, where the central bank jolted markets by loosening its grip on bond yields. The MSCI Asia Pacific Index was little changed on Friday, but headed for a 2% weekly gain as Chinese shares extended this week’s rally on emerging signs that Beijing is acting on its policy pledges. Meanwhile, the Nikkei 225 slid as much as 2.6%, the worst performance in Asia, on concern the Bank of Japan’s adjustment paves the way for a stronger currency, potentially hurting exporters, however the Nikkei eventually rallied sharply, closing down just 0.4% led by Japan's lenders who rallied on optimism their profitability will improve.

(Click on image to enlarge)

Regional stocks have climbed this week on hopes of stimulus measures in China following the Politburo meeting. A gauge of the nation’s equities listed in Hong Kong jumped as much as 1.7% on Friday after regulators were said to have signaled additional support for the technology sector and on speculation that authorities may lower stamp duties to bolster trading. Tencent and Meituan were among the top positive contributors in the MSCI Asia gauge, while Japan’s Sony and Toyota Motor were among the biggest drags.

Asia’s stock benchmark climbed for a fourth straight day on Thursday after the US central bank raised interest rates to a 22-year high and said further tightening would be data dependent. The gauge is approaching this year’s high seen in January though its gain of 9% so far in 2023 compares poorly with the S&P 500 Index’s 18% advance. Optimism over earnings, gains in China and rising speculation that the Federal Reserve is nearing the end of its policy tightening have boosted sentiment toward Asia’s emerging-market equities in recent weeks.

The MSCI Asia gauge is on track for a second straight month of gains, with its 3.7% rally in July set to be the best since January. An index of Southeast Asian stocks has jumped close to 6% this month, heading for the best performance since November. “There is enormous potential for emerging-market equities to play catch up on emerging market debt in a world where the Fed stops tightening and the dollar weakens,” Christopher Wood, global head of equity strategy at Jefferies, wrote in a note.

Australia's ASX 200 was pressured amid weakness in the property sector and miners, with sentiment also not helped by the surprise contraction in Retail Sales

The record-breaking India stock market ended the week among the worst performing markets in the region as sentiment was hit by weaker-than-expected earnings from some index heavyweights. The S&P BSE Sensex fell 0.2% on Friday to 66,160.20 in Mumbai, while the NSE Nifty 50 Index was little changed at 19,646.05. The MSCI Asia Pacific Index was up 0.5% for the day. For the week, benchmark indexes lost 0.8% as compared to the regional benchmark’s 2.6% gains. Indian equities underperformed their peers in China, Hong Kong and Taiwan. The losses in the benchmarks during the week were limited by continued net buying of stocks by global funds, who look set to mark their fifth consecutive month of net purchases in July. Global funds have net bought over $19 billion since end of February. HDFC Bank contributed the most to the Sensex’s decline, decreasing 1.7%. Out of 31 shares in the Sensex index, 15 rose and 15 fell, while 1 was unchanged

In FX, the Bloomberg Dollar Spot Index slipped, while Treasury yields fell led by the short-end of the curve. USD/JPY fell more than 1% after the BOJ decision before gaining by a similar amount. It was down 0.1% at 139.30 at 10:30 a.m. London. Dollar sell-stops are building below 137.25, the July 14 low and buy stops above 142, according to Asia-based FX traders. European short-end bonds gained following dovish comments by ECB policymakers; Money markets ease ECB tightening wagers for a second day.

In rates, treasuries held gains in early US trading, led by the short end, steepening the curve. Curves are steeper globally led by UK and Japan, where 10-year yields jumped to highest level in nearly a decade after BOJ effectively adopted a higher target, a move previewed during US trading hours Thursday. US yields lower across the curve by as much as 5bp-6bp at short end with long end little changed; however 30-year earlier climbed to within 0.1bp of its July 10 YTD high 4.082%.

Yields remain higher on the week with the curve steeper, as focus began shifting from Fed policy stance — which Chair Powell this week said was evenhanded with respect to another interest-rate hike in September — to strong economic growth indicators and expectations that Treasury auction size increases will be announced next week for the August-to-October financing period. Also ahead next week, month-end Treasury index rebalancing is projected to extend its duration by 0.07 year, and first major economic indicators for July including ISM manufacturing and services gauges and employment report are slated.

In commodities, crude futures decline with WTi falling 0.3%. Spot gold adds 0.2%.

Bitcoin prices are relatively stable just above the USD 29,000 level.

To the day ahead now, and data releases from the US include the Q2 employment cost index, June’s PCE inflation, personal income and personal spending, and the final University of Michigan consumer sentiment index for July. Over in Europe, we’ll get the French and German CPI readings for July. Central bank speakers include the ECB’s Simkus. Finally, earnings releases include Exxon Mobil and Procter & Gamble.

Market Snapshot

- S&P 500 futures up 0.3% to 4,578.25

- MXAP up 0.3% to 169.86

- MXAPJ up 0.1% to 536.74

- Nikkei down 0.4% to 32,759.23

- Topix down 0.2% to 2,290.61

- Hang Seng Index up 1.4% to 19,916.56

- Shanghai Composite up 1.8% to 3,275.93

- Sensex down 0.5% to 65,953.22

- Australia S&P/ASX 200 down 0.7% to 7,403.65

- Kospi up 0.2% to 2,608.32

- STOXX Europe 600 down 0.4% to 470.02

- German 10Y yield little changed at 2.52%

- Euro down 0.1% to $1.0963

- Brent Futures down 0.2% to $84.03/bbl

- Gold spot up 0.2% to $1,949.96

- U.S. Dollar Index up 0.12% to 101.90

Top Overnight News from Bloomberg

- China’s markets regulator has consulted securities firms for possible measures to boost stocks amid growing signs Beijing is seeking to restore investor confidence, people familiar with the matter said. BBG

- China has asked its largest technology companies to provide case studies of their most successful startup investments in consumer, telecom and media companies, a sign authorities are ready to grant them broader leeway in backing such deals after a crackdown brought them to a virtual halt two years ago. BBG

- The White House has decided it will bar Hong Kong’s top government official from attending a major economic summit in the United States this fall, according to three U.S. officials familiar with the matter, in the latest test of President Biden’s bid to reset relations with China. Washington Post

- The Tokyo CPI for Jul overshoots the Street, with core (ex-food/energy) coming in at +4% Y/Y (up from +3.8% in June and ahead of the Street’s +3.7% forecast). RTRS

- The BOJ surprised markets by loosening its grip on bond yields. It kept the target for 10-year yields at around 0% but said its 0.5% ceiling was now a reference point — not a rigid limit. It will manage the curve "flexibly" and buy benchmark bonds at 1% every business day, effectively capping it at that level. BBG

- Donald Trump has been accused of attempting to have surveillance video footage at his Mar-a-Lago estate deleted ahead of an FBI search, as federal prosecutors added more criminal counts to a case over the former US president’s handling of classified documents. FT

- Office space set to shrink for the first time on record – the lack of new supply coupled with existing buildings being repurposed or destroyed means the total square footage available to be used as office space will shrink this year for the first time on record. BBG

- Tech investment giant Sequoia Capital pared back the size of two major venture funds, part of a dramatic downsizing the venture firm is undertaking amid a startup downturn. WSJ

- Facebook removed content related to Covid-19 in response to pressure from the Biden administration, including posts claiming the virus was man-made, according to internal company communications viewed by The Wall Street Journal. WSJ

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed with the region cautious as all attention was on the BoJ policy decision in which the central bank kept monetary policy settings unchanged but announced to guide YCC more flexibly with fixed rate operations for 10yr JGB to be conducted at 1.0% (prev. 50bps). ASX 200 was pressured amid weakness in the property sector and miners, with sentiment also not helped by the surprise contraction in Retail Sales. Nikkei 225 underperformed with yields higher and markets spooked by the latest BoJ developments. Hang Seng and Shanghai Comp shrugged off early weakness and gained after further calls and efforts for China to support the housing market and tech industry. US equity futures were rangebound overnight although slumped during US trade as markets faltered stateside following source reporting by the Nikkei on the BoJ. European equity futures are indicative of a lower open with the Euro Stoxx 50 -0.4% after the cash market closed up by 2.3% yesterday.

Top Asian News

- Chinese market watchdog has reportedly asked brokers for advice to boost stocks, according to Bloomberg; brokers reportedly proposed stamp duty reduction.

- Italian PM Meloni said she plans to go to China in one of her next diplomatic missions and the decision on leaving China's Belt and Road Initiative will be made by December.

- China reportedly urges improved mortgage rules to support the housing market, while it also asked tech giants to showcase investments in a sign of easing, according to Bloomberg.

- US is to ban Hong Kong Chief Executive Lee from the APEC Economic Summit, according to Washington Post.

European equities are a mixed bag as the dust settles on yesterday’s ECB announcement and the overnight BoJ release. The Stoxx 600 index is on track to close the week out with gains over just over 1% with discrepancies between regional bourses stemming from various heavyweight earnings releases. Equity sectors in Europe have a negative tilt with Tech, Real Estate and Travel & Leisure names lagging peers. US equity futures are trading on the front foot, as positivity seemingly returns following a sell-off in stocks yesterday, after a slew of hot data prints ahead of today's top-tier data.

Top European News

- ECB's Simkus says the choice for September is between 25bps hike and unchanged rate; rate cut unlikely in H1'24; would not call a situation a recession, it is more a soft landing scenario, according to Reuters.

- ECB's Villeroy says French data showing inflation is falling without a recession; Pragmatism also needed as decisions at upcoming rate meetings will be open and entirely data drivenPerseverance is now the prime key virtue given the time needed for full transmission of monetary policy. Our growing confidence in the fall in inflation towards 2% is based on the good transmission of monetary policy, according to Reuters.

- ECB's Kazimir says ECB is nearing the completion of policy tightening; he is still waiting for an answer for what is coming in September; says ECB's mission is still not fulfilled and "we should take firm step further". He noted if ECB was to take a break in September, it would be premature to consider it the end, and added the ECB looking for the right place to stay for a large part of next year, according to Reuters.

- ECB Survey of Professional Forecasters (SBF): expectations for headline HICP inflation were broadly unchanged compared to the previous survey

FX

- XY briefly topped 102.00 earlier in the European morning. Dollar paused for breath after Thursday’s sharp rebound on bullish US data and Euro depreciation on the back of a dovish ECB hike, but retained a firm underlying bid.

- The Buck faced strong competition from the Yen following the BoJ’s hawkish "surprise" as this hammered USD/JPY down to within single digit pips of 138.00 at one stage from 141.05

- Antipodeans lag with the Aussie underperforming as Australian Retail Sales were downwardly revised, while market pricing was already tilting heavily in favour of no change in rates from the RBA next week.

Fixed Income

- Debt futures have settled down following several bouts of fast market moves and high volatility amidst somewhat mixed data and further reaction to or reflection on Central Bank meetings that threw several surprises.

- Bunds and Gilts have regained poise within wider 132.96-81 and 95.62-11 respective ranges, while OATs and Bonos lag in wake of French and Spain inflation data.

- The T-note remains above parity between 110-10+/110-25+ parameters in consolidative trade after yesterday’s mostly stellar US macro releases and turning attention to another busy agenda to end a hectic week.

Commodities

- WTI and Brent front-month futures continue with the choppy but horizontal performance seen overnight with prices moving in tandem with the broader risk sentiment. Complex-specific newsflow has been light this morning aside from the release of overall mixed GDP from various EZ nations.

- Spot gold was dragged back under its 100 DMA (USD 1,966.76/oz) to levels near USD 1,950/oz yesterday following the hot US economic data, with prices today meandering around the half-round figure and on both sides of the 50 DMA and 21 DMA.

- Base metals meanwhile are mostly firmer despite the stronger Dollar amid continued tailwinds from Chinese stimulus.

Geopolitics

- Russia prevented a Ukrainian drone attack on targets in Moscow, according to RIA citing the Defence Ministry.

- US President Biden and Italian PM Meloni's joint statement said the US and Italy will continue to provide political, military, financial and humanitarian assistance to Ukraine for as long as it takes. US and Italy are firmly committed to a free, open, prosperous, inclusive and secure Indo-Pacific, while they reiterated the vital importance of maintaining peace and stability across the Taiwan Strait. Furthermore, they commit to strengthening the bilateral and multilateral consultation on the opportunities and challenges posed by China.

- US is expected to announce a weapons package for Taiwan worth more than USD 300mln, according to US officials cited by Reuters.

- North Korea staged a military parade in celebration of the 70th anniversary of the end of the Korean War, while the Chinese delegation attended the parade and North Korea displayed an ICBM at the parade, according to KCNA.

- North Korean leader Kim had a formal lunch with Russian Defence Minister Shoigu and exchanged views on the political situation around the Korean peninsula, as well as discussed issues to advance strategic cooperation on military and security. Furthermore, North Korea said it will fight on the side of countries challenging US hegemony, according to KCNA.

- Russian President Putin said North Korea's support for the military operation against Ukraine emboldens the two countries' determination to cope with Western organisations, according to KCNA.

- Russia's Putin says we will discuss peace plan today, according ot Reuters.

- China declares a large no-sail zone in the South China Sea for military exercises from July 29 to August 2nd, according to a journalist on Twitter.

US Event Calendar

- 08:30: June PCE Deflator MoM, est. 0.2%, prior 0.1%

- June PCE Core Deflator MoM, est. 0.2%, prior 0.3%

- June PCE Core Deflator YoY, est. 4.2%, prior 4.6%

- June PCE Deflator YoY, est. 3.0%, prior 3.8%

- June Personal Income, est. 0.5%, prior 0.4%

- June Personal Spending, est. 0.4%, prior 0.1%

- June Real Personal Spending, est. 0.3%, prior 0%

- 10:00: July U. of Mich. Sentiment, est. 72.6, prior 72.6

- July U. of Mich. Current Conditions, prior 77.5

- July U. of Mich. Expectations, prior 69.4

- July U. of Mich. 5-10 Yr Inflation, est. 3.0%, prior 3.1%

- July U. of Mich. 1 Yr Inflation, prior 3.4%

- 11:00: July Kansas City Fed Services Activ, prior 14

DB's Jim Reid concludes the overnight wrap

It was originally another great day for the fictitious soft-landing ETF yesterday until markets started to break down around 6pm London time last night after a softish 7-year Treasury auction and more importantly, a report from Nikkei suggesting the BoJ would discuss tweaks to YCC at this morning's meeting, something they've followed through on as we'll see immediately below. This turned an +8bps sell-off in 10yr US yields into a +13.1bps one by the close and turned the S&P 500 from a +0.7% gain to a -0.64% loss, with the NASDAQ moving from c.+1.3% to -0.22% over the same 3 hour late session period. It all overshadowed a relatively dovish ECB meeting, within the context of the expected +25bps hike, afterwhich European yields moved notably lower for the day (e.g. 2yr bunds -5.1bps).

So the last international hold out on ultra low yields has turned with the BoJ tweaking it's YCC policy in the last couple of hours. In a slightly complicated message the BoJ kept their target for 10yr JGBs at 0% but effectively widened the band to +1% from 0.5% even if they've kept the original bands as reference points. It confused me a bit this early in the morning but they won't be able to defend 0.5% now absent a macro development that structurally lowers yields. 10yr JGBs have increased +12bps as we type to 0.56bps, their highest since 2014 and all other things being equal this should continue to creep up in the days and weeks to come and removes an anchor for global yields. It's going to be an interesting press conference just after we go to print.

Initially, the Japanese yen strangely fell on the news to 141 but now trades +0.6% higher at 138.6. Elsewhere the Nikkei (-2.24%) is sharply lower with the KOSPI (-0.26%) also trading in the red. Chinese stocks are bucking the trend with the CSI (+1.79%) leading gains followed by the Shanghai Composite (+1.38%) and the Hang Seng (+0.89%). US stock futures are edging slightly higher with those tied to the S&P 500 +0.18%. Meanwhile, yields on 10yr USTs (+3.01bps) are at 4.02% as we go to press.

Coming back to Japan, Tokyo’s consumer price index (CPI) rose +3.2% y/y in July (v/s +2.9% expected). This is the 14th consecutive month that the inflation rate in the capital came in above the BOJ’s 2% target. At the same time, core inflation (excluding fresh food) advanced +3.0% y/y in July, higher than Bloomberg estimates of +2.9% but lower than prior month’s reading of 3.2%. More surprising was the core-core inflation (excluding fresh food and energy) which climbed to +4.0% y/y in July (v/s +3.7% expected, +3.8% in June) and provided more justification for the move today. Elsewhere, Australia’s retail sales sharply declined by -0.8% m/m in June, recording its biggest decline this year, versus expectations of a flat outcome.

Before the 6pm London headline markets were riding high on optimism and shrugging off higher US yields. This all stemmed from another round of strong US data that added to investors’ optimism. At one point the Dow Jones was comfortably on track to record a 14th consecutive daily advance for the first time since the index’s creation in 1896. So a 1-in-a-127 year event. Blame the Nikkei article for that streak being over and only equally the record run.

Even before the late rate moves investors were growing increasingly sceptical about Fed rate cuts anytime soon, with the 2yr real yield (+6.3bps) hitting another post-GFC high of 3.058% with 2yr nominal yields up +7.7bps. The rate priced in for the December 2024 meeting rose by +15.3bps on the day to 4.23%. This moved US rates in the opposite direction to European yields (2yr bunds -5.1bps) after a slight dovish bias to the ECB meeting. All these moves will be put to the test today, or reinforced, by US core PCE, US ECI (important to see if labour costs can fall organicallly), alongside German and French CPI.

The main catalyst for the early move higher in US rates, and the earlier risk on yesterday, was a robust GDP print from the US, which showed growth accelerated in Q2 to an annualised pace of +2.4% (vs. +1.8% expected). The report also came with several positive details, including that core PCE inflation was only at +3.8% in Q2 (vs. +4.0% expected), which added to the recent theme of better-than-expected growth and softer-than-expected inflation. As well as the GDP release, the weekly jobless claims fell for a third week running to 221k over the week ending July 22 (vs. 235k expected), which is their lowest level since February. And the continuing claims print for the previous week came in at a post-January low of 1.69m (vs. 1.75m expected). So lots of good news all round from an economic standpoint maybe before the full impact of the monetary policy lag starts to bite.

So as discussed at the top equities faded into the close with tech stocks seeing the biggest beta to the move with the FANG+ index falling from c.+2.3% to -0.24% in the last 3 hours of trading. Meta (+4.40%) outperformed thanks to its strong Q2 results after the previous day’s close. This helped lift the communication services sector into the green for the day (+0.85%) while the rest of the top level S&P sectors declined, most notably real estate (-2.13%) and utilities (-1.73%). In Europe markets closed before the sell-off and neatly encapsulated the earlier bullish sentiment, with the STOXX 600 (+1.35%) hitting a 17-month high, whilst France’s CAC 40 (+2.05%) and Italy’s FTSE MIB (+2.13%) saw significant advances of their own.

Before all this excitement, the ECB delivered their own 25bp rate hike as expected, which took the deposit rate up to 3.75%. However, unlike recent meetings, there wasn’t a strong steer about what they’re going to do next, and President Lagarde said that “we have an open mind as to what the decisions will be in September and in subsequent meetings”. She avoided signalling a specific outcome, and said that if they did pause, then it “would not necessarily be for an extended period.” At the same time, the language in the statement was also softened, since it said that future decisions would ensure rates “will be set at sufficiently restrictive levels”. That’s a change from last time, when it said they “will be brought to levels sufficiently restrictive”. See our economists’ review here.

When it comes to the ECB’s next decision, we should start to get some more signals today, as the flash CPI releases from France, Spain and Germany are coming out ahead of the Euro Area-wide release on Monday. Obviously the data will go a long way to determining the likelihood of another move, but markets are still pricing in a 71.7% chance of another 25bp hike in September anyway. Nevertheless, sovereign bonds rallied yesterday after the decision, with yields on 10yr bunds (-1.0bps), OATs (-1.6bps) and BTPs (-3.0bps) all coming down. That divergence between Europe and the US also meant that the spread of 10yr Treasury yields over 10yr bunds reached its widest level of 2023 so far, at 153.4bps.

When it came to yesterday’s other data, in the US we had the preliminary durable goods orders for June, which showed strong growth of +4.7% (vs. +1.3% expected). Core capital goods orders were more subdued however, with just +0.2% growth (but better than the -0.1% expected). Elsewhere, pending home sales for June beat expectations with a +0.3% gain (vs. -0.5% expected), and the Kansas City Fed’s manufacturing index came in at -11 (vs. -10 expected).

To the day ahead now, and data releases from the US include the Q2 employment cost index, June’s PCE inflation, personal income and personal spending, and the final University of Michigan consumer sentiment index for July. Over in Europe, we’ll get the French and German CPI readings for July. Central bank speakers include the ECB’s Simkus. Finally, earnings releases include Exxon Mobil and Procter & Gamble.

More By This Author:

Stocks Dump, Yields & Yen Spike On Regurgitated Trial Balloon BOJ "Will Discuss" Tweaking Yield Curve ControlECB Hikes 25bps As Expected, Future Decisions To Ensure "Rates Are Sufficiently Restrictive"

S&P Futures Soar To 2023 High After Dovish Fed, Meta Earnings

Comments

Log in or sign up to join the conversation.