As a dividend growth investor, my favorite picks are the ones that grow fast in all categories. Here are my top 3 fastest growing Canadian dividend stocks for 2020.

Those are super-powered companies showing strong stock price jump potential along with solid dividend increases. While they are sometimes a little riskier than “good old Canadian banks”, they add some spice to my investment recipe.

Keep in mind that my 3 top fast-growing stocks for 2020 show low dividend yield, but they also come with a high single-digit to double-digit dividend growth perspective.

The selection methodology of those companies is explained in this article: What a Dividend Growth Investor Buys in 2020?

Here are some great stock ideas for 2020:

CAE (CAE.TO) (CAE)

Market cap: 9B

Yield: 1.21%

Revenue growth (5yr, annualized): 9.72%

EPS growth rate ((5yr, annualized): 11.00%

Dividend growth rate (5yr, annualized): 12.13%

CAE is a world leader in simulation and training for the civil aviation and defense markets. Since both industries are growing and expected to grow significantly in the coming years, CAE will continue to surf on this strong tailwind. Management estimated that over the next 10 years, 300,000 pilots will become new first officers and 215,000 will have been upgraded to captain and will have to be trained to support airline fleet growth and to replace retiring pilots. The total active pilot population will grow to 530,000 in 2028 from 360,000 in 2018 creating a much larger market to support CAE’s recurring training services.

Source: Investors presentation

The growth potential is similar in the defense & security industry as many countries are increasing their spending in these categories. While the company enjoys a strong core based on these two sectors, it is currently expanding its services through healthcare training.

The beauty of CAE’s business model is that training is never over. There are always new methods, processes and technologies to learn and master. Therefore, the company is sitting on an almost infinite source of recurring revenues. The company can use its reputation and expertise to expand into other training markets. By using its strong cash flows, it can buy other businesses in the same field such as Bombardier’s Aviation Training business (closed in 2019). This is a great way to add recurring business to its model with little risk.

While CAE offers a low yield, you can expect a high single-digit to double-digit dividend growth each year. You will rarely see such a great business model with such strong growth potential for the next decade.

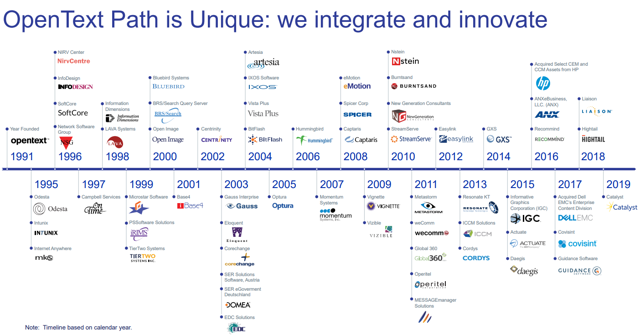

Open Text (OTEX.TO)(OTEX)

Market cap: 15.5B

Yield: 1.6%

Revenue growth (5yr, annualized): 16.92%

EPS growth rate ((5yr, annualized): 7.70%

Dividend growth rate (5yr, annualized): 20.15%

Big data, cloud, and security. Three keywords you are not done hearing about. As we evolve through an era of consolidation; businesses grow larger every second. Managing growth is one thing, but dealing with the enormous amount of data this growth is bringing inside each company is part of Hercules’ labors. Enterprise Information Management (EIM) systems have been developed to manage this issue, and OpenText happens to be one of the leaders in this emerging business.

Source: February 2019 investor presentation

OTEX shows a low yield but its growth policy is quite aggressive. OTEX will be surfing on strong tailwinds for several years. OTEX has built a business model generating consistent cash flow (recurring revenues through subscriptions). This will support dividend payment (and increases) for a while. As the company continues its quest for growth, expect a double-digit dividend growth policy for several years to come.

Alimentation Couche-Tard (ATD.B.TO)(ANCUF)

Market cap: 79B

Yield: 0.57%

Revenue growth (5yr, annualized): 14.12%

EPS growth rate ((5yr, annualized): 23.09%

Dividend growth rate (5yr, annualized): 28.62%

An investment in ATD is definitely not for an income-producing stock. However, if you are looking at the long-term horizon, your dividend payouts will grow in the double digits for a while and you will enjoy strong stock price growth. ATD’s potential is directly linked to its capacity to swallow and integrate more convenience stores. Management has often proven its ability to pay the right price and generate synergy for each deal. ATD shows a perfect combination of the dividend triangle: revenue, EPS and strong dividend growth.

Source: 2019 Investors presentation

The mediocre 0.57% dividend yield is so low that ATD shouldn’t even be considered as a dividend grower. However, the dividend paid has surged in the past 5 years (+174%) and the stock price jumped by over 125%. The only reason why the dividend yield is so low is because ATD is on a fast track for growth. ATD will continue increasing steadily its payout while providing stock value appreciation to shareholders.

Comments

Log in or sign up to join the conversation.