Photo by Nicholas Cappello on Unsplash

Yalla Group (NYSE: YALA), an online social networking and gaming platform based in the Middle East and North Africa (MENA) region, surprised investors with a strong set of results on Tuesday. The quarter was characterized by further user growth, an expansion of margins, 4.1% revenue growth, and a significant increase in non-GAAP net income to US$33.8 million.

Intro:

Yalla's primary offering is a voice-centric social platform that combines voice chat rooms with various interactive features such as games, music, and other forms of entertainment. The firm has gained popularity as a platform for connecting people in the MENA region, where voice communication and community engagement hold cultural significance.

Yalla operates on a diverse business model that encompasses multiple revenue streams, such as in-app purchases, subscription services, virtual gifting, and advertising. Since its initial public offering (IPO) in September 2020, priced at US$7.50 per American depositary share (ADS), the company has consistently generated profits. This profitability has facilitated the accumulation of substantial cash reserves, which currently stand at an impressive US$510.5 million.

Investors will be positively surprised by Yalla's Q2 results. Net income expanded significantly quarter over quarter – US$28.3 million from US$19.9 million – while there was further good news in the form of falling costs, increasing average user numbers, and higher revenues.

A strong quarter

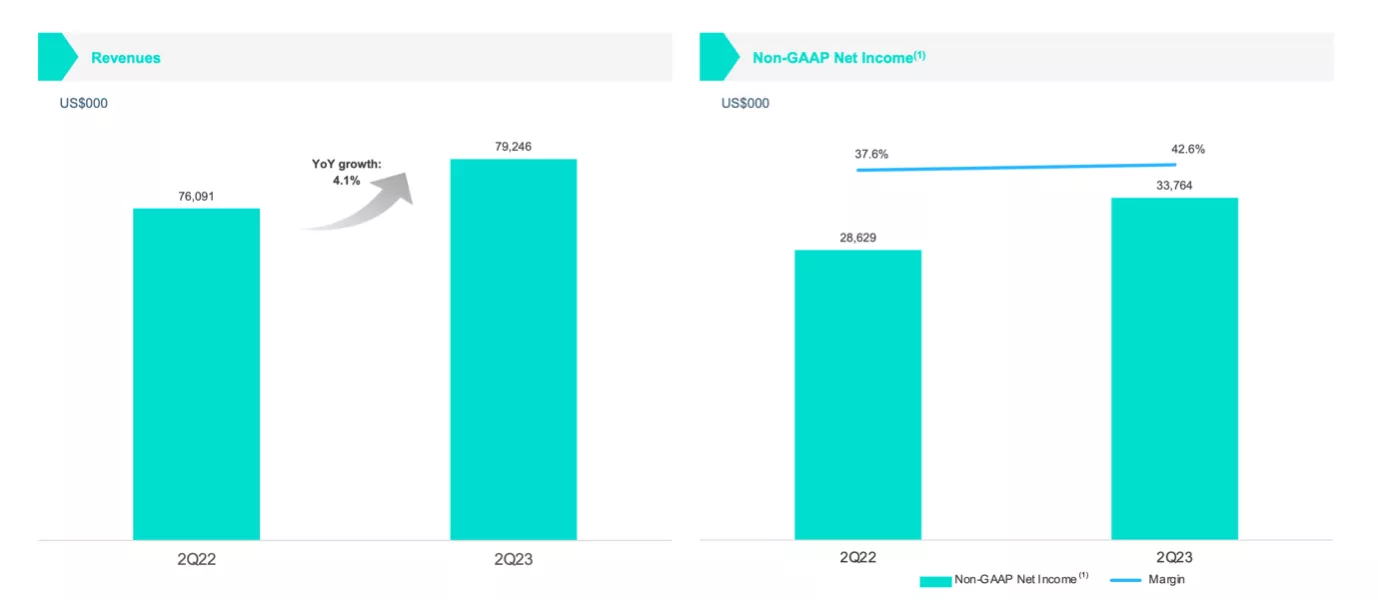

Yalla achieved notable successes in both financial and operational aspects during the second quarter of 2023. The expansion in net income and profit margins were core to these impressive results. Net income increased 38.9% YoY and 42.0% QoQ, representing some of the strongest figures released by Yalla to date. This quarter's net margin, standing at 35.7%, reflects this positive trajectory in terms of profitability. Similarly, we can observe non-GAAP net income extending to US$33.8 million, from US$28.6 million a year ago, and a sizeable non-GAAP net margin of 42.6%.

Net income was supported by a more modest 4.1% YoY increase in revenues to US$79.2 million. A significant portion, as we've seen previously, came from chatting services – US$55.2. This reflects a 9.5% increase in QoQ. Additionally, the games services accounted for US$24.0 million in revenue during the same quarter, a modest increase on the US$23.1 million recorded in the three months until the end of March.

(Click on image to enlarge)

Source: Yalla Q22023, Results Presentation

User engagement also improved during the quarter, with Yalla now boasting 34.2 million active users, up 14.3% from 29.9 million a year previous and from 33 million in the previous quarter. Moreover, the number of paying users on the platform experienced a substantial surge of 26.6%, reaching 13.4 million in the second quarter of 2023, up from 10.6 million in the same period of the previous year. However, there was a small contraction on a quarterly basis – Yalla had recorded some 13.5 million paying users in the first quarter of 2023.

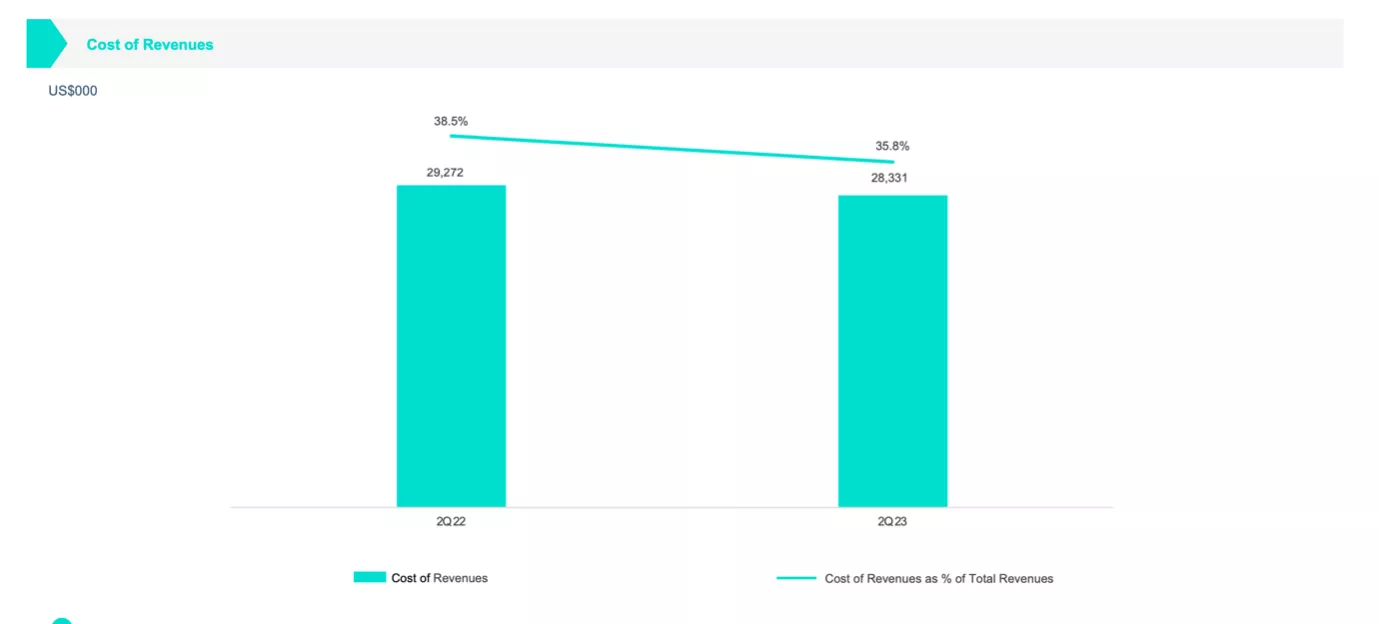

Total costs and expenses remained relatively stable at US$55.3 million in the second quarter of 2023, compared with US$55.2 million in the second quarter of 2022. Total costs and expenses amounted to US$56.8 million in the first quarter of 2023, and US$60.1 million in the fourth quarter of 2022. Meanwhile, in Q2 cost of revenues fell in real and percentage terms, to 35.8% from 38.5% a year ago. These falling costs partially enabled rising net income.

(Click on image to enlarge)

Source: Q2023, Results Presentation

Results Commentary

Apart from generating sales from its user base, Yalla has strategically shifted its focus toward diversifying income sources. This strategy involves expanding its established services to new geographical regions and delving into the creation of a new segment centered around mid-to-hard-core gaming. Naturally, the establishment and growth of this new gaming segment require dedicated investments. As such, investors may be surprised to see costs and R&D investments falling.

In the second quarter of 2023, Yalla reported a 14.8% YoY reduction in technology and product development expenses, with the figure amounting to US$6.6 million. By comparison, the Dubai-based firm spent US$7.7 million during the same period the previous year, and US$7.4 million in Q1 of 2023. The company says the primary factor contributing to this reduction was the appreciation of the US dollar.

However, as noted in previous quarters, it may be a while before investors see the impact of R&D expenditure may not be seen for some quarters. While we did see a 4.0% increase in gaming revenue QoQ, it is unrealistic to assume that new gaming applications will immediately generate strong revenues. Mr. Yang Tao, Founder, Chairman, and CEO of Yalla highlighted the impact of the hard-core mobile game Merge Kingdoms on sales in Q2, but investors may be expecting more over the next 12 months.

Low risk, low P/E

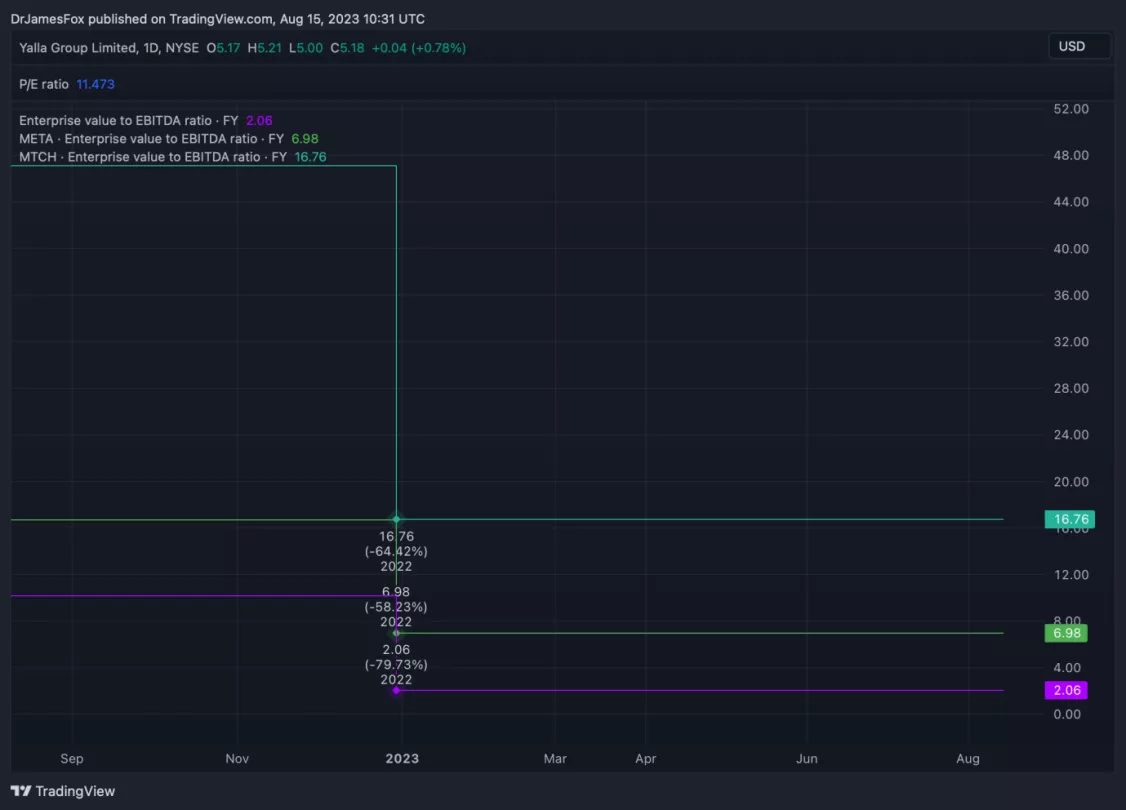

Yalla is one of the most intriguing technology stocks. It trades at a fraction of the valuation afforded to its globally-focused peers such as Meta. Yalla currently trades at 11.2x earnings on a trialing 12-month basis versus a communications sector median of 16.9x. The below chart shows the price-to-earnings ratio of Yalla, Meta, and dating app owner Match Group.

(Click on image to enlarge)

Created at TradingView

Yalla's discount to the sector is even more pronounced when we look at EV-to-EBITDA. The ratio provides insight into a company's valuation relative to its operational performance, independent of its capital structure. As we can see, Yalla trades with an EV-to-EBITDA ratio of just 2.06. That makes it considerably cheaper than its peers.

(Click on image to enlarge)

Created at TradingView

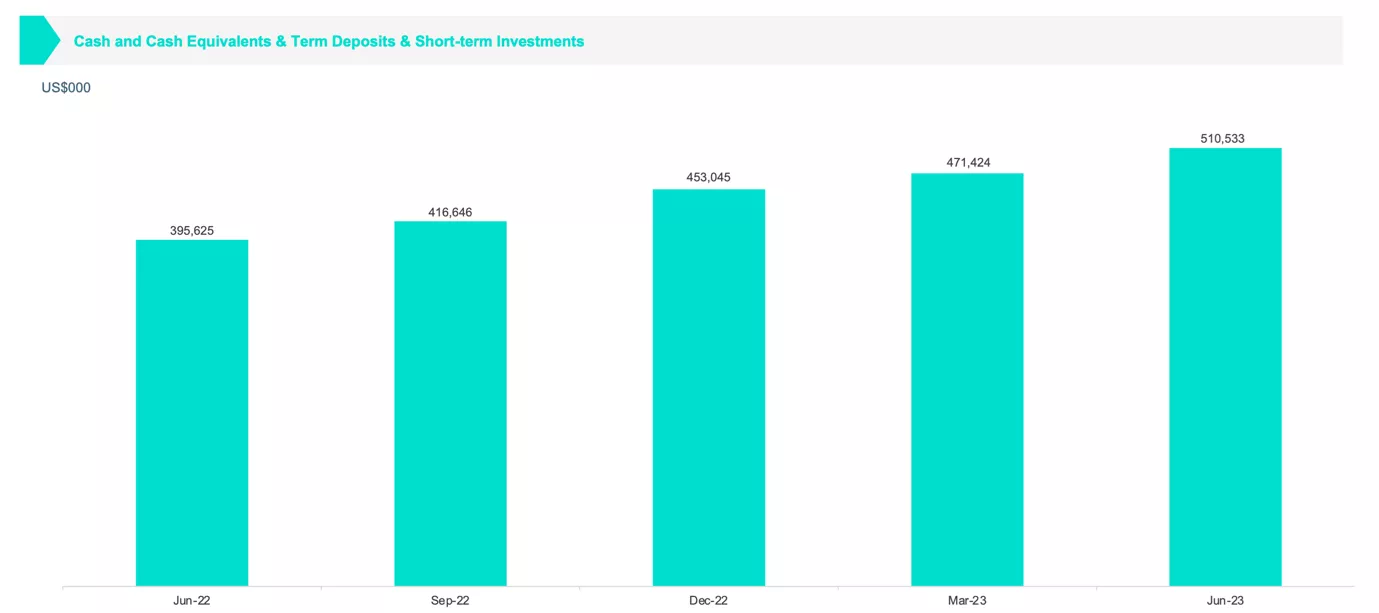

One reason for this discount is Yalla's sizeable cash and cash equivalents. The company had US$510.5 million in hand at the end of the second quarter, up from US$471.4 million at the end of Q1. This means the enterprise value of the stock is just around US$300 million – That's not a lot for a company that will likely generate between US$70-80 million this year.

(Click on image to enlarge)

Source: 2Q2023, Results Presentation

Consequently, Yalla emerges as an investment option that carries a comparatively low level of risk. This assessment is grounded in several key factors that collectively underscore the company's financial stability and potential for sustained growth. Firstly, Yalla's lack of debt burden positions it favorably within the investment landscape, minimizing the risks associated with interest payments and potential financial strain. Moreover, the company maintains a robust cash position, which not only provides a safety net during uncertain times but also enables strategic investments and business expansion.

The track record of profitability further solidifies Yalla's attractiveness to investors. Demonstrated profitability over a sustained period showcases the company's ability to generate earnings and navigate market challenges effectively. This track record not only instills confidence in its operational prowess but also indicates a level of financial discipline that contributes to its low-risk profile.

In addition to these factors, the positive trajectory of revenue developments further bolsters Yalla's investment appeal. A history of revenue growth, coupled with a strategic focus on diversifying revenue streams, suggests a forward-looking approach that aligns with changing market dynamics. This adaptability and proactive stance contribute to Yalla's resilience in the face of uncertainties and its potential for future expansion.

Collectively, Yalla's absence of debt, substantial cash reserves, proven profitability, and commitment to revenue diversification all contribute to positioning the company as a favorable choice for investors seeking a lower-risk investment option that aligns with sound financial principles and promising growth prospects.

More By This Author:

Yalla Group: A Strong Business In Low-Risk Transition

What Can AI Generated Content Bring To Education?

Yalla Group: Seeking A Balance Between Growth And Stability

Comments

Log in or sign up to join the conversation.