The Triple B Problem

Lately, I have fallen down when it comes to the number of MacroTourist posts. It’s not that I didn’t want to write, but I got Lennon’ed with life getting in the way of my plans. So to remedy this situation, I have decided to commit to posting today’s write up, but also a follow-up tomorrow. I figure that if I promise you two pieces, the shame of not following through will ensure compliance. Call it my own little life hack.

Today’s piece will be the bear argument, with tomorrow’s post arguing the bull case. I will not bother giving you all the reasons why the market might go up or down, but rather, focus on subtler reasons the market might be missing. Call it my version of the market’s in-attentional blindness (which by the way, I never seem to miss the guy in the gorilla suit so I almost don’t believe this is a real thing).

So on to it! The bear case.

Yesterday I was watching Bloomberg TV and one of my favorite reporters, fellow Canadian Luke Kawa, made the following joke:

“ask a journalist what’s the scariest thing for the markets, and the answer is triple B’s.”

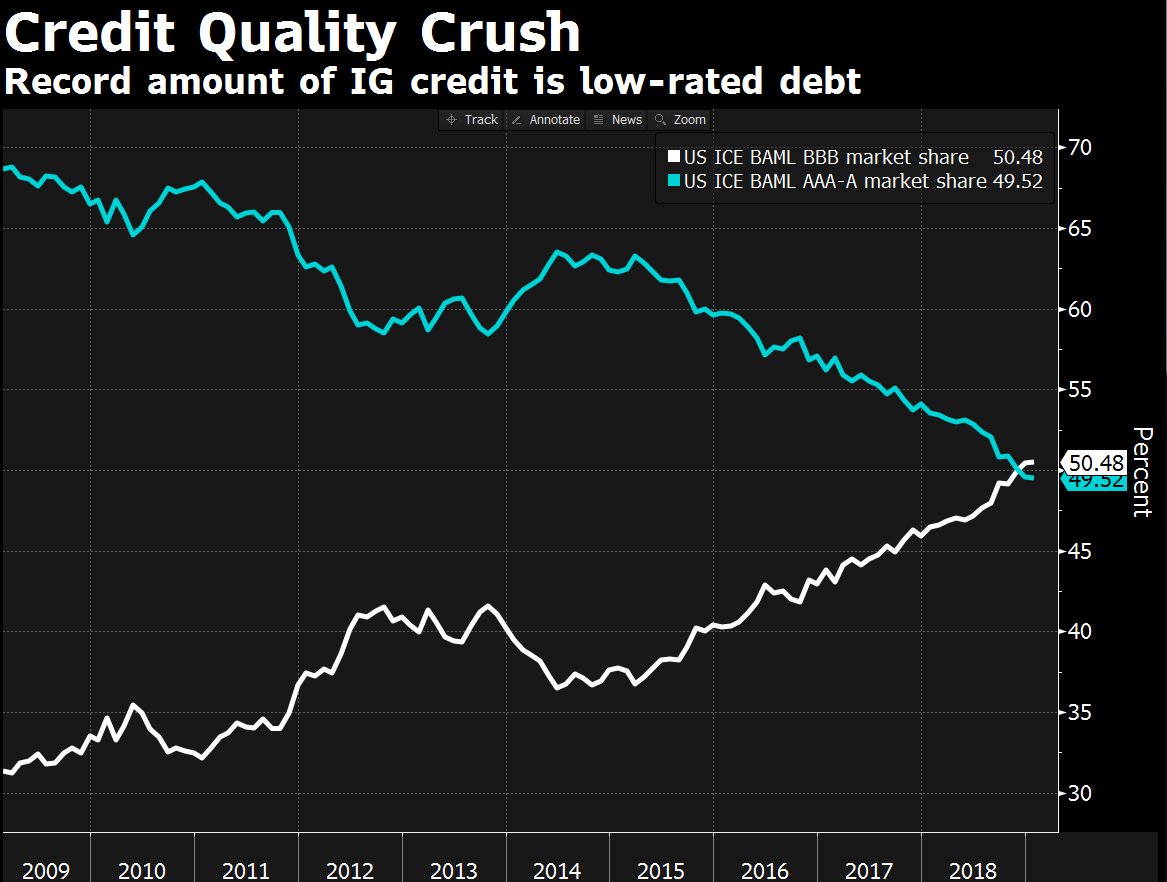

What did Luke mean by this comment? Well, I think it’s best explained by the following Bloomberg chart:

(Click on image to enlarge)

Investment grade debt is all corporate debt rated BBB or higher. If a debt security drops below this level, it is no longer investment grade and gets relegated to the high-yield or junk pile. The important thing to realize is that at that point, many institutions can no longer invest in the security. Therefore it is important for companies that rely on this funding to maintain at least a BBB rating.

What’s scary is that the number of issuers in the investment grade market ranked BBB has never been higher.

This means that the number of investment grade companies whose creditworthiness is one downtick away from junk is precariously perched ready to topple at the slightest weakness in the economy. Scary, huh? No wonder all the Bloomberg reporters have been highlighting it as a risk. It’s one of those inside baseball concerns that’s hard for the general public to get their minds wrapped around, but has professionals fretting.

Yet what’s the overwhelming conclusion about the consequence of this development? Why… that you should short investment grade bonds of course!

(Click on image to enlarge)

And maybe that’s the right trade. Maybe we are about to have another credit-led crisis as these companies slip to junk and can no longer fund themselves at the absurdly-low levels.

But I think too many people assume the next crisis will look like the last. And if there is one thing I know for sure, it’s that’s markets rarely make it so easy.

So I look at the number of BBB issuers, and I worry about the ominous development, but in my gut, I think the obvious trade (shorting LQD) will not be a money maker. Yet I didn’t know how to square this obviously negative trend with my forecast.

Lucky for me, another Canadian set me right in my thinking. I am indebted to Gluskin Sheff’s David Rosenberg’s insights regarding the implications of the large amount of BBB issuers. Recently David gave a speech at the University of Toronto (from the Varsity online publication):

Focusing on corporate debt, Rosenberg emphasized that “we have never had a more junkier corporate bond market than we do today.” He added that even the quality of bonds is poor, with 50 per cent of investment grade bonds rated BBB. This is the lowest rating for an investment grade bond, with lower graded bonds classified as ‘junk’ and considered high-risk or speculative.

Rosenberg explained that the response to the current high leverage will be corporate deleveraging. This would in turn lead to recession because of the sacrifices in capital spending.

Imagine you are a CEO at one of these companies that is teetering on losing its investment grade rating. What would you do? Continue spending balls-to-the-wall on equity buybacks and capex? No, not a bloody chance. You would hunker down and cut both of those expenditures. You will do whatever it takes to maintain your investment grade rating.

Therefore the trade is not to short investment grade bonds, but rather to short equities and play for a weakening economy due to weak capex spending.

Let that sink in for a second. There is little doubt the BBB story will get more airplay in the coming months and quarters. There will be lots of worrisome pieces which will encourage lots of bearish recommendations on investment grade bonds.

But ignore them. The trade will not be to short investment grade bonds. The problem will not be a collapse of investment grade bond prices, but rather the effects this credit deterioration has on equities and the economy as a whole…

Disclosure: None.

This could be good advice.