A Flatter Treasury Curve… And Slower Growth?

The spread between long and short Treasury yields has been narrowing lately, a change that some analysts see as a warning sign for US economic growth. The current numbers overall suggest that that the macro trend is sliding into the business-cycle ditch, but there’s still plenty of concern about painfully slow growth. How slow can it go before tipping into a formal recession? No one really knows, but the flatter yield curve these days is attracting attention in the wake of wobbly equity prices and mixed economic news.

“The yield curve itself signals that things are not good looking into the future and talking about recession risk,” Steve Major, head of fixed-income research at HSBC Holdings, tells Bloomberg. “The market is now ready for a long, long time with very low rates and it’s been painful because people have been expecting the Fed to do what it said it was going to do. The Fed really wants to hike rates but can’t.”

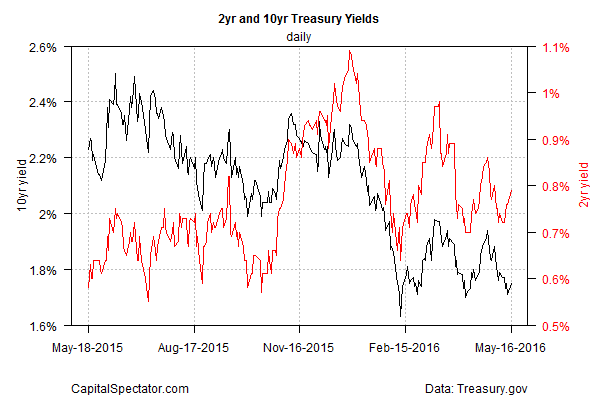

Divining the future path for the economy is loaded uncertainty, as always, but the big squeeze on the yield curve lately is still noticeable and somewhat worrisome, based on daily data via Treasury.gov. Note, for instance, how yesterday’s curve (black line) compares with its shape from a year ago (blue line). Maturities for five years and above have dropped while shorter term yields—2 years and below—have increased. The net result: the spread between short and long rates has been squeezed.

Squeezed but not inverted. The yield curve remains positively sloped, albeit less so compared with recent history. Nonetheless, there’s still a ways to go before we see an inversion, which is to say that yields aren’t predicting a recession at the moment. When/if the curve inverts, the change will trigger a widely respected signal that a new contraction is near. But long yields are still comfortably above short rates and so it’s premature to assume the worst.

The recent histories for the 2- and 10-year yields also paint less-threatening profiles vs. looking at changes in the shape of the entire curve. Although yields have fallen after the recent peaks in late-2015, Treasury rates have been relatively stable in the second quarter, albeit at moderately lower levels.

By one analyst’s reckoning, the numbers are less about an imminent downturn vs. the slow grind of a sluggish trend. In short, more of the same. “The long term suggests a scenario where growth will be slower and lower and that’s how the curve is really expressing that view,” Aaron Kohli, interest rates strategist at BMO Capital Markets explains via Reuters. It’s debatable if that’s a distinction with significance, but it’s a reasonable view–until or if new numbers lead to an attitude adjustment, for good or ill.

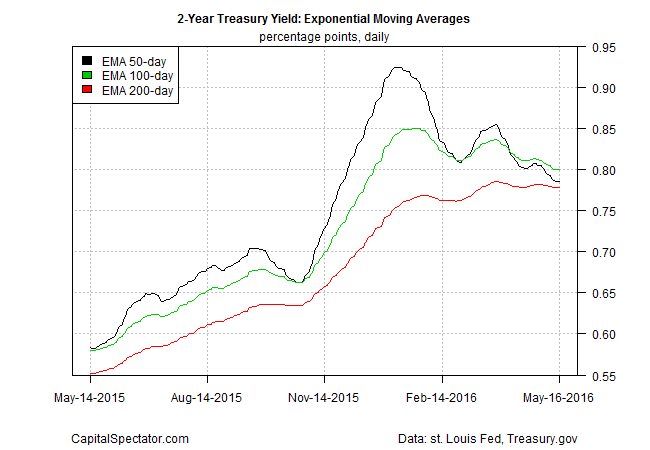

But the potential for further narrowing of the curve can’t be ruled out. Consider two clues: exponential moving averages (EMAs) for the 2- and 10-year yields. The next two charts suggest that this widely followed spread for the two maturities may continue to contract in the weeks ahead. The EMA data hints at the possibility that the 2-year has a weak but positive upward bias (although that appears set to reverse soon), which contrasts with the clear downside trend for the benchmark 10-year yield. If the implied forecasts hold, the spread between these two yields will become increasingly constricted.

At the same time, it’s reasonable to ask if the crowd is once again overstating the case for macro trouble. The Atlanta Fed’s current nowcast for GDP growth in the second quarter (as of May 13) points to a firmer pace: +2.8% (seasonally adjusted annual rate), which is considerably stronger than the stall-speed gain of 0.5% in Q1.

Forecasts should be viewed cautiously, of course, but for the moment there’s no smoking gun for arguing that the US has already slipped into an NBER-defined recession, as discussed in the May 15 update of the US Business Cycle Risk Report.The case for slow, and perhaps slower growth, remains a real and present danger, however. The question, then, is whether slow growth deteriorates into outright contraction down the line?

The preliminary numbers for April suggest that the economy continued to expand. But in a sign of the times, there’s not a lot of confidence about May’s profile, which is largely a mystery in macro terms at the moment, and beyond. The operative question until or if new numbers change the topic: How slow can it go?

Disclosure: None.

But excess bond demand is also driving long yields down. It does not necessarily mean recession. It could also mean that there are not enough bonds for collateral these days.