In this week’s Dirty Dozen Sixteen [CHART PACK], we pull way back and look at the really big picture. We dive into how a number of various cycles are syncing up (geopolitical, debt, conflict & cooperation, real vs. financial assets, etc…). And we lay out why the next decade(s) won’t be like the last.

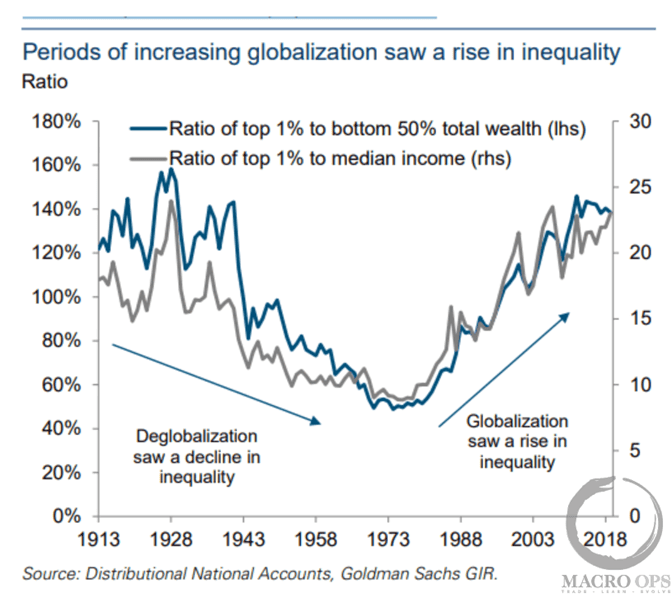

- The most recent cycle of globalization that kicked off in the 70s was a significant driver of income inequality, as US labor was forced to compete with millions of low wage workers from Eastern Europe and China. This dramatically shifted power from labor to capital.

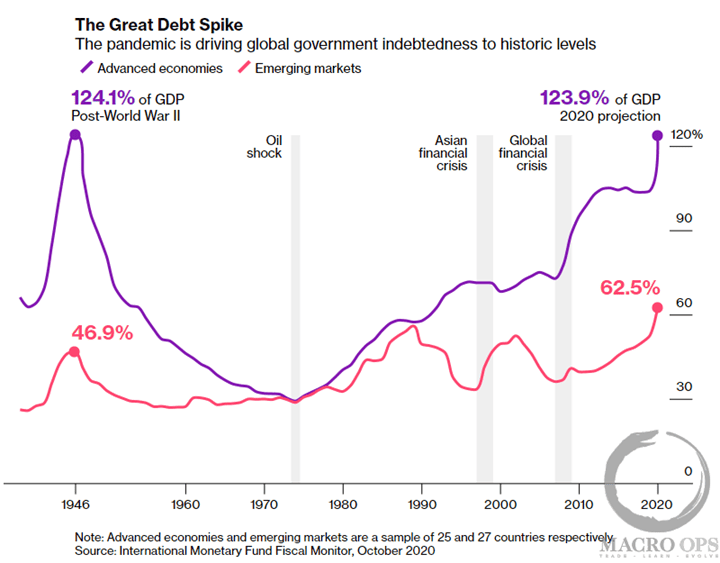

- Labor lost its bargaining power. Real wages declined, and inflation trended lower on a secular basis, allowing interest rates to also move lower over multiple decades. Lower interest rates meant lower debt servicing costs. This meant more capacity for expanding credit, driving a Long-term Debt Cycle, not just in the US but in many other parts of the world.

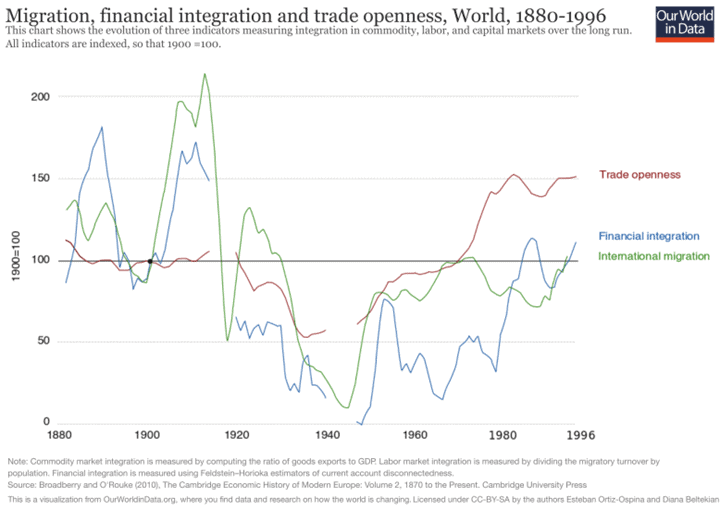

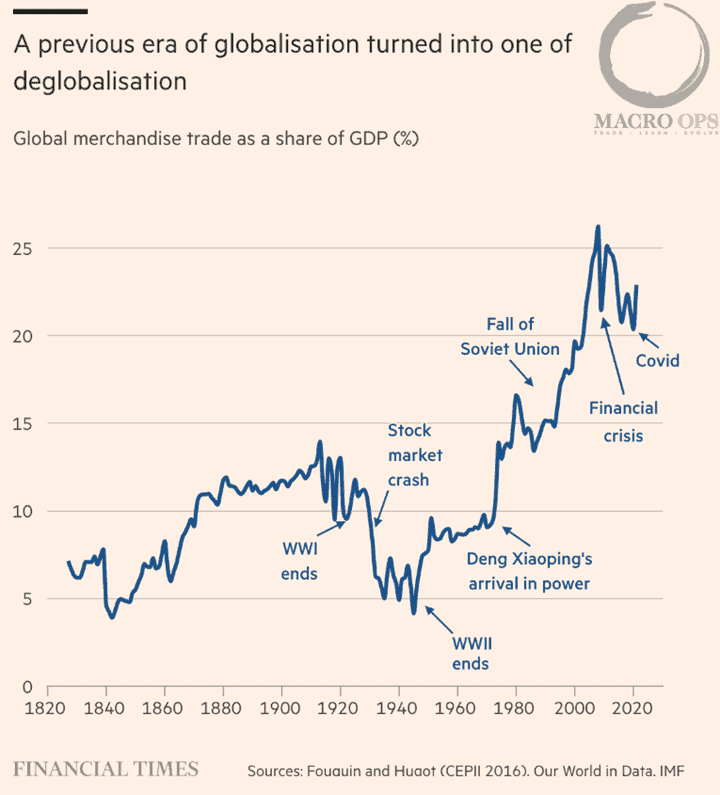

- With the ability to lower interest rates each and every time the market and economy hit a rough patch, volatility was suppressed. Not just in asset prices and the economy, but in global affairs. Global integration and trade openness rose to levels last seen just prior to WWI, which was the peak of the previous globalization cycle.

- But you can only lower interest rates so far. And you can only allow inequality to expand to a certain point. Eventually, you find that the volatility you thought you suppressed, was really just transferred to a later date. And the cycle begins to move in reverse…

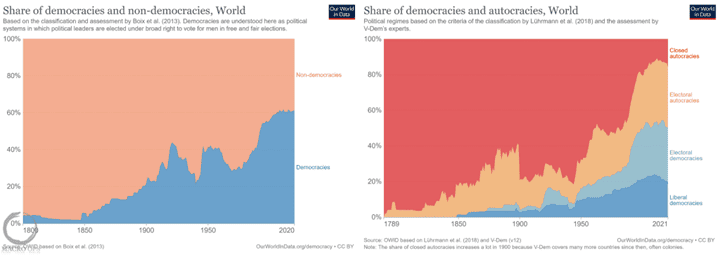

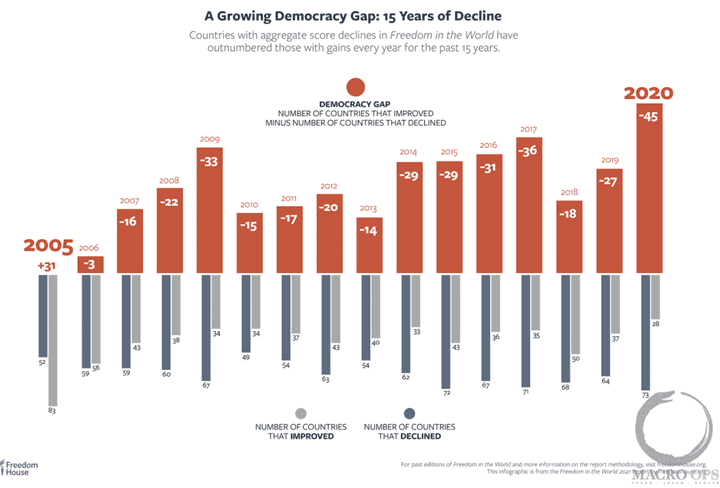

- Many other global trends key off this cycle. Take the powerful long-term trend of democracy as an expanding form of governance. The trend is clearly up and to the right, as democratic systems are vastly more robust than their fragile autocratic counterparts.

But, as we can see, this trend doesn’t move in a straight line. It’s turning over now and the last time we saw a prolonged period of stagnation was during the previous period of deglobalization / major deleveraging cycle.

- All of these cycles (debt, global integration, democracy, cooperation) peaked around the GFC and have been reversing ever since. They are accelerating now and there are a number of reasons why, which we’ll explore in an upcoming piece.

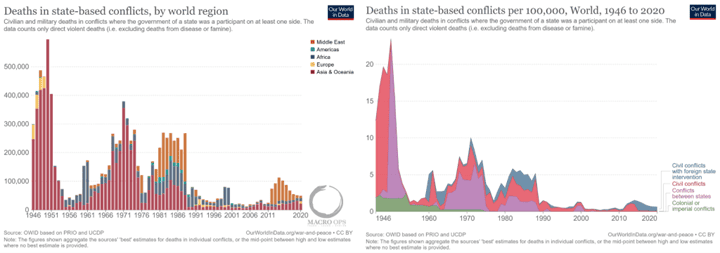

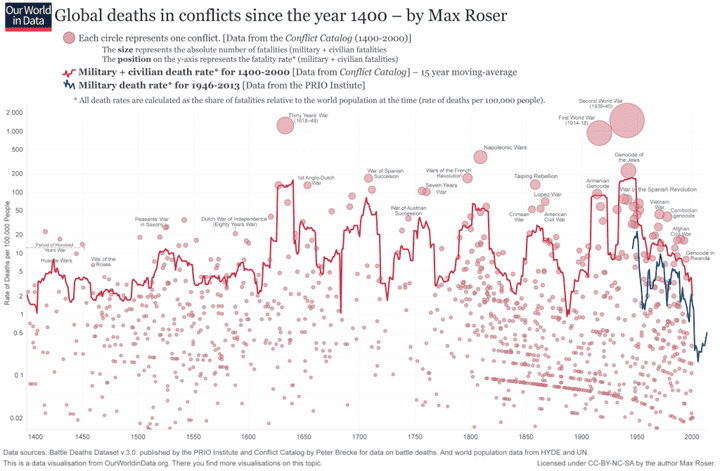

- Volatility was suppressed across the board, including in the number and scale of violent conflicts.

- These volatility cycles repeat time and time again throughout our history. And we’re just now coming off of an anomalous period of prolonged peace.

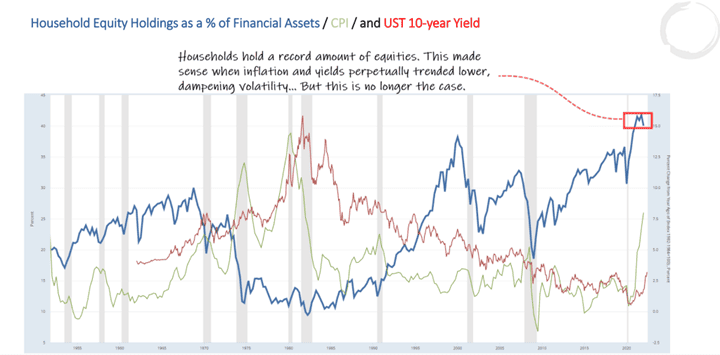

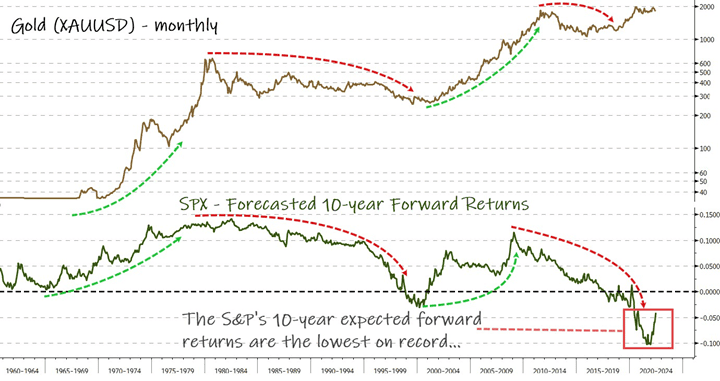

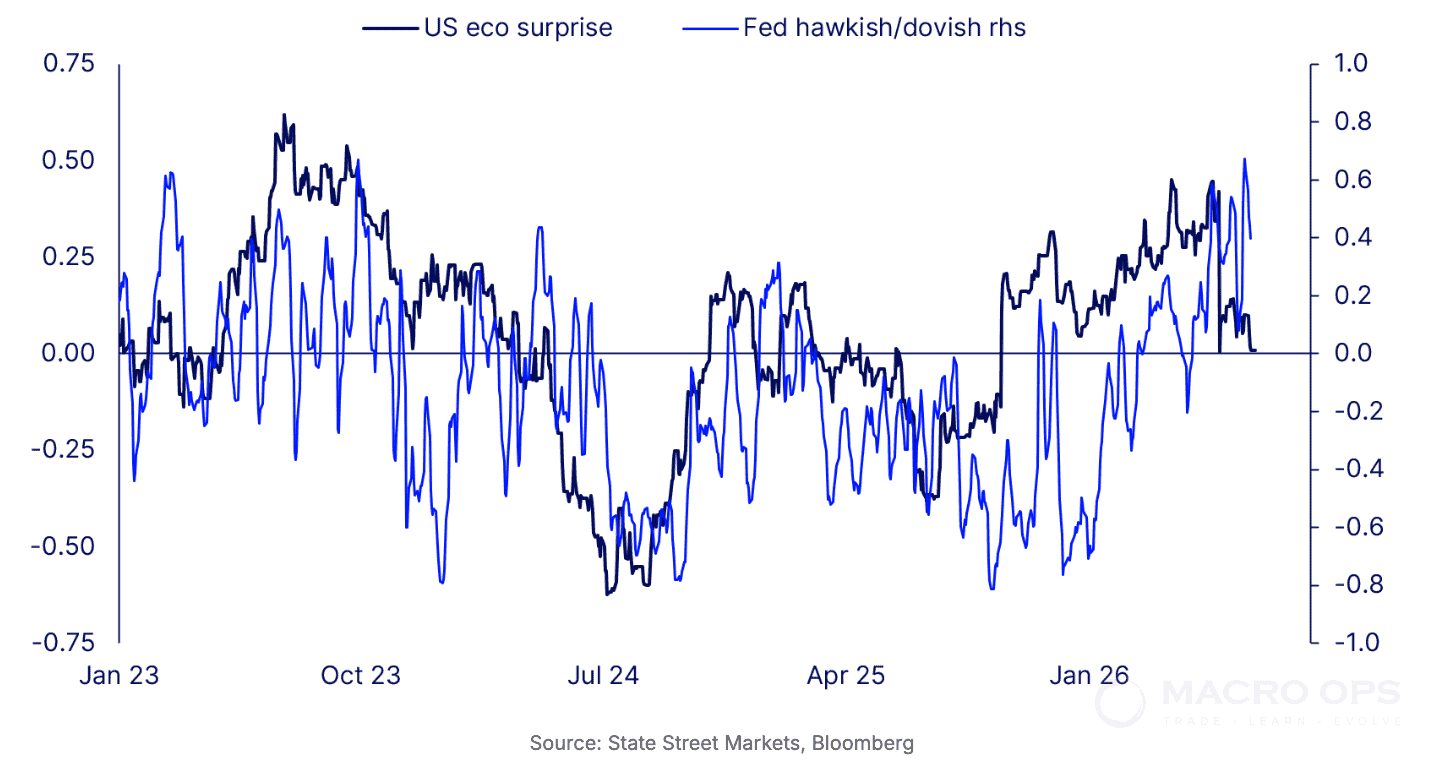

- Increasing global volatility, higher inflation, and rising interest rates are now running up against a near-record high allocation in stocks.

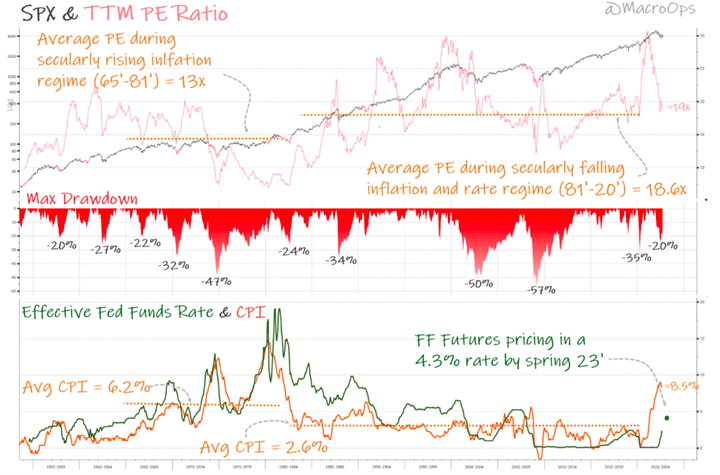

- I shared this chart back in September (link here). But where you think multiples will settle largely depends on where you think inflation will bottom. In an upcoming report, I’ll be making the case that we’re entering a new secular inflation regime, which will mean lower average multiples for risk assets.

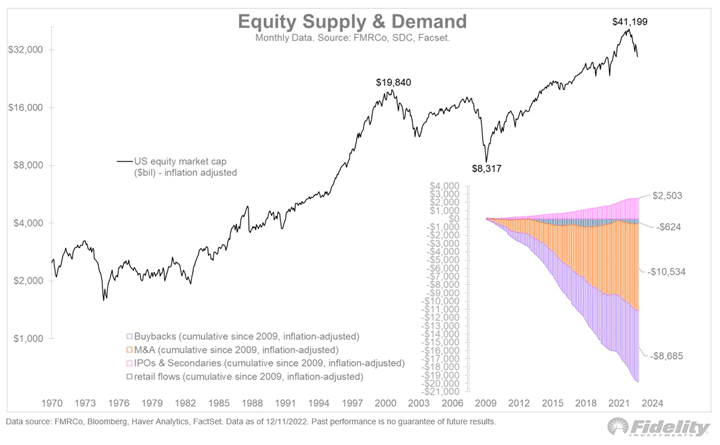

- Net equity issuance is one of the Most Important Fundamentals when looking at long-term stock market returns, as I discussed here. Buybacks have been an incredible tailwind for the US stock market over the last decade (chart via @TimmerFidelity).

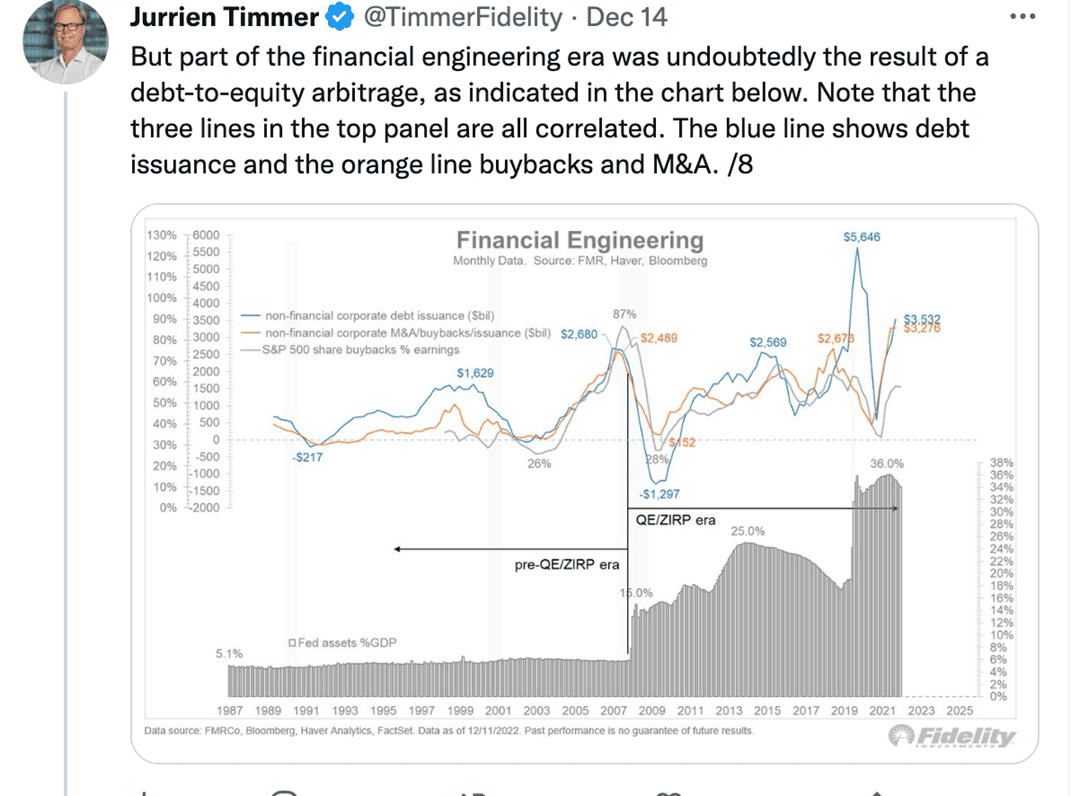

- Falling interest rates drove the increasing use of leverage and financial engineering, which propped up asset prices, and suppressed volatility while increasing overall fragility. If higher structural inflation means higher rates and a more expensive cost of capital, what does that do to this tailwind? You can read Timmer’s full thread here.

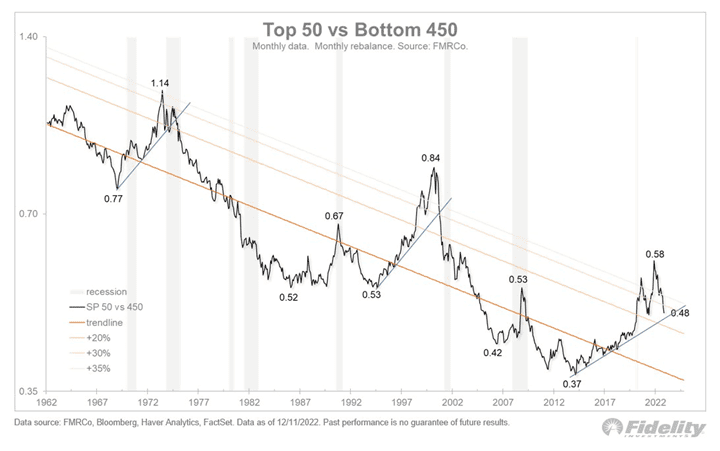

- The mega-cap stocks were some of the most aggressive in buying back shares. They were also some of the biggest beneficiaries of globalization (cheap labor and EM growth), both of which helped drive concentration in these names to extremes. But it looks like mean reversion is on the way, which I wrote about in A Mutant Selling Deformity… (chart via @TimmerFidelity).

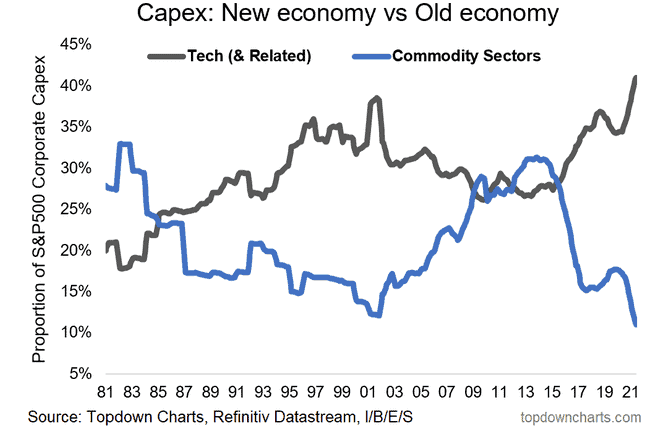

- This was all part of a major CAPEX cycle, where capital crowded into “New” economy tech/growth stocks and SBF ventures, while “Old” economy commodity stocks languished with little access to financing (chart via @Callum_Thomas).

- But the cycle is turning… Capital follows sentiment, and sentiment follows prices.

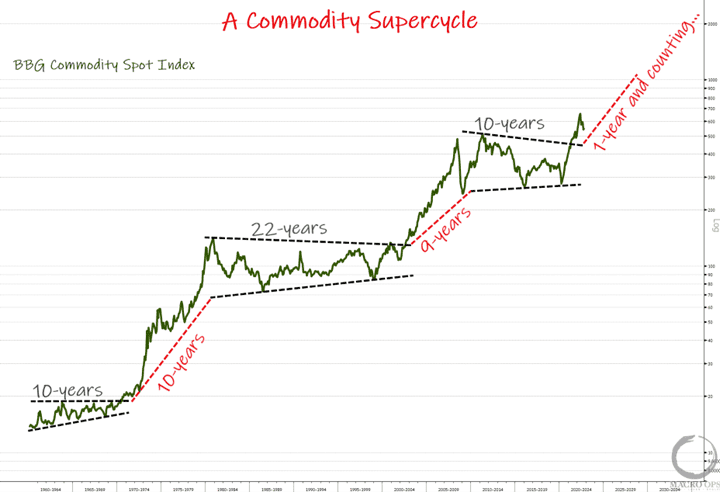

- Higher structural inflation, rising geopolitical volatility, crowded positioning in equities with negative real expected 10-year returns, the bottom of a major CAPEX cycle in commodities… Own real assets.

More By This Author:

This Is One Bad Apple…Value Investing Q3 Letter Recaps: P10, Tremor, Hagerty

Why Mexico Is Set To Outperform…

Comments

Log in or sign up to join the conversation.