From The Makers Of Wal-Mart And Bank Of The Ozarks Comes Bear State Bank

What's up with these regional US banks? So many of them are growth stories nowadays with crazy stock climbs in a weak economy. And that was before the elections. The small banks seem to be jumping since then.

Well, you're not just imagining this. As Thomas Michaud, CEO of the investment banking firm KBW said on CNBC's 12/21/15 interview, "there is a rise of regional champions" going on with the high powered merger activity we are used to seeing in the large money center banks shifting dramatically the last couple years or so to the well run regional banks looking to grow. Some of these growth stories have been stunning with stocks tripling or more, defying commodities, China, junk debt, and lack of economic growth.

As rates rise, banks will certainly benefit from a return to its classic business model. But a big difference in this rate cycle could be our escape from the aberrant zero interest era. As explained in this article, the Fed is now paying interest to banks over the prevailing rate to keep the massive QE sums on banks' balance sheets and out of lending into the economy to prevent inflation from going out of control. This amount will be $24 billion yearly if the Fed increases rates just once more. They are expected to do at least that. This was viewed as a problem back in 2013 as the commercial banks' reserves held at the Fed ballooned to over $2 trillion as noted in the Wikipedia account on this feature of the Fed:

As the economy began to show signs of recovery in 2013, the Fed began to worry about the public relations problem that paying dozens of billions of dollars in interest on excess reserves (IOER) would cause when interest rates rise. St. Louis Fed president James B. Bullard said, "paying them something of the order of $50 billion [is] more than the entire profits of the largest banks."

Banks are in a ZIRP induced sweet spot where they will, at a minimum, be collecting no risk interest ($34 million a day) no matter what happens in the economy - multiples of that if rates rise at all next year. This fallout from the Fed's tom foolery with creating an artificial market in everything looks like a windfall for the banks. It has been described as a "subsidy" to lenders for doing absolutely nothing. There is another megatrend that makes this development more significant - the drastic shrinkage in the number of banks as featured in a Wall Street Journal piece. Since 1985, the number of U.S. banks has shrunk from 18000 to around 6500 while squeezing deposit assets up from $3 trillion to about $10 trillion.

The weak banks being gobbled up by the strong is making the players left fewer and stronger. On top of that, not all commercial banks get this interest from the Fed, just the ones who are Fed member banks. You have to meet certain qualifications for that, and only about one out of three are member banks. If you take the $34 million a day in Fed interest payments and do the simple math, that's about $15000 a day for each surviving member bank, and will increase by multiples of $15000 for each rate increase by the Fed from here on. That's about as safe as revenue growth gets in a market starved for safe revenue growth. This federally guaranteed largess is perhaps one reason why the fast growing "regional champions" are doing so great the last couple years. The Trump effect is looking to amplify all this. So we're seeing the post election jumps in these stocks.

I have been very negative on banks in some of my other writings. Have I changed my mind? Well, banks are like Italian families. Some are involved in the mafia and are neck deep in nefarious global doings. And some families just like toughening up their kids as they raise them, like Frank Barone of Everybody Loves Raymond. They're all tough Italian families - but there is a huge difference in the mortality rate. It's the big global banks I am avoiding. There is a vast difference in the growing U.S. regionals run by tough, smart people, and the big banks drowning in derivatives and bad debt.

But do we want to buy banks into what appears to be a down debt cycle? The gloomy side of banking is centered around the commodity/junk debt problem that I wrote about in my 2015 article "The Debt Cycle And Rhymes of Lehman Brothers". In that article last year, I said of this gloom,"Personally I suspect this lopsided view of next year's stock market will be wrong" and I pointed out that "history has seen stock and debt markets act independently before, and next year [2016] may well be a case of that (hopefully) as was the year 1980." And I made this obsevation:

There we saw a nice climb for stocks even though we were entering the weak economy of '80-'82. The debt cycle was down as with any recession, and in fact snowballed into the Savings and Loan Crisis of the '80s that eventually saw one third of these banks go under! ... 1980 was an election year as is next year. To the extent you believe market forces are politically controlled, you have to put those forces all to the upside for 2016.

After the earthquake in Washington November 9, you must suspect, as in the early '80s, that we could see a down debt cycle with an up stock market, including the best run regional banks not being destroyed by debt.

Enter Bear State. It's a trick to find them before they have done big climbs and attracted attention. I offer Bear State Financial as such a find. It is a Fed member bank as are all state chartered banks. Although it is obscure to say the least, it has started on a growth track being orchestrated by some most able growth people on the planet. It was formulated as a dramatic reorganization of a struggling bank, First Federal of Harrison, in 2011. A corporate raider restructure was done by one Rick Massey. As the Bear State Financial website describes it:

On May 3, 2011, Bear State Financial Holdings made a $46.3 million investment in the Company to recapitalize First Federal Bank. Company Chairman Richard N. Massey led the Bear State group, which brought a new management team to the Bank. In June 2014, First Federal Bancshares of Arkansas, Inc. changed its name to Bear State Financial, Inc. (NASDAQ:BSF). Bear State Financial is the parent company for Bear State Bank.

In the Form SC13D (Statement of beneficial ownership) filed May 11, 2011 in conjunction with this $46 million "investment" in First Federal, it's clear it was a one man takeover by Massey. The name officially changed from First Federal with ticker FFBH to Bear State Financial with ticker BSF in June, 2014. The name Bear State was chosen for the large population of black bears in this part of the state.

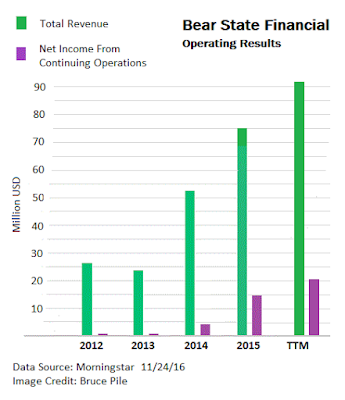

So how has this heavy handed takeover worked out so far?

Not too bad. Overall, there seems to be a turn into fast growth taking hold.

These results, as nice as they are, may not be the star attraction here. It's the Board. The Board of Directors for Bear State is an intriguing mix of success and power with Little Rock's movers and shakers. The Stephens Group, a diversified investment banker, officed in Little Rock, is the largest brokerage outside of Wall Street, New York. It has had a strange, bipartisan habit of rubbing shoulders with presidential power ever since Jackson Stephens attended the US Naval Academy and became friends with Jimmy Carter. He later became financially involved with his administration. Then the "king maker" was a big backer of Reagan in the early '80s and has been given varying degrees of credit for installing Arkansas Governor Bill Clinton in the White House.

Maybe Jack Stephens should have written the book How To Win Friends And Influence People. The football field at the US Naval Academy is named Jack Stephens Field to honor him. He underwrote the initial public offering for Wal-Mart Stores. Wal-Mart (WMT) is now the largest company in the world by revenue. The Stephens Group also had a hand in building Tyson Foods (TSN) and Alltel into giants. Alltel started in 1943 putting up telephone poles in Arkansas. By the mid 2000s, Alltel operated the largest network in the United States by area. Then Verizon (VZ) gobbled them up.

Stephens and his team have an eye for spotting growth potential. As the Wikipedia write up on him states it:

Jack began to grow Stephens by providing private equity to many young growing companies, much in the way of the British Merchant Bank investing model, predating by decades the private equity endeavors of Wall Street firms. Jack's acumen as an investor was combined in remarkable fashion with his ability to form enduring personal relationships with his partners. Several generations of companies and business leaders came to know Jack as not only a smart investment banker, but as a loyal and reliable friend as well. Jack's influence grew well beyond Arkansas to the boardrooms of corporate America and to the halls of Washington D.C.

What does this Arkansas power connection have to do with Bear State? Wal-Mart and Alltel are old news with this bunch, What they seem to be into now are regional banks. Many of the growth stories in the regional banks are launching from here including Home Bancshares, Inc. (Nasdaq: HOMB) of Conway and Bank of the Ozarks (Nasdaq: OZRK) of Little Rock. If you peek at what these two stocks have done the last 5 years, you see HOMB growing four fold and OZRK five fold.

Bank Director, the premier bankers' industry magazine, does a yearly ranking of banks by small, mid, and large size categories, and OZRK has held the number one ranking in the nation for the last four years running in its small, then mid size categories including its current number one rank in mid size. They rank the 300 best run banks out of about 6500 banks in the country. That's the top 1/2 of one % - it's an honor to even be in their ranking list.

In the SEC Prospectus filing for the 1997 IPO for Bank of the Ozarks, Stephens, Inc. is the chief underwriter. In this filing, it is amazing to read that the two main banks that came together to form Bank of the Ozarks were headquartered in Jasper, population 498, just a few miles south of Harrison, and Ozark, population 3525, just a few more miles south of Harrison. Wal-Mart's ground zero was actually this same Harrison.

After setting up shop in Rogers, AR, where I live, Wal-Mart's first store in 1962 labored as a local loner for almost 3 years. We didn't even think of it as a chain. Sam Walton himself described it in his book as an "experiment", trying his lower cost mass merchandising in a somewhat modest, unappealing building just to see if the concept would work. There's an antique mall in there today, I shop there. In 1965, when this store proved quite popular, the Waltons began the real building and expansion blitz we know of today, opening over 20 stores between 1965 and 1967 - starting with store #2 in Harrison, population 13,000. The Rogers "store" was still in the flea market as the building spree blasted into the '70s. Stephens took the company public in 1970.

What is it with Harrison anyway? I go over there a lot, and if you've ever been there, you know it's a cultural throwback. There's a joke that says if the world were to end, you'd want to be there, because it would end 30 years later. Why does the business elite of Little Rock like launching some of Wall Street's biggest growth behemoths from these backward hills? Is Harrison an alter ego of New York - the phantom Wall Street of the Ozarks?

Will The Phantom Strike Again with Bear State? Little Bear State is also from Harrison. Bear State could now almost be considered a branch of the Stephen's Group. For years before 2011, First Federal was thought of as a "Stephens controlled bank". And this piece from the Bear State website back in 2011 suggests a Stephens orchestrated rescue of First Federal in describing Bear's new board. Both Massey and Scott Ford had been key chiefs at Alltel, and Massey was Managing Director at Stephens for six years.

With Home Bancshares Inc. and Bank of the Ozarks, the role of Stephens was the public launch of those companies. With Bear State in 2011, there was no public launch, First Federal was already public. But Stephens supplied the board leadership that has essentially launched a new company. As promising as Bear State is, you see almost nothing being written about them. Bear State is already on a buying spree as detailed in this story published at Talk Business and Politics when they acquired Metropolitan National Bank last year. This was a quantum leap for Bear State as the MNB banks headquartered in Springfield, Mo. pushed total assets up by about a third, and breached the Missouri state line.

Already, a scant four years from reorganizing a failing bank, they are into the elite Banking Director list at #127 in the small category. So could this tiny backwoods regional bank be another embryonic Stephens growth beast springing from the Arkansas Outback? If you go to the BSF website, you see the heading "Your Financial Partner" emblazoned across a beautiful panoramic view of undisturbed rolling Ozark Mountains - where it looks as though the only financial partners have been trappers and the occasional Cherokee trader. Watching the green Bear State signs popping up in front of banks around here is starting to remind me of the very early days of the Wal-Marts, taking first steps in and around Harrison and here in Rogers, then creeping over the state lines of Missouri and Oklahoma with zero national attention.

As a fine point of terminology, I'd like to point out the difference between "Stephens, Inc." and "Stephens Group", the creators of Alltel, Bear State, and other enterprises. Sometimes "Stephens Group" is used to describe Stephens in general, but actually Stephens, Inc. is the investment banking arm, which helped form Alltel, Wal-Mart, and others, while Stephens Group, which does other business formation activities, is what is helping with the formation of Bear State. They are two separate entities.