3D Systems Corporation's (DDD) stock has been volatile over the last couple of years. The stock has been on the decline since 2021, and I believe it should continue to do so given weak demand in the dental orthodontic business and uncertainty about the regenerative medicine business.

A look into recent quarter’s financials

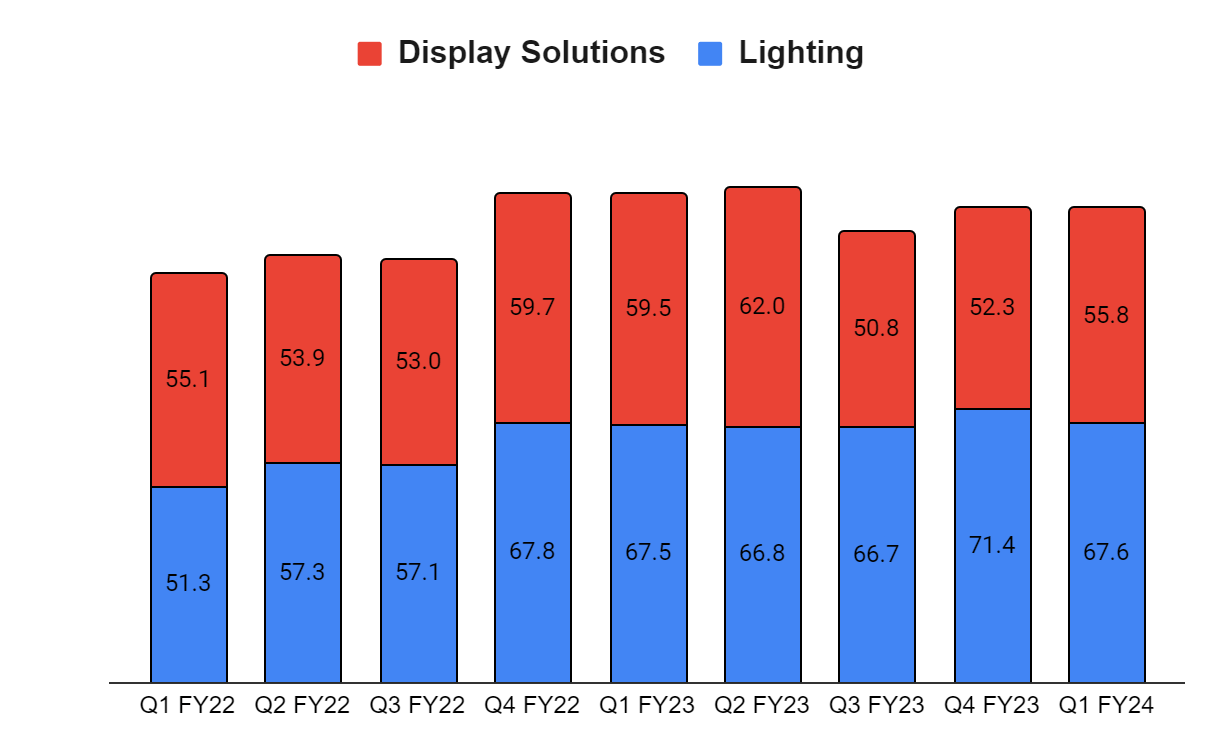

DDD recently reported lower-than-expected first-quarter FY23 financial results. The revenue in the quarter decreased by 8.8% Y/Y to $121.24 million, which is below the consensus estimates of $128.02 million. This decline was primarily attributed to the underperformance of the dental business and adverse effects from foreign exchange translation.

On a segment basis, the Healthcare Solutions segment experienced a substantial setback as its revenue plummeted by 24.3% compared to the previous year. This decline was mainly driven by the ongoing weakness in the dental orthodontic market, which experienced a significant 46% year-over-year drop in Q1 FY23. The dental orthodontic market showed promise in the first half of 2022, only to suffer a significant decline in the latter half due to unfavorable macroeconomic conditions, resulting from rising interest rates. Despite this setback, there was some positive news to be found. Non-dental markets, on a constant currency basis, saw a noteworthy increase of over 22% year-over-year in the quarter. This growth was fueled by the strength exhibited in both the orthopedic and CMS markets, offering a glimmer of hope amidst the challenging landscape. Within the Industrial Solutions segment, revenue experienced a 5.6% year-over-year upswing, bolstered by impressive performance in consumer auto and OEM, academic and research, jewelry, as well as electronics and connectors.

However, despite some positive aspects, the company's adjusted loss per share for the quarter stood at $0.09, falling short of both the prior year's Q1 loss per share of $0.06 and the consensus estimate of $0.07. The adjusted gross margin also declined by 200 basis points year-over-year, settling at 39%. This decrease can be attributed to lower overall sales volumes, lower fixed cost leverage, an unfavorable sales mix, and input cost inflation. The adjusted EBITDA took a hit as well, reaching a negative $10 million in the quarter. The decrease was a result of lower gross profit, increased R&D costs, investments in regenerative medicines, and acquisitions. Consequently, the lower adjusted EBITDA led to a loss per share for the quarter, highlighting the challenges faced by DDD in the current financial period.

What’s the near-term outlook for DDD?

The current market dynamics for DDD can be bifurcated, with one specific market being soft and the remainder being strong. Specifically, the demand for clear aligners within dental orthodontics has been significantly impacted by reduced consumer discretionary spending as inflation has led consumers to prioritize essential expenses such as food, gas, and rent. As a result, DDD's customers are scaling back their inventory levels, which had previously seen substantial growth during the COVID-19 period. Consequently, this downward trend has led to volume declines over the past few quarters.

Looking ahead, I believe that this pressure will persist for at least the next two quarters, gradually subsiding as supply chain issues and demand improve. The management's recent commentary during the earnings call supports my belief, as they anticipate a downturn of approximately 35% in the dental orthodontic market for 2023. However, on a brighter note, the orthopedic business, which constitutes half of the healthcare solutions segment, is witnessing robust demand. In fact, it achieved double-digit revenue growth in Q1 FY23, and this positive momentum should continue throughout 2023 due to heightened demand and advancements in technology within the orthopedic market.

Additionally, the Industrial Solutions segment is experiencing strong demand across various sectors such as automotive, electronics, military aviation, and space. The electronics market, in particular, is witnessing a surge in demand for electrical connectors within the additive manufacturing business. This is driven by the ability to produce a large number of parts with complex geometries.

Overall, I believe DDD's revenue growth should be in the low single digits for 2023, primarily fueled by the healthy performance of the industrial solutions business and the resilient half of the healthcare solutions segment. However, this growth is expected to be partially offset by the ongoing weakness in the dental orthodontics business.

DDD's adjusted gross margin and adjusted EBITDA margin

In terms of profitability, DDD has encountered a decline in both adjusted gross margin and adjusted EBITDA margin over the past few quarters. This decline can be attributed to various factors, including divestitures, inflationary pressure, investments in the regenerative medicine business, and lower sales volumes. To address these challenges and enhance profitability, the company recently unveiled a comprehensive restructuring initiative for 2023. This initiative aims to align DDD's European engineering and manufacturing operations for its three metal platforms, streamline the software organization, and concentrate on growth-oriented businesses. As part of this effort, DDD has also decided to reduce its workforce by approximately 6% across the entire company, a move driven by uncertain macroeconomic conditions.

The restructuring initiative holds significant potential for improving profitability in the coming year. It is expected to generate annualized savings ranging from $6.5 million to $9.5 million in 2023 and a more substantial range of $14.5 million to $18 million starting in 2024. These cost savings will contribute to the company's bottom line and overall financial performance.

Overall, I believe margins should remain flat in 2023 due to lower volumes and investments in the regenerative medicine business. This should be offset by tailwinds from moderating inflationary pressure and DDD’s restructuring initiatives.

Risks

DDD has made strategic investments in the regenerative medicine business, a sector that is currently in its pre-commercial stage. DDD formed a separate entity for this business named Systemic Bio, a wholly-owned start-up company that is leveraging DDD’s expertise in vascularized tissue printing to develop and manufacture a unique organ-on-a-chip technology called hVIOS for use in drug discovery and development by the pharmaceutical industry. While this venture presents potential growth opportunities, it is also a speculative bet that comes with some short-term challenges. The investments made in this nascent market are impacting the company's margins in the near term.

Considering the uncertainty surrounding the regenerative medicine business, there is a level of risk involved. If these investments do not yield the expected results, DDD might need to reevaluate its position and consider divesting this business. Such a decision would be aimed at redirecting resources towards alternative growth opportunities that could better support the company's financial goals.

However, it is worth noting that if DDD is forced to divest the regenerative medicine business without achieving the desired returns, it could further impact the company's margins. The process of divestiture and the search for alternative growth avenues would likely require additional costs and resources, potentially leading to a temporary compression of margins.

Overall, while DDD's investment in the regenerative medicine business presents an opportunity for future growth, the outcome remains uncertain. The company will need to carefully assess the performance of this venture and make informed decisions regarding its continuation or potential divestment. This will be crucial in navigating the impact on margins and identifying alternative avenues for sustainable growth.

Valuation

Created using Alpha Spread

Valuing 3D Systems Corporation's stock is indeed a challenging task, considering the complex dynamics of its various business segments. In my discounted cash flow (DCF) calculations, I have taken several factors into account to arrive at a fair value estimation. For the year 2023, I have assumed a low-double-digit revenue growth rate, considering the healthy demand projected in the orthopedics and industrial solutions businesses. However, this growth is expected to be partially offset by the weakness observed in the dental orthodontics business.

Looking beyond 2023, I have conservatively assumed a growth rate in the low-single digits. This cautious estimate accounts for the company's investments in the speculative regenerative medicine business, which introduce a level of uncertainty to its future growth potential. Additionally, I have factored in a terminal growth rate in the low-single digits to account for the company's long-term stability. I used a discount rate of 7.38% and arrived at a fair value of $4.83 for DDD.

Conclusion

Considering the complexities and uncertainties involved, I am giving the stock a neutral rating. While the company shows potential in certain segments, such as orthopedics and industrial solutions, the weak performance of the dental orthodontics business and the speculative nature of regenerative medicine investments introduce risks that should be carefully considered.

More By This Author:

Is Curtiss-Wright Poised To Fly High?

Albany International Corporation: Not A Buy At Current Levels

Northwest Pipe Company: Boring, But Interesting Growth Opportunities

Comments

Log in or sign up to join the conversation.