Image Source: Unsplash

Risk-taking wanes

The primary driving force behind the strong dollar is the looming spectre of enduring monetary policy divergence.

Oil market Time Structures seldom lie.

MARKETS

Thursday marked the fifth consecutive session of decline for US stocks as optimism regarding multiple interest rate cuts by the Federal Reserve waned.

The downturn in sentiment can be attributed to robust economic data releases, prompting traders to adjust their expectations for multiple rate cuts this year. Indeed, as financial conditions tighten, speculative jitters heighten, engulfing investors in a billowing cloud of apprehension.

Asian stocks are poised to decline, following the footsteps of US shares and Treasuries, which extended their downward spiral.

Of course, Asia investors aim to salvage a challenging week; however, prevailing global unease and a cautious attitude towards risk-taking ahead of the weekend ( Yes, the Middle East is still on the radar), compounded by relentless waves of hawkish fed speak, could limit any appetite for upside moves.

On the macro front, attention now turns to next week's release of first-quarter gross domestic product (GDP) data, which will provide insight into the strength of the US economy and likely influence market sentiment.

The Atlanta Federal Reserve Bank's GDPNow indicator suggests that the U.S. economy expanded at a 2.9% annualized rate in the first quarter. This growth was primarily propelled by consumer and government spending and an expanding labour force, which is unlikely to spring a pressure valve release.

Last week, the standout release from the world's largest economy was particularly notable. Nominal spending surged, nearly doubling initial estimates, while retail sales displayed even greater strength. Moreover, the control group, a critical indicator, demonstrated a remarkable 1.1% increase, nearly quadrupling the anticipated gain. These robust figures are expected to bolster first-quarter GDP estimates in anticipation of the upcoming advance read on overall growth next week.

The greenback remains strong, having rallied by 3% recently to reach its highest level since November.

Meanwhile, U.S. bond yields continue to rise, marking their third consecutive weekly increase. The 2-year Treasury yield has rebounded to 5%, while both the two- and 10-year yields have surged by 40-45 basis points in the past few weeks.

One silver lining amidst these developments is the easing of oil prices from their recent highs.

OIL MARKETS

Oil futures continued their decline on Thursday morning following the release of the Energy Information Administration's report, which revealed a larger-than-anticipated increase in U.S. crude oil inventories. According to the EIA, commercial crude oil stockpiles in the U.S. rose by 2.7 million barrels in the week ending April 12. Despite draws of 4.7 million barrels in gasoline and distillate inventories, total commercial petroleum stocks surged by 10 million barrels last week. This increase was driven by crude oil builds, a 1 million barrel rise in jet fuel stocks, and a notable 7.5 million barrel surge in "other oils" stocks. The clear read-through is that demand is not as rosy as thought and that demand destruction, due to soaring prices at the pump, could be setting in even as we head for summer driving season.

The decline in oil futures has erased all gains made since the Israeli attack on an Iranian consulate on April 1. Additionally, the time structure of futures contracts suggests that concerns over near-term threats to oil supply have diminished. The forward curve for Brent crude, which seldom lies, has flattened since early April, with the prompt spread dropping back below $0.60 per barrel from $1.07 per barrel.

FOREX

The USD's resurgence as a global concern echoes a scenario I wrote about two weeks ago: "duelling currency wrecking balls." Observations from the IMF-World Bank meetings in Washington hint the dollar's unyielding strength emerged as the central issue, drawing serious apprehension from officials, particularly in Japan and South Korea, where persistent currency devaluation has become a source of frustration.

Janet Yellen's acknowledgment of the "serious concerns" expressed by Japanese Finance Minister Shunichi Suzuki and South Korean Finance Minister Choi Sang-mok culminated in a joint statement. This statement, perceived as a signal for potential intervention, received cautious optimism from market participants. Masato Kanda, Japan's FX overseer and highly regarded in market circles, emphasized the gravity of the situation by distinguishing these concerns as "serious" rather than ordinary.

Reflecting on September 2022, a period marked by a distressing surge in dollar strength, parallels emerge, albeit not yet reaching the same severity when the world was forced to go “dialling for dollars.” Nevertheless, the prevailing strong dollar trend raises alarms, suggesting that the "US exceptionalism" trade poses escalating risks, potentially leading to significant disruptions for the global economy.

The primary driving force behind the strong dollar is the looming spectre of enduring monetary policy divergence. Specifically, while the US economy remains resilient and steadfast, it shows little sign of weakening compared to its primary G-10 peers.

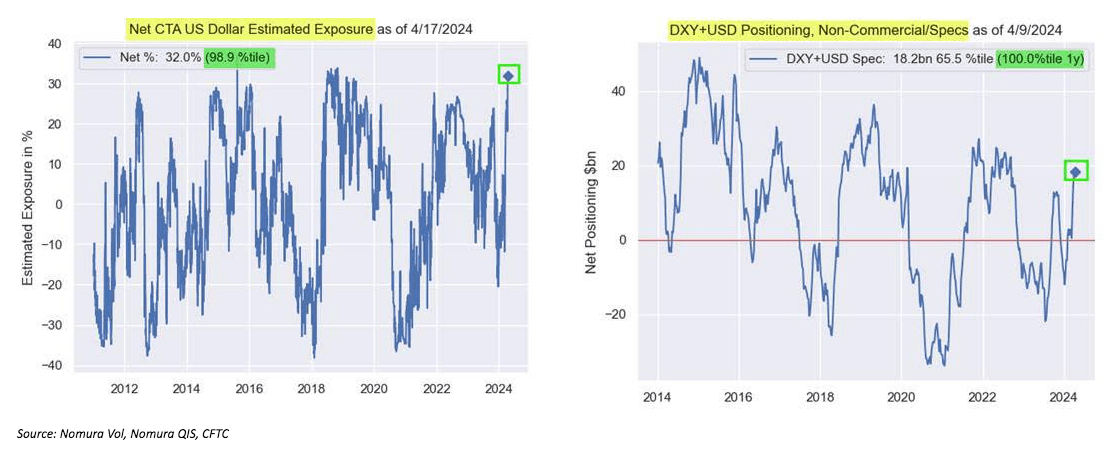

A significant worry for US dollar bulls is the apparent strain in dollar positioning. Both CTA exposure and CFTC net long figures suggest stretched positions. To elaborate, the CFTC net long positions are currently at the 100th percentile based on a one-year lookback period, while CTA exposure is approaching comparable extremes over a longer duration.

Simply put, this situation suggests a potential reversal, namely a pullback, in the event of coordinated intervention or any dovish US macro catalyst.

However, regardless of what unfolds in the immediate future, it's improbable that this will entirely undermine the multi-level case for a strong US dollar. Instead, intervention might offer the opportunity to buy into the US dollar at more favourable levels.

The US dollar appears remarkably resilient, almost impervious, amidst a notable global growth divergence.

Moreover, capital continues to flow into the allure of US exceptionalism, particularly given the proximity to US tech/AI companies, which are perceived as engines of perpetual growth. A newfound penchant for higher oil prices further bolstered the dollar's strength.

Furthermore, amidst escalating uncertainties, there's a flight-to-safety dynamic at play. In times of heightened risk, there's an increased demand for dollars, primarily manifested through benchmark Treasuries. Notably, individuals seek cash USDs to hide under the mattress during genuine major crises, eschewing all substitutes.

More By This Author:

Netflix In Focus As Stocks Grapple With 'Higher For Longer' Mantra

US Stock Continue To Stumble As Traders Rethink Rates

Chair Powell Echoes The 'Higher For Longer' Mantra

Comments

Log in or sign up to join the conversation.