4 High-Yield Dividend Traps To Sell Now

I review a lot of high-yield investments. You likely are aware that an investment gets priced for a higher-than-typical yield because of the potential or possibility of a dividend rate reduction. The interesting part about a company’s decision to change its dividend is that it is a binary event. Either the dividend is cut, or it will be sustained. The goal as an investor is to find and invest in high-yield stocks that don’t cut the dividends. Dividend reductions are the landmines of income-focused investing strategies.

The pandemic triggered an economic shutdown, and related financial markets crash, has already pushed hundreds of companies with high-yield stocks into dividend cuts. Because share prices are so low, many of these stocks still have very high percentage yields.

You may think it’s safe to get back into the stocks with already-cut dividends. However, for certain types of high-yield businesses, it’s a case of once a landmine dividend stock, always a landmine dividend stock.

Dividend cuts are independent of the company’s stock price and the current yield. Just because a stock has dropped a lot—and the yield is now very high—does not automatically mean the company will cut the dividend rate.

The ability to pay dividends depends on business results and the amount of free cash flow generated by the business. The corporate board of directors determines whether the dividend will be sustained or reduced based on business results and the business future outlook.

Here are some types of businesses that are always dividend cut landmines. And one that, post-pandemic, has the potential to surprise investors with more dividend reductions.

Agency mortgage-backed securities real estate investment trusts (MBS REITs) are companies that own highly leveraged portfolios of U.S. government agency guaranteed mortgage-backed securities. These companies are classified as finance REITs. Not all finance REITs are dividend landmines. You need to look for the code words “agency MBS” and the fact the companies leverage up their equity to six times or more. Here are two popular high-yield finance REITs to avoid.

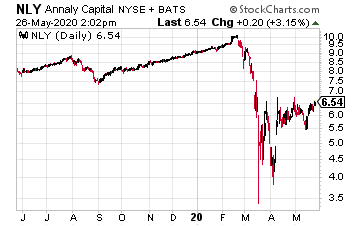

Annaly Capital Management (NLY) currently yields 14.75%.

This is a stock I get a lot of questions about from my Dividend Hunter readers.

To get the cash flow to pay the big yield, the company reported economic leverage of 6.8 times for the 2020 first quarter. For that quarter, Annaly paid a $0.25 dividend.

Unfortunately, core earnings were just $0.21 per share. In 2012, the Annaly dividend was $0.55 per share. In 2019, it was cut from $0.30 per share down to the current $25 per share. Over the past six years—but before the recent crash—the share price dropped by 41%.

Annaly is a dividend landmine with a reset button.

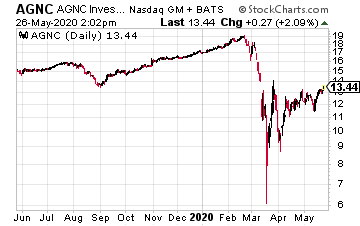

AGNC Investment Corp. (AGNC) is another agency MBS REIT. It currently yields 11.4%.

For the first quarter, AGNC reported 9.4 times “tangible net book value ‘at-risk’ leverage.” That phrase alone shows how complicated the business model is.

The company reported $0.57 per share in net spread income, against $0.48 paid in dividends. That’s a good thing. The bad thing is, the leveraged agency MBS business model always stops generating enough cash eventually.

The AGNC dividend has been cut four times in the last five years, pulling the share price down with the reductions.

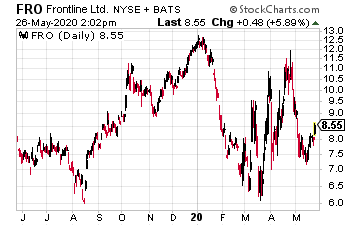

Shipping stocks are another high-yield investing landmine. Ship leasing rates are very volatile, fluctuating wildly with swings in the global economy. When rates are high, the shippers lock in those rates with multi-year contracts, and they pay out big dividends. When the leases expire, renewal lease rates are often much lower, and the dividends get slashed.

Frontline Ltd. (FRO) owns a fleet of 70 crude oil tankers used for floating oil storage.

With crude oil demand destruction, tanker rates have skyrocketed. Frontline, which paid a $0.10 per share dividend in December, and a $0.40 per share dividend in March, has declared a $0.70 dividend payable in June. The current yield based on the latest dividend is over 30%.

Investors may get a few more big dividends from Frontline, but eventually tanker lease rates will come back down—and so will the dividend.

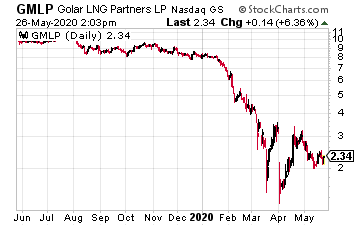

Golar LNG Partners (GMLP) owns and operates a fleet of LNG carriers and LNG floating and storage regasification units (FSRUs).

The vessels are on long-term contracts, and before the pandemic, Golar paid out almost 100% of free cash flow as a $0.4042 per share dividend.

The yield on Golar before the market crash was 17% to 18%. When the so-called “corona crisis” took down the energy sector, the Golar management took the opportunity to slash the dividend to $0.02 per share and renegotiate terms with its bondholders.

Common shareholders were left holding the bag.

Disclaimer: The information contained in this article is neither an offer nor a recommendation to buy or sell any security, options on equities, or cryptocurrency. Investors Alley Corp. and its ...

more

Not $AGNC, best agency mreit, the small cut in dividend only backs that (in these economic times).