U.S. Home Prices Could Decline

The U.S. housing market has seen a significant increase in the past few years. As this happened, homebuilder stocks surged.

But beware, this might change soon. Housing prices could decline, and homebuilder stocks could face scrutiny. The rest of 2022 and early 2023 could be a very rough period for the U.S. housing market.

It almost seems that the U.S. housing market has become like a growth stock. According to the S&P/Case-Shiller U.S. National Home Price Index (a well-known and most-quoted indicator of the U.S. housing market), housing prices in the U.S. increased by more than 32% between January 2020 and January 2022. (Source: “S&P/Case-Shiller U.S. National Home Price Index,” Federal Reserve Bank of St. Louis, last accessed April 13, 2022.)

For some perspective, home prices in the U.S. increased by just a little more than 8.3% between January 2018 and January 2020. In simple terms, the increase in U.S. housing prices over the past two years was roughly four times as high as the increase in the preceding two years.

Why did home prices increase so much? As the COVID-19 pandemic began, the Federal Reserve lowered its benchmark interest rates, which caused mortgage rates to drop. Plus, many businesses moved to a work-from-home structure, so many individuals started to look for homes away from city centers, sometimes in different states. This caused a spike in demand for U.S. housing, and basic economics played out: home prices shot higher.

Interest Rates Soar While Incomes & Savings Drop

Fast-forward to now. The tide has been turning; there could be several headwinds for the U.S. housing market and housing-related investments.

First of all, many of the businesses that switched to work-from-home operations during the pandemic have started to bring their employees back to their offices. Surely, a decent number of businesses completely switched to work-from-home structures, but many didn’t. With this, one has to ask: what will happen to the prices of homes in suburbs? And what will happen to the prices of homes in city centers?

Furthermore, inflation in the U.S. economy has been rampant lately. To fight it, the Federal Reserve has started to raise interest rates. As the Fed has raised interest rates, mortgage rates have started to skyrocket.

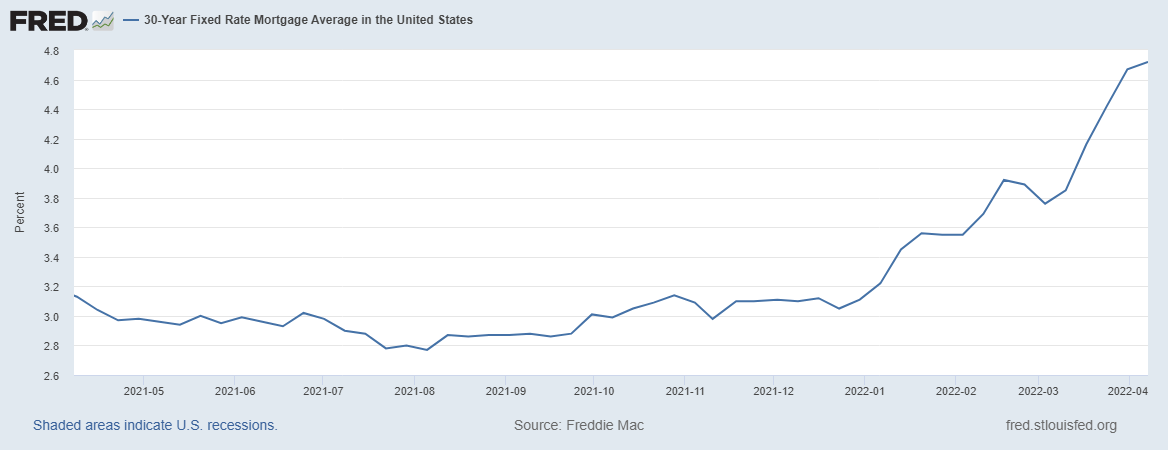

Look at the chart below. It plots the 30-year fixed-rate mortgage average in the U.S.

In August 2021, the 30-year mortgage rate was around 2.8%. Now it’s 4.7%. This is such a huge change in such a little time; the rate has spiked by 70%. Mind you, it could still go a lot higher.

(Source: “30-Year Fixed Rate Mortgage Average in the United States,” Federal Reserve Bank of St. Louis, last accessed April 14, 2022.)

Why do mortgage rates matter? They’re highly correlated with demand in the U.S. housing market. As mortgage rates go down, affordability increases. When mortgage rates surge, affordability declines: individuals need higher incomes to qualify for mortgages, and their mortgage payments are higher.

Adding to the misery, thanks to inflation and not much growth in terms of income in the U.S., Americans haven’t been saving as much as before.

Look at the following chart. It plots the U.S. personal saving rate.

In December 2021, Americans were saving 8.3% of their disposable incomes. In February 2022, this figure stood at 6.3%. The last time the U.S. personal saving rate was this low was back around 2013.

(Source: “Personal Saving Rate,” Federal Reserve Bank of St. Louis, last accessed April 14, 2022.)

U.S. Housing Market Outlook Is Gruesome at Best

Dear reader, seeing higher interest rates, businesses reopening their offices, stagnant incomes, and declining savings, I can’t help but be pessimistic about the U.S. housing market. It almost feels like a perfect storm is brewing. It could take the housing market lower, and housing-related investments could be in a lot of trouble. Beware if you own homebuilder stocks.

As home prices skyrocketed, homebuilder stocks surged. Look at the SPDR S&P Homebuilders ETF (NYSEARCA: XHB). This exchange-traded fund (ETF) tracks the performance of the major homebuilder stocks in the U.S. In early 2020, the ETF traded as low as $23.50. By early 2022, it was trading above $85.00. This represents an increase of more than 260% in about two years.

Will homebuilder stocks continue to perform like this if the housing market faces headwinds? It’s hard to see that happening.

Comments

Log in or sign up to join the conversation.