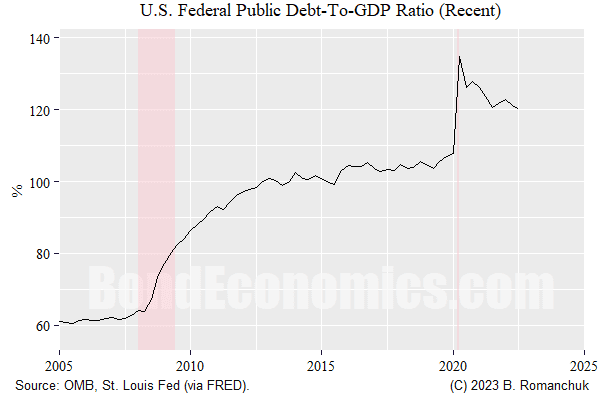

I saw a comment about the drop in the U.S. Federal debt-to-GDP ratio, which reminded me that I wanted to discuss it once the data started to settle down. As can be seen in the above chart, the public debt-to-GDP ratio went from 135% in 2020Q2 to 120% in 2022Q3 (latest figure on FRED). A drop of (roughly) 15% in the ratio without some kind of “austerity” policies might seem surprising — but it is only surprising if you look at debt dynamics the wrong way. That wrong way is relying on “real” variables — real GDP growth, real interest rates — as well as thinking too much about long-term “steady state” or “equilibrium” values.

The reliance on “real analysis” (ha ha) leads to silly things like charts of the U.S. debt/GDP ratio marching in a straight line towards 200%. (Yes, CBO, I am not laughing with you.) This framing also leads to neoclassical economists going on about the question: is r greater or less than g?

What is “Real Analysis”?

The standard way of projecting debt/GDP ratios is as follows.

-

The assumption is that the economy will grow at its “potential growth rate,” g which is a growth rate for real GDP. This potential growth is (roughly) the sum of the growth of productivity per worker (which is allegedly stable) and the growth of the working age population (which can be predicted fairly accurately as long as net immigration is near forecast).

-

There is a well-defined long-term neutral interest rate r that is defined as a real interest rate that actual interest rates will converge to.

-

Taken together, if we project debt/GDP on an infinite horizon, debt/GDP will go to infinity if r>g if there is not serious fiscal retrenchment.

-

Interest spending is assumed to not have stimulative effects on the economy, so all that matters is the “primary fiscal balance” — the fiscal balance excluding interest payments.

The resulting analysis allows us to (allegedly) accurately predict the long-term path of the debt-to-GDP ratio, and is consistent with the most scientific (i.e., neoclassical) models. (Please ignore those hecklers in the cheap sets who are yelling that the the existence of a neutral real interest rate is essentially an assumption of neoclassical models.) Furthermore, by putting everything in real terms, we can ignore inflation.

From the perspective of someone used to this framework, the debt-to-GDP ratio is largely driven by the primary fiscal deficit, and thus to lower the debt-to-GDP ratio, we need to run primary surpluses for an extended period.

Real World is Nominal

The problem with the previous analysis is that the real world is nominal, and the “short term” matters. Developed countries try to keep relatively long weighted average maturities for their debts. (This article puts the weighted average maturity around 6 years for the United States.) This implies that interest expenditures will take roughly half a decade to converge with current interest rate levels.

(The discounted value of inflation-linked debt will rise immediately in line with the price index, as the U.K. has found out.)

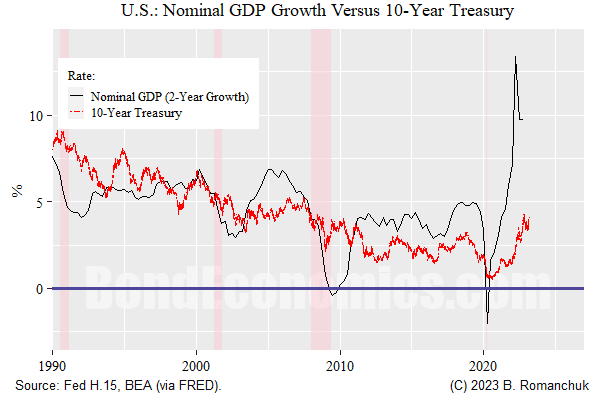

The chart above shows the 2-year growth rate of nominal GDP (I used 2 years to shave down the pandemic blip) versus the nominal 10-year yield, which I am using as a stand-in for the middle of U.S. coupon debt issuance. Look at where the 10-year yield was over the past decade, and ask yourself whether you think nominal GDP growth rate will be down at those levels at any time soon?

One interesting verbal tic mainstream economists have is that they will invariably describe what happened as “inflating away the debt” — since real GDP growth is allegedly fixed. Given the fixation on “structural reforms to improve real growth” by the same economists in other contexts, you would think that they would recognise that real growth is not in fact constant, and you can have periods of sluggish growth (e.g., the 2010’s). Admittedly, a lot of the post-pandemic surge in nominal GDP was the deflator, but it will not be hard to raise real growths versus the 2010’s baseline. Even 0.5% greater real growth matters a lot for medium-term debt projections.

When we look at the annual change in the debt-to-GDP ratio, we see that the “steady state” fiscal deficit (the deficit that leaves the ratio unchanged) is given by:

Steady state deficit (% of GDP) = (nominal GDP growth (%)) × (debt/GDP ratio (%))/(100%).

(Yes, it looks silly to have a “divide by 100% term,” but my feeling is that people are used to thinking of a debt/GDP ratio of 1 as 100%.)

This means that we need increasingly large deficits to keep the debt-to-GDP ratio constant. For 5% nominal growth (typical for the post-1990 era),

- 50% debt/GDP = 2.5% deficit;

- 100% debt/GDP = 5% deficit;

- 120% debt/GDP = 6%.

A fiscal deficit is a source of net income to the “non-central government sector” (private domestic, sub-sovereign governments, external sector). Although interest spending almost certainly has a lower fiscal multiplier than other spending (e.g., pension funds are not taxable and only slowly distribute wealth increases), deficits greater than 6% of GDP are going to be hard to sustain without some kind of inflationary effect (raising nominal GDP growth).

The above relationship explains why it was so painful to lower debt-to-GDP ratios in an environment where the debt-to-GDP ratio was lower than 100%: the steady state nominal GDP growth rate was so low that fiscal retrenchment was required to actually reduce the debt ratio. Once the debt ratio is high enough, the automatic stabilisers in fiscal policy are pretty much enough to do the job.

The debt-to-GDP ratio marched higher after the early 1980s — matching the secular downtrend of nominal GDP growth, and an ageing working age population that was hoarding financial assets ahead of retirement. However, those secular trends are largely past, and further increases in the debt ratio are fighting basic mathematics.

In order to get really exciting debt/GDP ratios, we either need a country mired in state where nominal GDP growth is non-existent (post-1990s Japan) or emulating a wartime economy where something like rationing is used to control the inflationary impact of large fiscal deficits. Although such scenarios are not impossible, they certainly should not be viewed as a base case projection for the United States.

Concluding Remarks

We cannot ignore nominal values and the effect of interest expenditures in our analysis. For a longer discussion of this topic, I would point readers to my Chapter 7 of book Understanding Government Finance.

More By This Author:

Financial Markets And InflationGovernment Bonds As Money

MMT After The Pandemic Shock

Comments

Log in or sign up to join the conversation.