It’s been a rough year to date for US stocks overall, but within the equity-factor space, the modest rise for shares with relatively high dividend payouts is a conspicuous counterpoint.

Vanguard High Dividend Yield (VYM) stands apart as the only source of profit so far in 2022, based on a set of ETFs representing a broad set of equity risk factors. VYM is up 1.1% year to date through yesterday’s close (June 7). That’s a mild gain, but it’s an impressive performance when compared with its factor counterparts. VYM’s trailing 12-month dividend yield is a relatively rich 2.79%, according to Morningstar.com — roughly double the yield for US stocks in general via SPDR S&P 500 (SPY).

(Click on image to enlarge)

Performance-wise this year, everything else is in the red vis-a-vis factor risk premiums. The broad market via SPDR S&P 500 (SPY) is also down more than 12% this year. But even that pales next to the deepest equity-factor loss in 2022: a near-21% tumble for iShares S&P 500 Growth ETF (IVW), which targets large-cap firms in this corner.

(Click on image to enlarge)

Growth stocks generally are having a tough time in 2022 to no small degree due to the reversal of fortunes of tech shares. “Big technology stocks are in the midst of their biggest rout in more than a decade,” reports The Wall Street Journal. “Some investors, haunted by the 2000 dot-com bust, are bracing for bigger losses ahead.”

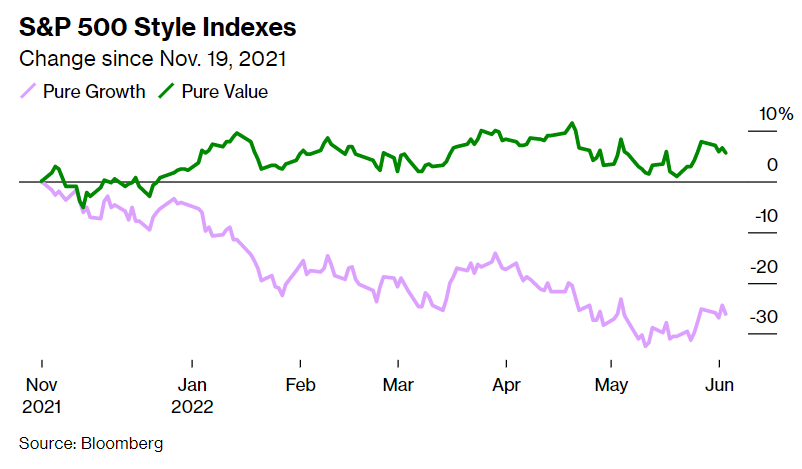

On the flip side, value stocks and shares with relatively high payouts are faring well, at least in relative terms. The revival of the value factor lately marks a change from a decade or more of languishing in growth’s shadow. As Bloomberg notes, the S&P Pure Value Index, a proxy of companies with low valuations based on the ratios of their share price to their book value, earnings, and revenue, has earned nearly 8% on a total-return basis over the past seven months. The S&P Pure Growth Index, by contrast, has shed 25%.

“High inflation is good for value,” says Rob Arnott, founder and chairman of Research Affiliates and a widely quoted advocate of value investing. He explains that when inflation pressure rises, the outlook becomes more uncertain generally and so investor demand increases for “boring, steady-as-you-go businesses.”

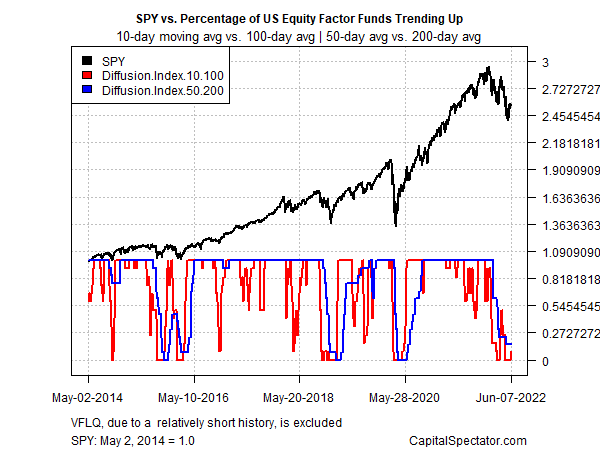

Monitoring the ebb and flow of equity-factor momentum overall via a set of moving averages suggests that the cycle is close to a near-complete reversal following the broad upside bias that still prevailed at the start of 2022 (see chart below). If an extended downside run for stocks generally is underway (i.e., a “bear market”), more factor pain probably awaits. By contrast, if the market correction this year is largely behind us, the across-the-board pessimism for equity risk factors could be a sign of a bottom for factor risk premiums. Unfortunately, the case for one or the other market profile remains fuzzy until deeper clarity is forthcoming on the outlooks for inflation, the Ukraine war, and the US business cycle.

Comments

Log in or sign up to join the conversation.