Fed Chair Jerome Powell acknowledged that the strong jobs report underscores that central bankers have more work to do to ensure inflation hits target, but he chose not to ratchet up the hawkish rhetoric on the back of one data print. Other Fed officials also suggest the central view of a couple more rate hikes remain the base case for now.

Powell: Labour markets remain a risk, but inflation to return to target by next year

Following Friday’s jobs report we have started to get the reactions of Federal Reserve officials and today it is the turn of Chair Jerome Powell. Speaking to the Economics Club of Washington he again stated that they “probably need to do further interest rate increases” with the strong jobs number underscoring there is a “significant road ahead” to get inflation back to target. This broadly echoes comments from last week’s press conference where he stated “we've raised rates four and a half percentage points and we're talking about a couple of more rate hikes to get to that level we think is appropriately restrictive”.

While acknowledging that the disinflationary process has started in the goods sector, it isn’t as pronounced in the services sector and there is “a long way to go”. He believes it will happen in the housing components in the second half of the year, but it is the services ex-housing component where he is most uncertain. Labour costs are a clear driver of what happens in this sector and Friday’s jobs number highlights the risks.

He is concerned that the pandemic has had a lasting legacy on the jobs market which will be structurally tighter for longer due to the absence of potential workers. This is likely to keep inflationary pressures emanating from the labour market more elevated relative to the pre-pandemic period – at least for a while – and argues against an early loosening of monetary policy. Consequently, while inflation is expected to fall sharply through 2023, he is of the view that it will be 2024 before we “get close to 2%”. Interestingly, he dismissed the idea of accelerating the run-down of the Fed’s huge balance sheet at this time, which could help nudge longer dated borrowing costs higher.

Fed sticking with its December forecast view

Neel Kashkari and Raphael Bostic have also spoken in the past couple of days and they highlighted the strength of the jobs numbers, which has raised the chances the Fed needs to be more aggressive in terms of policy tightening, but one print hasn’t impacted their own personal forecasts as yet. While Chair Powell is seemingly in the two more hikes camp and Bostic confirmed he sees the Fed funds rate hitting 5.1%, Kashkari still favours a 5.4% level, equating to three more 25bp hikes.

The fact that he didn’t become more hawkish in the wake of the jobs report has seemingly come as a modest relief to markets. We argue that the report isn’t as strong as the headline number suggests with our note from yesterday outlining our view that it was due to reduced seasonal firings rather, tied to mild weather and labour hoarding rather than actual hirings. Moreover, the fact that in net terms, all the jobs created since March last year have been part time, predominantly in lower paid sectors, is not an especially convincing sign that the jobs market is especially hot. This is especially the case given that the BEA’s measure of personal incomes, the BLS measure of average hourly earnings and the employment cost index are converging on pre-Covid growth trends.

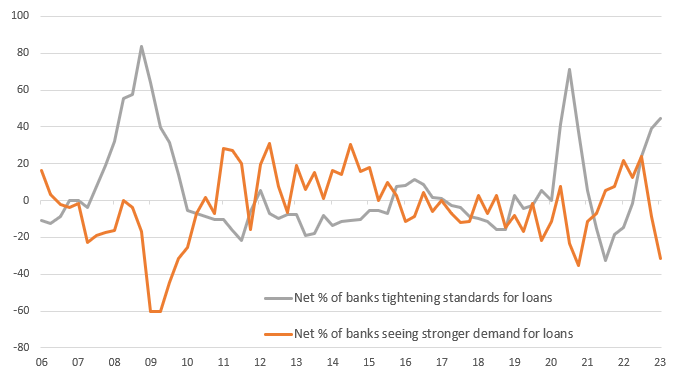

Tighter lending standards despite loosening financial conditions

Adding to the mix is yesterday’s Senior Loan Officer Survey from the Federal Reserve. While financial conditions may have eased on market measures using long dated borrowing costs, the dollar and credit spreads this isn’t the story faced by companies and households. Banks are tightening lending standards significantly for small, medium- and large-sized firms and are also tightening lending standards for consumer loans too. This has prompted a marked decline in loan demand across all markets according to Federal Reserve data.

Fed's Senior Loan Officer survey suggest things are getting tougher for corporates and households

Source: Macrobond, ING

The reasons cited for bank caution were an “uncertain economic outlook, a reduced tolerance for risk, and the worsening of industry-specific problems”. A “significant” factor for many also included “decreased liquidity in the secondary market for C&I loans, less aggressive competition from other banks or nonbank lenders, deterioration in their current or expected liquidity position, and increased concerns about the effects of legislative changes, supervisory actions, or changes in accounting standards”.

Meanwhile, the weaker demand for loans was put down to “decreased customer investment in plant or equipment, as well as decreased financing needs for mergers or acquisitions, inventories, and accounts receivable”. Unfortunately, “major net shares of banks” reported they expect the situation on both lending standards and loan demand to worsen through 2023, with a particular focus on credit quality.

As such, we are loathe to make major revisions to our forecasts on the back of one firm jobs print. We expect a much weaker jobs figure for February with the tightening credit conditions faced by the economy acting as a clear headwind to growth. Consequently we continue to forecast just one more rate hike in March, before a six to nine month pause with rate cuts still firmly on the cards for later this year despite the Fed’s current guidance.

More By This Author:

Hungarian Industry Surprises On The UpsideFX Daily: The Dollar Comeback Hinges On Powell, Again

FX Talking: Soft Landing, Hard Landing, No Landing?

Comments

Log in or sign up to join the conversation.