Most Asian equity markets had a positive trading session as the region drew inspiration from the gains on Wall Street. The S&P 500 and Nasdaq reached nine-month highs, buoyed by optimism surrounding the debt ceiling, falling labour costs, and dovish commentary from the Federal Reserve. Meanwhile, US index futures remained steady after the Senate also passed the debt ceiling bill. However, further upside potential was limited ahead of the impending US jobs data.

The Nikkei 225 (+1.0%) received support from comments made by Bank of Japan Governor Ueda, who reaffirmed the central bank's dovish stance. SoftBank emerged as one of the major gainers after receiving a buy rating from Jefferies and benefiting from the recent artificial intelligence technology bid leading up to the ARM IPO. Both the Hang Seng and Shanghai Composite followed the overall positive sentiment, with Hong Kong outperforming due to a rally in the property and technology sectors.

With no tier one data of note on the European data slate investor attention will shift Stateside for the the Non-Farm Payrolls (NFP) report for May, which is anticipated to show a moderation in job growth, with expectations of 190,000 new jobs compared to the previous month's 253,000. However, analysts' forecasts vary, ranging from 100,000 to 293,000. The unemployment rate is projected to rise slightly to 3.5% from 3.4%, while wage metrics are expected to ease to 0.3% month-on-month from 0.5%, while maintaining the year-on-year pace of 4.4% seen in April. Leading up to the NFP release, labour market indicators for May provided a mixed picture. The ADP employment number indicated strong job growth, but the wage components in that survey showed signs of cooling. Jobless claims data during the survey week for the Bureau of Labor Statistics (BLS) report came in lower than expected for both initial and continued claims. Additionally, the S&P Global PMI report highlighted solid growth in the manufacturing sector and a faster pace of employment growth in the services sector. The Challenger Layoffs report exceeded expectations. Notably, the latest JOLTS data surpassed expectations, and this report will be influential in assessing the Federal Reserve's reaction. In the lead-up to the data release, markets priced in a nearly 70% probability of a 25 basis point rate hike in June, however, market sentiment shifted quickly when Federal Reserve voters, Vice Chair Nominee Jefferson and Harker, expressed their preference to "skip" a rate hike at the upcoming June Federal Open Market Committee (FOMC) meeting. Their rationale was to allow more time for assessing the incoming data, policy lags, and the impact of credit tightening before deciding on the appropriate level of policy tightening. It is worth noting that Harker mentioned that his view could change depending on the data in the interim period. As a result, the Non-Farm Payrolls (NFP) report will be closely watched to gauge the Federal Reserve's reaction function and gather insights into their potential policy stance ahead of Fed officials entering their ‘blackout’ period this weekend. Furthermore, the Consumer Price Index (CPI) and Producer Price Index (PPI) reports scheduled for June 13th and 14th, respectively, will also play a crucial role in shaping the Federal Reserve's decision-making process.

FX Options Expiries For 10am New York Cut

(1BLN+ represent larger expiries, more magnetic when trading within daily ATR)

-

EUR/USD: 1.0690-00 (2.01BLN), 1.0725-35 (882M)

-

1.0750 (793M), 1.0775 (284M), 1.0790-00 (486M)

-

USD/JPY: 138.25-30 (831M,, 139.20-30 (612M)

-

140.00 (642M). AUD/JPY: 0.9090 (250M)

-

USD/CHF: 0.8900 (250M), 0.9005 (252M), 0.9050 (692M)

-

0.9200 (400M)

-

GBP/USD: 1.2225 (298M), 1.2250 (335M), 1.2350-60 (377M)

-

AUD/USD: 0.6500 (420M), 0.6525-35 (266M), 0.6550 (281M)

-

0.6600 (419M), 0.6620 (299M)

-

NZD/USD: 0.5800 (382M), 0.5950 (770M), 0.6100 (497M)

-

USD/CAD: 1.3400-05 (450M), 1.3580 (558M)

-

1.3420-30 (625M), 1.3500 (396M), 1.3515-25 (340M)

-

1.3575-80 (702M), 1.3600-05 (966M), 1.3615-20 (855M)

-

USD/ZAR: 19.4500 (230M)

Overnight News of Note

-

Asian Shares Rise On Debt Bill Progress, Fed Pause Hopes

-

Stock Futures Inch Higher As Wall Street Eyes May Jobs Report

-

Fed’s Harker Says FOMC Should At Least Skip June Rate Hike

-

Fed Emergency Lending To Banks Ticks Down In Latest Week

-

Debt-Limit Deal Clear Congress, Ending Threat Of US Default

-

Goldman Cuts China Index Target, Retaining Overweight Call

-

BoJ's Ueda: No Set Time Frame Reaching 2% Inflation Target

-

Economists See More Near BoJ Change Chance Over Market

-

Hawkish Aussie Economists Expect RBA Raising Rate To 4.6%

-

Australia Raises Minimum Wage 5.75%, Boosts Hike Pressures

-

Brussels Urge UK To Join Trade Pact To Ease Risk Of Car Tariff

-

Oil Head For Weekly Decline Ahead Of OPEC+ Supply Meeting

-

Dell Say Quarterly Sales Top Estimates, Business PCs Surprise

-

Broadcom Expect Q3 Revenue Above Estimates Over AI Boost

(Sourced from Bloomberg, Reuters and other reliable financial news outlets)

Technical & Trade Views

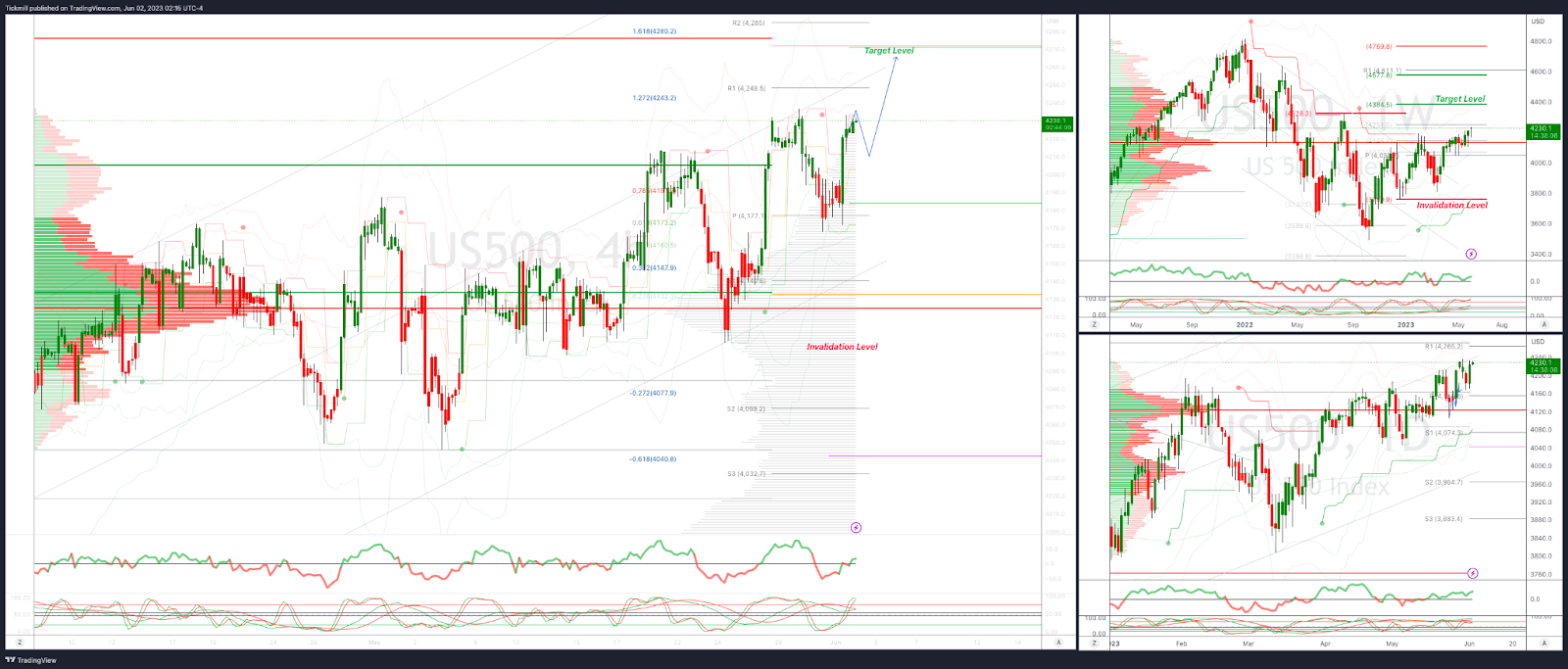

SP500 Bias: Intraday Bullish Above Bearish Below 4200

-

Below 4200 opens 4170

-

Primary support is 4126

-

Primary objective is 4268

-

20 Day VWAP bullish, 5 Day VWAP bullish

(Click on image to enlarge)

EURUSD Bias: Intraday Bullish Above Bearsih Below 1.0750

-

Above 1.0765 opens 1.0830

-

Primary resistance is 1.0830

-

Primary objective is 1.06

-

20 Day VWAP bearish, 5 Day VWAP bearish

(Click on image to enlarge)

GBPUSD Bias: Intraday Bullish Above Bearish Below 1.2440

-

Below 1.23 opens 1.2234

-

Primary support is 1.23

-

Primary objective 1.2680

-

20 Day VWAP bullish, 5 Day VWAP bullish

(Click on image to enlarge)

USDJPY Bias: Bullish Above Bearish Below 139.60

-

Below 139.50 opens 138.90

-

Primary support is 137.40

-

Primary objective is 141

-

20 Day VWAP bullish, 5 Day VWAP bearish

(Click on image to enlarge)

AUDUSD Bias:Intraday Bullish Above Bearish Below .6580

-

Below .6490 opens .6450

-

Primary resistance is .6680

-

Primary objective is .6450

-

20 Day VWAP bearish, 5 Day VWAP bullish

(Click on image to enlarge)

BTCUSD Bias: Intraday Bullish Above Bearish below 26000

-

Below 26000 opens 25800

-

Primary support 26000

-

Primary objective is 34600

-

20 Day VWAP bullish, 5 Day VWAP bearish

(Click on image to enlarge)

More By This Author:

FTSE Green Shoots As Summer Trading Starts

Daily Market Outlook - Thursday, June 1

FTSE Closing Out The Month Firmly In The Red

Comments

Log in or sign up to join the conversation.