Commercial & Industrial Loans Are In The Danger Zone

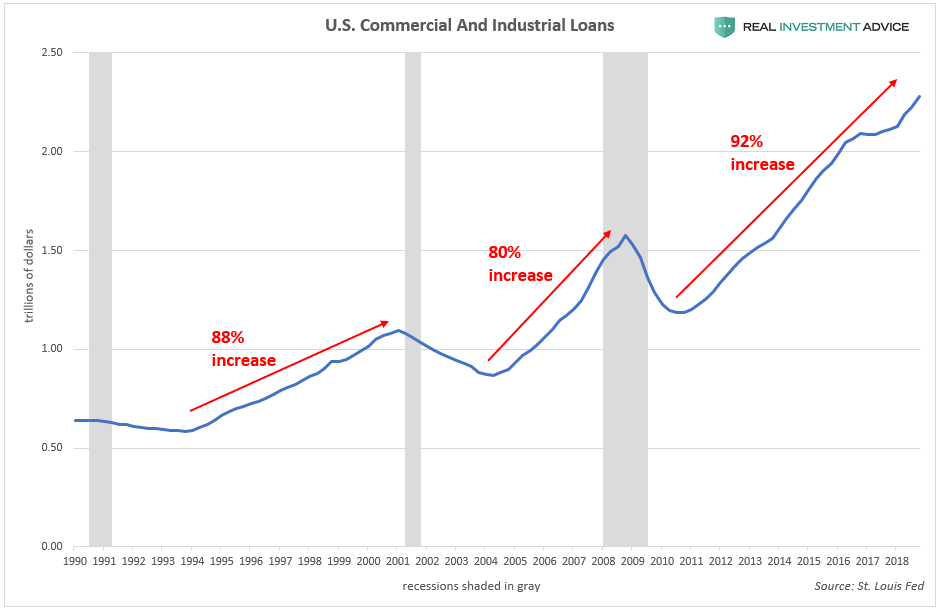

Commercial and industrial (C&I) loan activity is watched closely by economists to gauge the strength of the economy and estimate where we are in the business cycle. C&I loans are used to finance capital expenditures or increase the borrower’s working capital. The C&I loan cycle often takes up to a couple of years to turn positive after a recession, but provides even more confirmation that an economic expansion is underway. For example, the U.S. Great Recession officially ended in June 2009, but the C&I loan cycle didn’t turn positive until late-2010. C&I loans also help to warn when the economic cycle is approaching its end (as they are now).

Total outstanding U.S. commercial and industrial loans have increased by 92% in the current cycle, which surpasses the 80% increase during the mid-2000s cycle and the 88% increase during the late-1990s cycle:

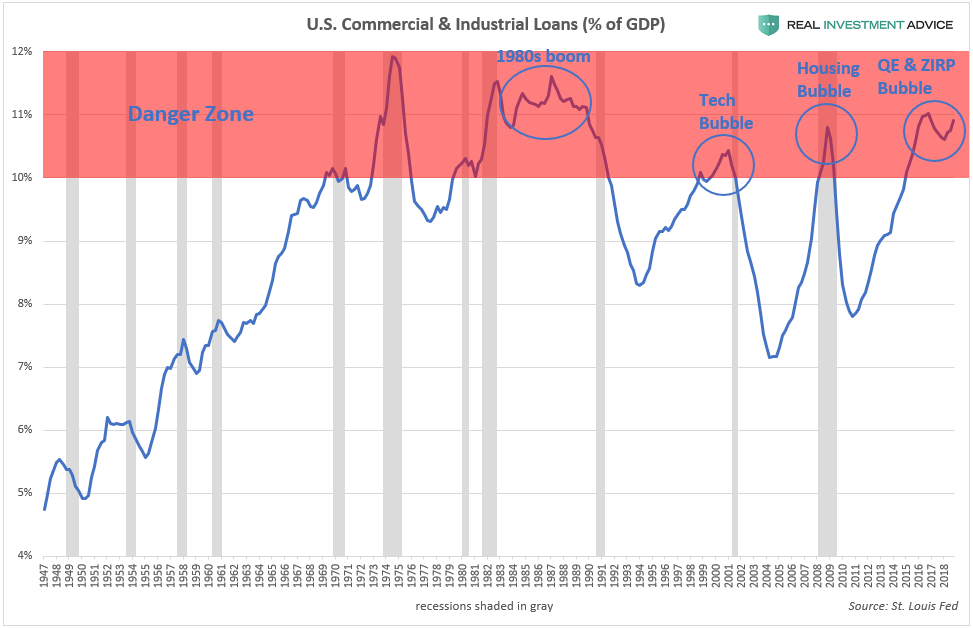

One way of determining when the C&I loan cycle (and, therefore, the overall economic cycle) is nearing its end is by charting total outstanding commercial and industrial loans as a percentage of GDP. When C&I loans are at 10% of GDP or higher (the “Danger Zone”), that is typically a sign that the cycle is long in the tooth and about to tip over into a recession. According to the chart below, recessions occurred shortly after C&I loans peaked within the “Danger Zone.” C&I loans are currently in that zone, which I see as further confirmation that we are in a Fed-driven economic bubble that will end badly.

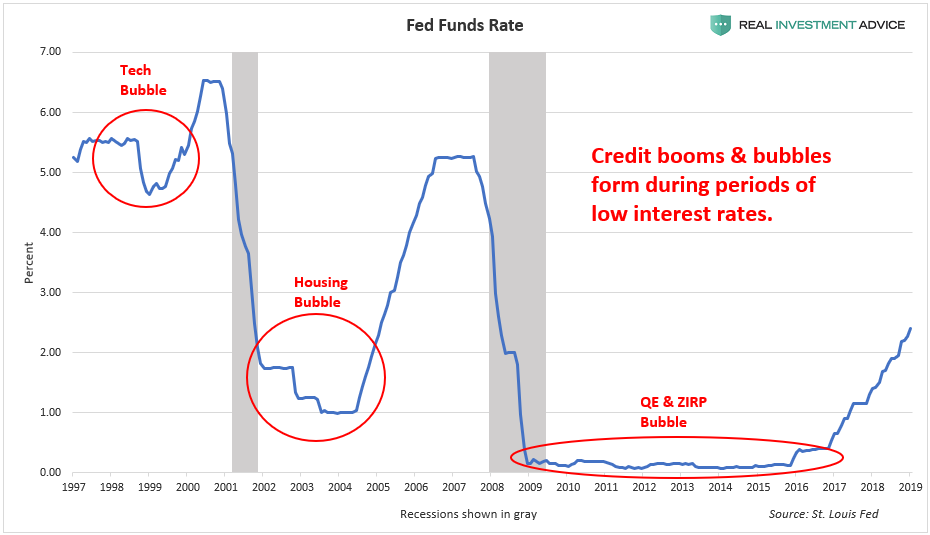

The current C&I loan cycle has been more powerful and longer-lasting than the prior two cycles because the Fed has held interest rates at record low levels for a record length of time. As the chart below shows, credit booms and bubbles form during low interest rate periods (low interest rates encourage borrowing):

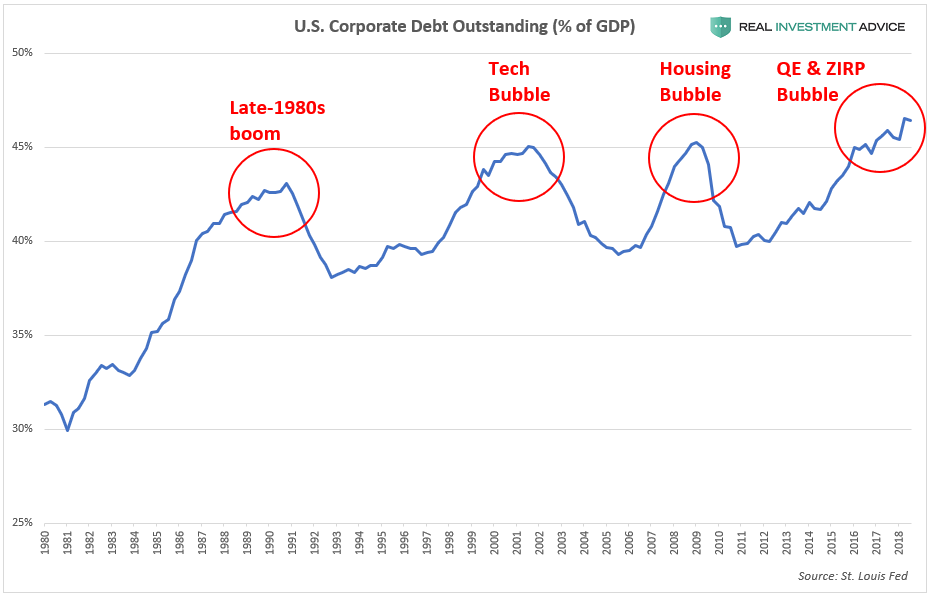

The U.S. corporate debt market (which is mostly in the form of bonds instead loans) is telling a similar message as commercial and industrial loans, as I recently discussed. To summarize, ultra-low bond yields over the past decade have encouraged a corporate borrowing bubble that has also been funding the stock buyback boom. As a result, total outstanding U.S. corporate debt has increased by $3 trillion or 45% since the last peak in 2008. U.S. corporate debt is now at an all-time high of over 46% of GDP, which is even worse than the levels reached during the dot-com bubble and mid-2000s housing bubble.

I am fully aware that both C&I loans and corporate debt may reach a higher percentage of GDP in this cycle due to how low interest rates are. Still, it is important to be aware of the risks that are building up and not be complacent. When the Fed and other central banks hold interest rates at low levels, they create market distortions and encourage malinvestment or unwise lending decisions that would not otherwise occur in a normal interest rate environment. These malinvestments are revealed once interest rates are raised and the economic cycle turns (read my piece about this in Forbes). A tremendous amount of malinvestment has accumulated after a decade of artificially low interest rates, which is going to result in serious pain when the cycle inevitably turns – make no mistake about that.