Between Blackrock And A Hard Place

An excellent ETF.com article on September 22 “NYC Comptroller: Blackrock ESG Standards Alarming” highlighted a very public effort by Brad Lander to shame Blackrock into being more environmentally conscious.

New York City Comptroller Brad Lander demands the company bolster its climate disclosures and publish a plan that establishes its commitment to net-zero greenhouse gas emissions across all assets they manage. The same article highlights the fact that BlackRock (BLK) has also lost accounts with state pension funds, coming under fire by no less than 19 Republican Attorneys General accusing the firm of collaborating politically with climate activists instead of siding with clients.

I was quoted in the article characterizing the extent to which Blackrock was in a no-win situation by being singled out by both sides ostensibly because it is the largest asset manager in the world. I stated “…I think trying to demand that it [Blackrock] does not accept any customers who want exposure to those fields is absolutely beyond the pale.”

The origins of these assaults on BlackRock begin with the term ESG itself. For those not familiar, ESG stands for Environmental, Social and Governance. It was intended as a way of specifying the main principles of aligning investments with beliefs in a better world known as Socially Responsible Investing (SRI). Unfortunately, terms have been tossed about and confused so much that it is unclear to many people what ESG is and what it isn’t.

Among those of us trying to provide differentiation, there is a loose agreement that there are three major categories of responsible investing:

- ESG Investing when properly defined is using ESG ratings for risk management; specifically screening out companies that score poorly on a checklist of best industry practices; ESG investing of this type does NOT eliminate industries such as Oils-Integrated or Alcohol;

- Sustainable Investing begins with the screened list of companies omitting those with the worst ESG scores. Then it further screens out companies involved in industrial practices that are deemed harmful for the future of the planet. This can be interpreted in different ways but generally focuses on environmental concerns;

- Impact Investing characterizes ETFs most specifically designed to align investors’ personal values with their investments. Themes here can run the gamut from green energy to evolving technologies to social justice, etc. These tend to be narrower and more individual-investor oriented than the ETFs in the first two categories. They are designed for long-term investors who want to invest in companies trying to make an impact on society for a better world.

In 2006, iShares became the first company to offer an ESG ETF, DSI, an index created by a firm called KLD Research and Analytics. That was three years before Barclay’s Global Investors and the iShares were sold to Blackrock making the latter the largest asset manager in the world.

Since being acquired by BlackRock, iShares has been the leader among ETF issuers in providing a multitude of responsible investing options. Today, there are 35 iShares that fit the Responsible Investing Category. It also has been attempting to provide ETFs that meet the disparate objectives of different investment constituencies.

Their core institutional series include 7 ETFs branded “ESG Aware” fitting the definition category #1 above. These ETFs use ESG ratings to weed out the lowest scorers in each industry sector of other relevant groupings. No entire industries are screened out. The broadest based US ETF and the ESG ETF with the highest assets under management by far is MSCI USA ESG Aware Index ETF. ESGU is its ticker symbol. Shares also provides two other naming conventions they use for broad-based US Equity ETFs, “ESG Select”, SUSA, first screens out companies engaged in “unsustainable practices” such as companies engaged in carbon-based energy practices before employing a similar screen to weed out the stocks of companies with the lower half of ESG scores in each industry group. Please note that the first three letters in this ticker are “SUS” for sustainable rather than “ESG.” Even more stringent screens and standards for inclusion are applied to the MSCI USA Extended ESG Leaders ETF, SUSL.

Impact investing is frequently also referred to as a subset of thematic investing by the larger ETF issuer community, but I think that may be misleading. Thematic ETFs are generally tactical tools that institutional trading desks, RIAs and individuals may use for opportunity deployment until a market cycle or trend falls out of favor. Impact ETFs, constructed to align investment dollars with underlying values are viewed as long-term commitments to investing in a better world. iShares offer 8 ETFs fitting this category, the largest of which is ICLN, iShares Global Clean Energy ETF.

Sector, industry and factor-tilted ETFs altogether come pretty close to defining tactical thematic investing. It is tactical deployment of part of one’s overall equity allocation for the period of time that the investor thinks that sector, industry or factor will be in favor.

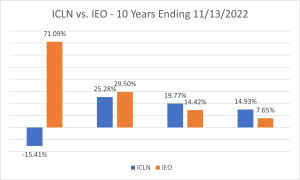

The iShares impact ETF with the longest history is ICLN, iShares Global Clean Energy ETF. Even after enduring a -15.4% return for the past 12-months. One iShares ETF that can be thought of as ICLN’s antithesis is IEO, iShares U.S. Oil & Gas Exploration & Production ETF. The companies in this ETF include Conoco Phillips (18.7%) and EOG (9.5%). They epitomize the expression “Drill, baby, Drill".

Please note that iShares’ website provides the exact same materials for IEO as ICLN. Excluding leveraged ETFs, IOH was one of the top five returning ETFs during the past 12 months. For various reasons, many tactical and thematic investors, purchased IOH during this period and were rewarded with a mammoth 71% return.

The chart above not only delineates the difference between ICLN and IEO in returns during four different time frames during the past ten years. It also illustrated the difference between impact investing and tactical investing in terms of time horizon. IEO posted negative returns in 6 of the past 10 years. It cycles in and out of favor. Ultimately, however, most of the world anticipates that after 2035, the demand for oil will decrease incrementally given global nations’ commitments and improving clean energy technology. Commonly, thought leaders refer to the future of oil reserves as stranded assets. If true, there will be little if any need for companies such as EOG, an entire business built on oil exploration and drilling; it would not be a stock anyone with a long-term buy-and-hold investment philosophy.

Alternatively, impact investors invest in ICLN because they want to align investment returns with their personal values and beliefs in a better future for the world. They feel that by doing this, they provide more capital for “good” companies and restrict capital going to old energy companies. ICLN is a long-term investment geared for buy-and-hold investors. Its 5-year annualized return 70% higher than that of the S&P 500. Its 10-year annualized return of nearly 15% also outperformed SPY substantially while coming close to doubling that of OIH. So, impact investing is not about giving up the opportunity for superior returns. It’s about not worrying about short-term market cycles while sticking with personal convictions and believing that returns will be at least as good if not better in the long-term by investing in corporate leaders doing the right thing for the future of the world.

This week’s analysis six ESG ETFs and SPY, the SPDR S&P 500 Index Trust. Four of these ETFs chosen are iShares sponsored by Blackrock presented in order of increasingly stringent ESG selection criteria. The other two, ESMV and NULV have factor tilts, minimum volatility and value respectively, overlaid on simple ESG screens.

DSI, iShares MSCI KLD Social 400 Index is a socially conscious ETF with reasonably market-like exposure. The fund limits its holdings to firms deemed to be socially responsible, from an environmental, social, and governance (ESG) standpoint. It excludes stocks of companies significantly involved with weapons manufacturing, "vice" products, nuclear energy and genetic modification. Those firms that make the cut are ranked according to ESG criteria

ESGU, MSCI USA ESG Aware Index ETF attempts to maintain tight tracking to the broad MSCI USA Index (a benchmark similar to albeit somewhat larger than the S&P 500). Companies in the broad index are rated based on ESG factors. Portfolio optimization software is then used to maximize the funds’ stake in highly-rated companies while staying true to a market-like exposure.

SUSL, MSCI USA Extended ESG Leaders Index, also starts with the MSCI USA Index, then removes firms involved with major business controversies as well as companies engaged in tobacco, alcohol an, gambling, nuclear power and certain weapons. As the ‘extended’ version of the MSCI ESG Leaders Index, the fund further excludes producers and major retailers of firearms. Firms passing this screen are assigned with an ESG score with adjustments for sector and cap weight. The fund removes firms with lower rankings.

USXF, MSCI USA Choice ESG Screened Index, invests in US equities with above average ESG ratings relative to its sector peers. The underlying index starts with the MSCI USA Index (the parent) and excludes companies engaged in controversial activities like nuclear weapons, genetic engineering, palm oil, private prisons, and predatory lending. Firms in the energy sector per GICS methodology, including those involved in fossil fuels, reserve ownership, related revenues and power generation are also excluded, with the exception of firms having bulk of their revenues tied to alternative energy. The remaining companies are ranked based on a sector-specific ESG Key Issues (e.g. carbon emissions) selection and weighting model, only those with above average scores (BBB and up) are selected. The market cap-weighted index is reviewed quarterly and excludes small-cap firms.

ESMV, MSCI USA Minimum Volatility Extended ESG Reduced Carbon Target Index provides exposure to large- and mid-cap US stocks that have low volatility, reduced carbon exposure, and positive ESG characteristics. The fund then applies an optimizer to select and weight securities, aiming to achieve lower volatility and better ESG qualities relative to the parent index.

NULV, TIAA ESG USA Large-Cap Value Index is sponsored by Nuveen which acquired asset manager and index provider TIAA-CREF in 2018. It has been chosen partially because it has a value tilt and a longer history than any of the iShares ESG ETFs with factor tilts. NULV selects large-cap stocks from the MSCI USA Value Index which itself selects value stocks according to price/book, forward price/earnings, and dividend yield. From there, NULV screens out companies involved in controversial businesses, such as alcohol, weapons, nuclear power, and gambling. Companies that exceed carbon emissions thresholds are also excluded. The portfolio is weighted according to a multi-factor optimization algorithm.

SPY, the SPDR S&P 500 Index Trust ETF mimics the S&P 500 index.

The table below provides summary data as of Nov. 13, 2022, for analysis.

|

|

DSI |

ESGU |

SUSL |

USXF |

ESMV |

NULV |

SPY |

|

MSCI KLD Social 400 Index |

MSCI USA ESG Aware Index |

MSCI USA Extended ESG Leaders Index |

MSCI USA Choice ESG Screened Index |

MSCI USA Minimum Volatility Extended ESG Reduced Carbon Target Index |

TIAA ESG USA Large-Cap Value Index |

SPDR S&P 500 Index Trust ETF |

|

|

ValuEngine Rating |

2 |

3 |

3 |

4 |

3 |

2 |

3 |

|

VE Forecast 3-mo. Price Return |

1.75% |

1.85% |

1.83% |

1.85% |

2.28% |

1.76% |

1.86% |

|

VE Forecast 6-Mo. Price Return |

4.46% |

4.43% |

4.6% |

4.53% |

5.15% |

4.32% |

4.52% |

|

VE Forecast 1-yr. Price Return |

-1.97% |

-1.73% |

-2.15% |

-1.67% |

-2.10% |

-3.86% |

-2.29% |

|

Largest Sector Weight (%) |

Comp. & Tech. 33.4% |

Comp. & Tech. 28.4% |

Comp. & Tech. 30.1% |

Comp. & Tech. 34.8% |

Comp & Tech. 20.4% |

Finance 22.1% |

Comp. & Tech. 28.6% |

|

Largest Holding |

Microsoft (MSFT) 9.5% |

Apple (AAPL) 6.7% |

Microsoft (MSFT) 9.9% |

Microsoft (MSFT) 10.9% |

Gilead Scienced (GILD) 1.9% |

JP Morgan Chase (JPM) 2.2% |

Apple (AAPL) 6.7% |

|

Last mo. Price Return |

12.25% |

11.65% |

11.70% |

13.39% |

10.56% |

13.85% |

11.40% |

|

Last 3 mo. Price Return |

-6.30% |

-5.49% |

-5.68% |

-5.29% |

-2.81% |

-1.31% |

-5.11% |

|

Historic 1-Yr. Price Return |

-18.71% |

-16.50% |

-17.40% |

-19.64% |

-8.74% |

-10.69% |

-14.07% |

|

Historic 3-Yr. Price Return |

9.12% |

9.99% |

8.99% |

N/A |

N/A |

3.34% |

10.03% |

|

Historic 5-Yr Ann. Price Return |

8.20% |

8.40% |

N/A |

N/A |

N/A |

4.14% |

8.13% |

|

Volatility |

18.8% |

18.9% |

20.0% |

20.0% |

19.5% |

18.6% |

18.6% |

|

Sharpe Ratio |

0.44 |

0.44 |

0.40 |

N/A |

N/A |

0.22 |

0.44 |

|

Beta |

1.01 |

1.02 |

1.00 |

1.04 |

0.83 |

0.95 |

1.01 |

|

# of Stocks |

398 |

312 |

278 |

363 |

162 |

100 |

500 |

|

% of Stocks Undervalued by VE |

29.4% |

20.8% |

26.3% |

25.6% |

18.8% |

25.6% |

22.4% |

|

P/B Ratio |

4.2 |

3.6 |

4.3 |

4.1 |

4.5 |

2.2 |

3.8 |

|

P/E Ratio |

18.7 |

17.3 |

20.1 |

20.5 |

21.8 |

14.0 |

17.4 |

|

Div. Yield |

1.3% |

1.7% |

1.6% |

1.4% |

1.5% |

1.9% |

1.6% |

|

Expense Ratio |

0.25% |

0.15% |

0.10% |

0.10% |

0.18% |

0.25% |

0.09% |

Analysis

- Of the iShares ETFs, ESGU has by far the highest amount of Assets Under Management and is easily the most institutionally constructed to resemble the broad stock market and it does. On a sector weight breakdown, it is very similar, including the same 6% weight in the Energy sector. For all the hue and cry over underperformance vs. outperformance, the differences in price return have been relatively modest. On a one-month basis, ESGU outperformed by 0.25% while SPY outperformed by 0.39% on a three-month basis. For the 12-month period, ESGU registered its largest underperformance of 2.43% but outperformed on a 5-year basis by 0.27%. For the 3-year period, it is a dead heat. In short, ESGU is a way of investing in companies that follow best governance, social and environmental basis proactively while disinvesting in the laggards in each category. Of pension funds that elect to be ESG-conscious, ESGU and Blackrock’s separately managed accounts with the same objectives account for the lion’s share of these assets. From a fiduciary standpoint, there is no statistical evidence that ESGU will underperform systematically, and it is therefore prudent to avoid firms that are below the median in adopting best practices. There also no evidence of outperformance that would make it imprudent not to do so. The relatively small periods of underperformance and outperformance tend to be cyclical.

- DSI, the following an index sometimes referred to as “the grandfather index” of SRI, has systematically underperformed AND has a higher expense ratio. This is often true of legacy ETFs. I have written before why it makes little sense to buy new shares of GLD (SSgA Gold Trust) when GLDM is available at less than half the fee. Another example applies to SPY which is included here for familiar comparison but systematically underperforms Vanguard’s VOO following the same exact index by about 0.13% per year. While not identical portfolios, I would say the same about buying new shares of DSI. It’s systematically more cost-effective to buy shares of ESGU. It also has a lower ValuEngine Rating of 2, a recommendation for investors to consider selling shares of DSI.

- SUSL can be thought of as a more environmentally conscious version of ESGU with no exposure to carbon-based fuels. Since the last two years were the best since the 1970’s for companies involved in providing them, it is not surprising that aligning beliefs in net-zero-carbon long term by investing in sustainable leaders would lead to greater underperformance during the past two years. Since SUSL was started in 2019, it doesn’t yet have five years of history so we cannot measure whether the underperformance of those old energy stocks from 2017 – 2020 would have been strong enough to make up for its 5-year deficit relative to SPY. That said, sustainability goals are long-term. Spokespeople for these funds often advise that they are for long-term investors seeking to align investments with values, not for quarter-to-quarter comparisons with market performance.

- The same comparison would apply to USXF following the MSCI USA Choice Index with even more stringent environmental and social requirements. Interestingly, USXF is the only one of these responsible investing ETFs rated a 4 (buy recommendation) by ValuEngine’s predictive models. Its relatively short history may concern investors looking for long-term validation.

- Alternatively, both factor-tilted ESG ETFs show portfolio constitution risk profiles and performance histories significantly different from SPY. One difference is that neither ESMV nor NULV are market-cap weighted. Both also have far less allocation to technology. As one might expect, ESMV, an ESG-compliant ETF constructed to minimize price volatility, underperformed the market and the more market-like ESG ETFs during the 10+% month-long rise but outperformed during the three-month and twelve-month periods. Knowing that value stocks have outperformed their counterparts during the past 12 months, the significant outperformance relative to SPY of Nuveen’s value-factor-tilted NULV should come as no surprise. NULV also offers the highest yield and best traditional value statistics of all the stocks in the sample. Since value greatly underperformed growth during the 2018- 2020 period, NULV’s poor relative performance in the three- and five-year compounded periods also makes sense. Most asset managers employ factor-tilted and sector ETFs tactically understanding that their returns are directly tied to market cycles. These two examples substantiate the fact that factor tilts will influence annual performance far more than ESG screens and ratings.

Conclusion

ESG investing is about due diligence in weeding out the firms within each industry that are laggards at adopting best management practices. Performance comparisons in studies I’ve performed and reviewed demonstrate clearly that this type of investing will underperform during some cycles and outperform during other cycles and will generally perform in line with non-ESG-screened market indices over ten-year or longer periods of time.

Sustainable investing, eliminating companies engaged in practices considered bad for the environment, will be somewhat more cyclical as they are attempting to own companies committed to sustainable future leadership. They are more suitable for investors that can take ten-year views than investors who must be concerned with quarterly and annual performance.

Factor-tilted ESG portfolios will have significant differences quarter-to-quarter that tend to be more influences by whether that factor is in favor than the ESG ratings used to screen out holdings and/or included in the underlying portfolios’ weighting schemes.

The political backlash against ESG in general and Blackrock and TIAA-CREF in particular seems to be just that, political. The most mystifying part to me personally is why Blackrock is the focal point for anti-ESG and pro-ESG investors. As with SSgA, Vanguard, Goldman Sachs, American Century, etc., they offer everything their investors may want. This includes ESG, Sustainable and Impact investing options. It also includes Energy Sector and industry ETFs including one that holds the companies of oil drillers. It is true that CEO Larry Fink and Blackrock materials have been a bit more explicit about issues such as board diversity and a more sustainable future. It is also true that SSgA, TIAA-CREF and others have also done so. Why put a target on Blackrock? As far as I can see, it is only because they are the biggest that both sides have put Blackrock in such a hard place.

More By This Author:

Communications Services: Meta Vs. AT&T

Opportunities In Large Cap Growth And Small Cap

Bank Stocks And ETFs In A Rising-Rate Environment

Disclaimer: Always read the fact sheets and/or summary prospectus before buying any ETF. Do your own research. Past performance may not be indicative of future results.