With three months left, the fiscal 2023 budget deficit has already eclipsed the massive 2022 shortfall.

The US government ran a $227.77 billion deficit in June, pushing the total fiscal 2023 shortfall to $1.393 trillion, according to the Monthly Treasury Statement for June.

The budget deficit for the entirety of fiscal 2022 was $1.375 trillion.

The federal government continues to struggle with shrinking revenues. In June, the Treasury reported receipts of $418.32 billion. This was a healthy increase from May but was down 9.2% from June 2022.

It’s not a surprise that government receipts are falling. In fact, after record tax receipts last year, the CBO projected a drop in federal revenue.

The federal government enjoyed a revenue windfall in fiscal 2022. According to a Tax Foundation analysis of Congressional Budget Office data, federal tax collections were up 21%. Tax collections also came in at a multi-decade high of 19.6% as a share of GDP. But CBO analysts warned it won’t last. And government tax revenue will decline even faster as the economy spins into a recession.

The bigger problem is on the spending side of the ledger.

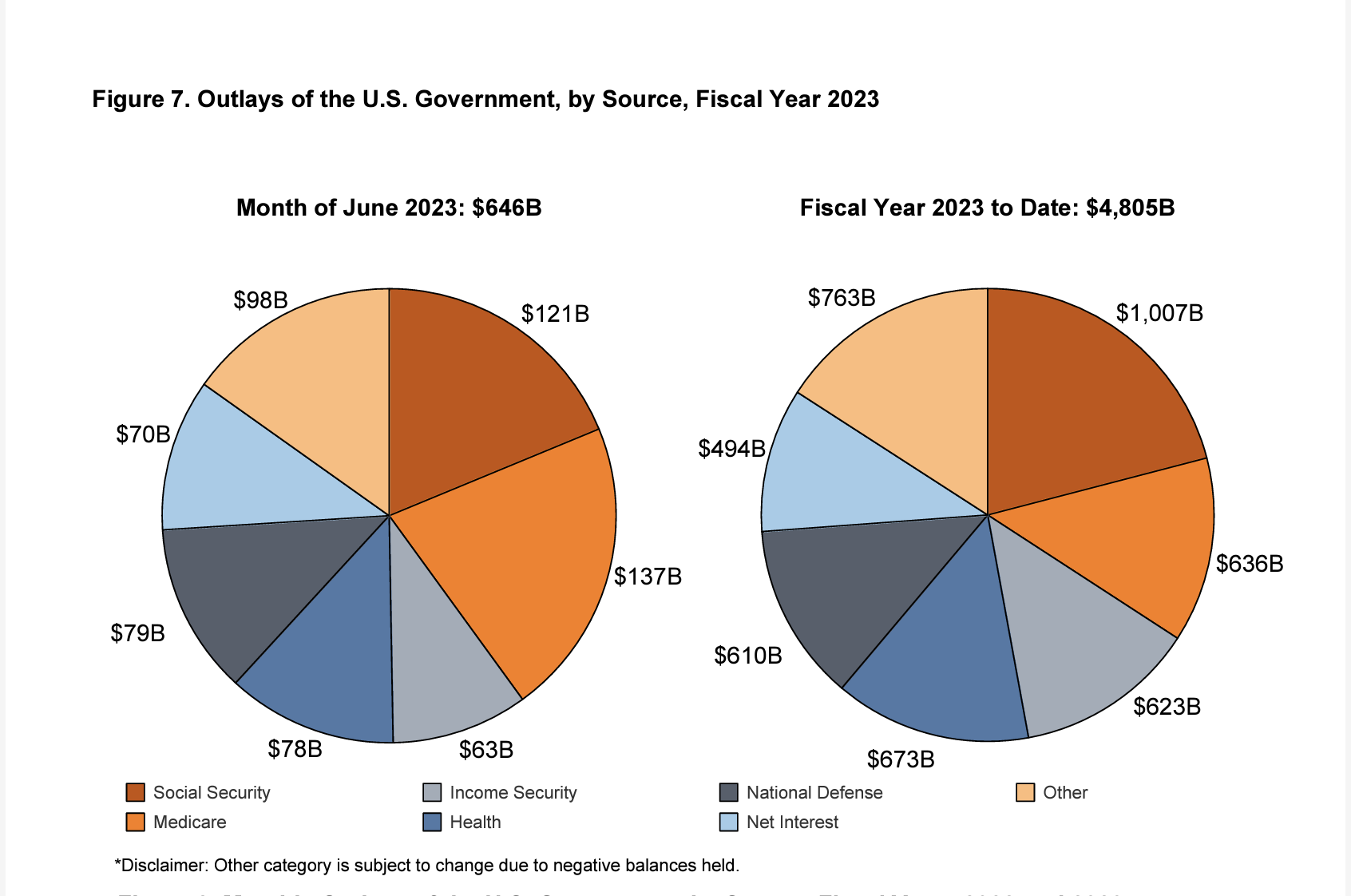

The Biden administration blew through another $646.09 billion in June. That was a 17.6% increase over June 2022 spending.

(Click on image to enlarge)

Now, you might be thinking that with the spending cuts in the Fiscal Responsibility Act, Congress fixed this problem. But we live in an upside-down world where spending cuts mean spending still increases in reality.

In other words, the spending cuts will not put a dent in current spending levels. That means we can expect these massive deficits to continue month after month. And it’s only a matter of time before Congress and the Biden administration abandon the pretense of spending cuts to address the next crisis.

Keep in mind, the feds now have a credit card with no limit.

The fundamental issue wasn’t that the US government couldn’t borrow enough money. The fundamental problem was, and still is, that the US government spends too much money. Despite the pretend spending cuts, the debt ceiling deal didn’t address that problem. Even with the new plan in place, spending will go up. And it’s already historically high. That means big budget deficits will continue and the national debt will mount.

The US Treasury blew up the national debt by $850 billion in June alone as it scrambled to make up the ground it lost while the government was up against its borrowing limit. The national debt now stands at $32.54 trillion.

Meanwhile, according to the National Debt Clock, the debt-to-GDP ratio stands at 122.9%. Despite the lack of concern in the mainstream, debt has consequences. More government debt means less economic growth. Studies have shown that a debt-to-GDP ratio of over 90% retards economic growth by about 30%. This throws cold water on the conventional “spend now, worry about the debt later” mantra, along with the frequent claim that “we can grow ourselves out of the debt” now popular on both sides of the aisle in DC.

To put the debt into perspective, every American citizen would have to write a check for $97,138 in order to pay off the national debt.

This is an unsustainable trajectory, especially in a high-interest rate environment.

And if you believe the rhetoric coming out of the Federal Reserve, rates aren’t going down any time soon.

Meanwhile, the federal government has paid nearly half a trillion dollars ($494 billion) on interest payments alone in fiscal 2023.

According to an analysis by the New York Times, net interest costs rose by 41% last year. The Peterson Foundation said the jump in interest expense was larger than the biggest increase in interest costs in any single fiscal year, dating back to 1962.

The cost of financing the debt will almost certainly rise even more now that Congress has done away with the debt ceiling for two years.

As the Treasury floods the market with new debt, bond prices will likely fall in order to create enough demand for all of those Treasuries. Bond yields are inversely correlated with bond prices, and as prices fall, interest rates rise.

We’re already seeing extreme weakness in the bond market. Financial analyst Jim Grant recently said we could be heading toward a generational bear market in bonds. This would mean rising interest rates for the US government even if the Fed stepped in and tried to push rates down. This is an unsustainable trajectory for the US government. It simply cannot continue to borrow at this pace in a high-interest rate environment.

In fact, if interest rates remain elevated or continue to rise, interest expenses could climb rapidly into the top three federal expenses. (You can read a more in-depth analysis of the national debt HERE.)

The soaring national debt and the US government’s spending addiction are big problems for the Federal Reserve as it battles price inflation. As you’ve already seen, the push to raise interest rates is putting a strain on Uncle Sam’s borrowing costs. But there is an even bigger problem. The Fed can’t slay monetary inflation — the cause of price inflation — with rate cuts alone. The US government also needs to cut spending.

That’s not happening, despite Republican Party talking points.

Something has to give. The Fed can’t simultaneously fight inflation and prop up Uncle Sam’s spending spree. Either the government will have to cut spending in real life, or the Fed will eventually have to go back to creating money out of thin air in order to monetize the debt. It seems likely that at some point in the near future, the Fed will have to go back to quantitative easing in order to rescue the bond market. This will mean more inflation.

More By This Author:

There’s No Place Like Home

Many Countries Bringing Their Gold Home For Safekeeping

Credit Card Borrowing Still Running Hot Even As Borrowing For Big-Ticket Items Tanks

Comments

Log in or sign up to join the conversation.