Image Source: Pixabay

The federal government charted a surprising budget surplus in August.

But don’t be fooled. The feds didn’t miraculously fix their deficit problem.

The Biden administration continued to spend money at an unsustainable pace last month. The surplus was merely a function of the reversal of student loan forgiveness.

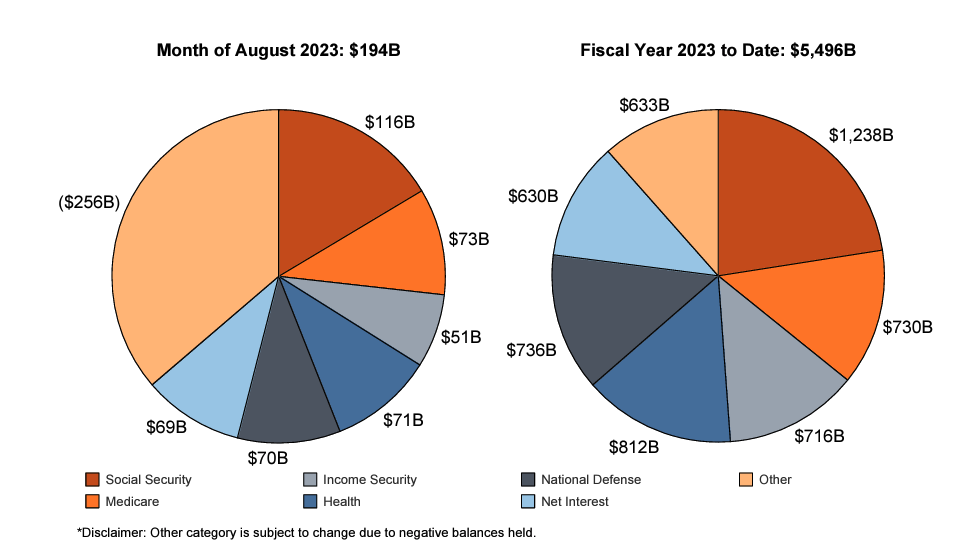

Officially, the US government recorded an $89.26 billion surplus deficit in August, according to the Monthly Treasury Statement. But if you factor out the $333.65 billion student loan forgiveness reversal, there was a $244.39 billion budget shortfall. That was a 56.8% increase over the August 2022 deficit.

The reversal of student loan forgiveness, funds added to the spending ledger in September 2022, was necessitated when the Supreme Court ruled the forgiveness scheme unconstitutional.

With one month left to go, the deficit for fiscal 2023 now stands at $1.52 trillion.

To put the deficit in perspective, prior to the pandemic, the US government had only run deficits over $1 trillion four times — all in the aftermath of the 2008 financial crisis. Trump almost hit the $1 trillion mark in 2019 and was on pace to run a trillion-dollar deficit prior to the pandemic. The economic catastrophe caused by the government’s response to COVID-19 gave policymakers an excuse to spend with no questions asked. Now the Biden administration has settled into the new status quo – running ’08 financial crisis-like deficits every single year.

Declining tax receipts continue to plague the Treasury. The government recorded $283.13 billion in receipts in August. That was a 6.78% decrease from August 2022.

The continues a generally downward trend in government receipts. Revenue is down 10% year-on-year.

The federal government enjoyed a revenue windfall in fiscal 2022. According to a Tax Foundation analysis of Congressional Budget Office data, federal tax collections were up 21%. Tax collections also came in at a multi-decade high of 19.6% as a share of GDP. But CBO analysts warned it won’t last. And government tax revenue will decline even faster as the economy spins into a recession.

The bigger problem is on the spending side of the ledger.

The Biden administration blew through another $527.53 billion in July (excluding the credit for the student loan adjustment). That was a 0.8% increase over August 2022 spending.

(Click on image to enlarge)

Now, you might be thinking that with the spending cuts in the Fiscal Responsibility Act, Congress fixed this problem. But we live in an upside-down world where spending cuts mean spending keeps going up.

In other words, the spending cuts will not put a dent in current spending levels. That means we can expect these massive deficits to continue month after month.

And the Biden administration already wants more money. Last month, the president asked Congress to appropriate $40 billion in additional spending, including $24 billion for Ukraine and other international needs, $4 billion related to border security, and $12 billion for disaster relief.

Keep in mind that the feds now have a credit card with no limit.

The fundamental issue wasn’t that the US government couldn’t borrow enough money. The fundamental problem was, and still is, that the US government spends too much money. Despite the pretend spending cuts, the debt ceiling deal didn’t address that problem. Even with the new plan in place, spending will go up. And it’s already historically high. That means big budget deficits will continue and the national debt will mount.

The national debt grew by $1.3 trillion in just three months, and it now stands just a hair under $33 trillion. It will likely eclipse that level this month.

Meanwhile, according to the National Debt Clock, the debt-to-GDP ratio stands at 122%. Despite the lack of concern in the mainstream, debt has consequences. More government debt means less economic growth. Studies have shown that a debt-to-GDP ratio of over 90% retards economic growth by about 30%. This throws cold water on the conventional “spend now, worry about the debt later” mantra, along with the frequent claim that “we can grow ourselves out of the debt” now popular on both sides of the aisle in DC.

To put the debt into perspective, every American citizen would have to write a check for $98,110 in order to pay off the national debt.

This is an unsustainable trajectory, especially in a high-interest rate environment.

With CPI still running hot, the Federal Reserve will likely raise rates at least one more time this year.

Meanwhile, the federal government has paid well over half a trillion dollars ($630 billion) on interest payments alone in fiscal 2023. In July, interest on the debt exceeded the amount spent on national defense. In August, defense spending was slightly higher, but Uncle Sam is well on the way to spending more on interest payments than any line item other than Social Security and Medicare. (You can read a more in-depth analysis of the national debt HERE.)

The rising interest on the national debt along with excessive government spending are two reasons the Federal Reserve can’t win the inflation fight.

In a recent interview, Peter Schiff pointed out that government spending and massive budget deficits are two reasons we have inflation to begin with.

All of that government spending is being financed by deficits and that’s really the source of the inflation. And it has been the source of the inflation for many, many years because the Fed has been monetizing all the government debt by creating money. That’s what’s been putting all the upward pressure on prices. So, it’s the government that’s responsible for the inflation. As long as the Biden administration keeps spending money that it doesn’t have, inflation is going to get worse.”

More By This Author:

CPI Spiked Again In August Throwing Cold Water On Disinflation NarrativeChinese Gold Demand Improved In August

Borrowing Our Way to Prosperity?

Comments

Log in or sign up to join the conversation.