German 10Y yields climbed above zero for the first time since May 2019 just as money markets brought forward bets on a 10-basis-point European Central Bank rate hike to September from October previously. Traders expect that by the end of next year, the policy rate will no longer be negative.

But, as Bloomberg's Ven Ram notes, the key things to watch out for will be how sustainable the move is, how much of a tightening in financial conditions the ECB will tolerate (it may yet take a sanguine approach if Treasury yields continue to trek higher) and where the near-term top for yields is (my expectation is around 0.15%-0.20% -- though this isn’t a year-end target). It would be a surprise if the ECB were to allow bund yields to climb all the way to where they need to be. Notice also that the 10-year swap rate is around 0.41%, closer to the implied level on bunds.

However, the two-year yield is still trailing the benchmark deposit rate. That nonchalance at the front end of the curve may yet continue given that the ECB is unlikely to raise rates this year, setting us up nicely for further curve steepening.

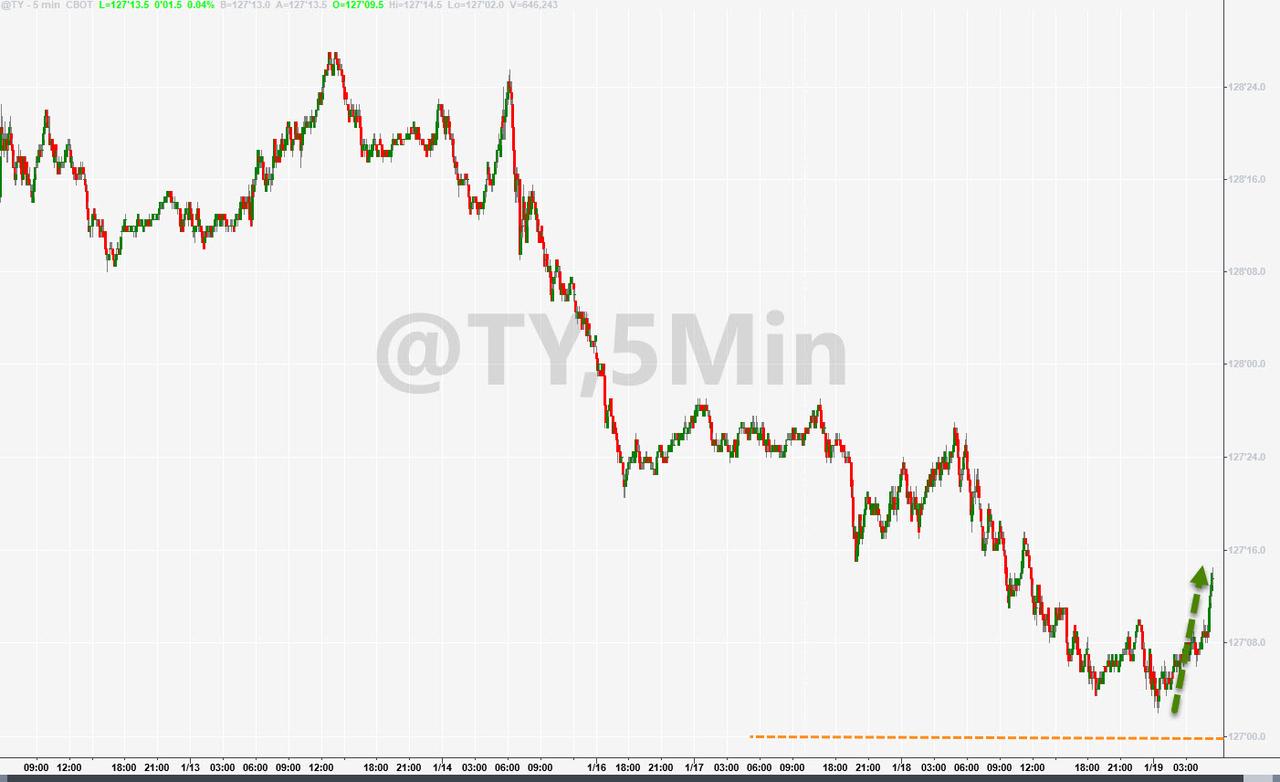

Meanwhile, US Treasuries are suddenly bid - after some weakness overnight - as the 10Y Future tagged the $127 level we warned about yesterday as critical and reversed rapidly.

As Nomura's Charlie McElligott noted: the most critical security “level” in global markets right now is 127 in UST 10Y Treasury Futs (TYH2), because the Street is short just a massive amount of downside struck there in TYH2 Puts, with 321,729 of OI (while we continue blowing-through downside strikes of all levels, most notably the TYH2P 127.5 level and its 140,579 of OI and the 128 strike’s 105,818 of OI); if that 127 level goes, the potential for a “short gamma / negative convexity” event grows substantially on Dealer hedging “accelerant” flows.

And that reversal (from 1.90% - which is equiv to $127 in Futs) is accelerating...

Is this a pause that refreshes in the rates surge?

“It’s a done deal that 10-year Treasuries hit 2%, but the selloff is likely to slow for a bit then,” said Damien McColough, head of fixed-income research at Westpac Banking Corp. in Sydney.

“Yields will definitely go higher still once the Fed delivers its first hike.”

However, an extended spike in yields could spur the Fed to move to reassure markets, according to Resona Asset Management.

“I don’t expect 10-year U.S. Treasury yields to keep rising on and on beyond 2%,” said Mamoru Shimode, chief strategist at Resona.

“That’s unlikely to be something that the Fed will tolerate.”

Everyone and their pet rabbit is short bonds here, so perhaps the pain trade in the short-term is indeed lower in yield.

Comments

Log in or sign up to join the conversation.