Image Source: Unsplash

Sentiment slumps: consumers worry about prices, jobs and wealth

The most worrying data point this Tuesday has been the April Conference Board measure of consumer confidence. It fell from 93.9 to 86.0, weaker than the 88.0 consensus forecasts. The expectations component, which is the most important metric for guidance on the prospects for consumer spending, fell from 66.9 to 54.4. It's fair to say this is at recession levels. Meanwhile, 'current conditions', which basically follows the unemployment rate, was little changed at 133.5 versus 134.4 in March.

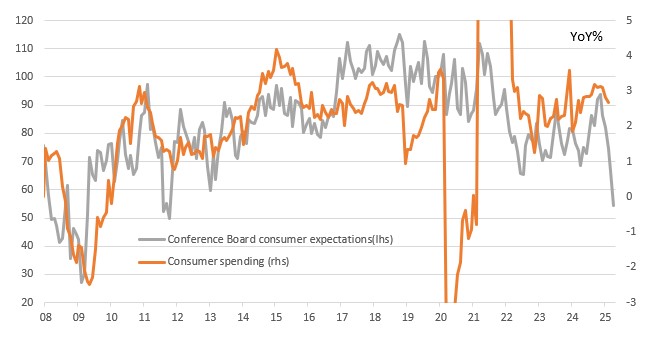

Consumer expectations and spending

Source: Macrobond, ING

Risks of outright consumer spending falls increase

The chart above shows the relationship between consumer spending growth and the Conference Board consumer expectations series. It isn’t perfect, but it paints a worrying picture of where the risks to economic growth lie.

US consumers are being hit on three fronts: prices, incomes and wealth. Households are worried that tariff-induced price rises will squeeze spending power, while government spending cuts and concerns about the outlook for the economy are prompting some angst about job prospects. With bond and stock prices falling, household wealth is declining, and that's making consumers more nervous about making big-ticket purchases.

Given that consumer spending accounts for close to 70% of US economic activity, this is clearly a concerning situation. While the Federal Reserve will be constrained from rate cuts in the near term due to tariff-induced price hikes and potential supply chain disruptions adding to inflation pressures, there will be growing pressure to cut interest rates meaningfully later in the year.

Net trade risks dragging 1Q GDP into contraction territory

As for tomorrow’s first quarter GDP print, the March advanced goods trade deficit heightens the chances of economic contraction. It came significantly wider than predicted at -$162bn versus the consensus -$145bn. Remember we had been averaging around -$100bn per month through much of 2024. Clearly, importers have been trying to get as many products into the country as they can before tariffs hit, with the result set to be a huge drag on GDP growth in 1Q 2025.

We had hoped that investment spending would be strong enough to generate a +0.8% annualised outcome in the knowledge that consumer spending and government spending would be subdued, but we are far less confident about that now. All sectors have seen a big increase in imports, but it is consumer goods that are responsible for most of the move. In March last year, the US imported $66.1bn of consumer goods, which increased to $103bn this March. Industrial supplies have increased $20bn to $74.6bn versus March last year, but for autos, it is a relatively modest $3bn increase. This perhaps suggests that with less of an inventory build we will see the impact of tariffs on pricing feed through more quickly in the auto sector than elsewhere.

More By This Author:

Italian Business And Consumer Confidence Deteriorate In AprilFX Daily: Hopping From Tariffs To Data

Rates Spark: Kicking Off A Data-Driven Week

Comments

Log in or sign up to join the conversation.