Image Source: Pixabay

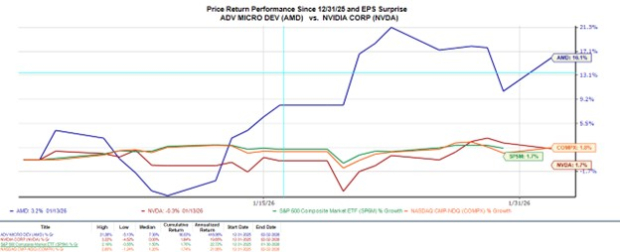

AMD's (AMD - Free Report) stock has had an explosive start to 2026, spiking over +15%, and is now up more than +100% in the last year as it gains share in the AI chip market.

With companies seeking alternatives to Nvidia’s (NVDA - Free Report) ecosystem, AMD’s rally has been driven by surging demand for its AI accelerators, bullish analyst upgrades, and near-sold-out server CPU capacity — creating a perfect storm of optimism around its revenue outlook.

This makes it a worthy topic of whether it's still time to buy, hold, or take profits in AMD stock as its Q4 results approach after-market hours on Tuesday, February 3.

Image Source: Zacks Investment Research

AMD’s Q4 Expectations

Based on Zacks estimates, AMD’s Q4 sales are thought to have increased 26% to $9.67 billion compared to $7.66 billion a year ago. On the bottom line, Q4 EPS is expected at $1.32, a 21% increase from $1.09 per share in the comparative quarter.

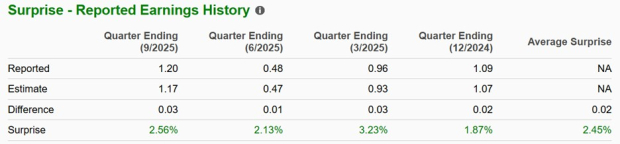

It's noteworthy that AMD has been able to exceed top and bottom line expectations in each of its last four quarterly reports, posting an average sales and EPS surprise of 4.02% and 2.45%, respectively.

Image Source: Zacks Investment Research

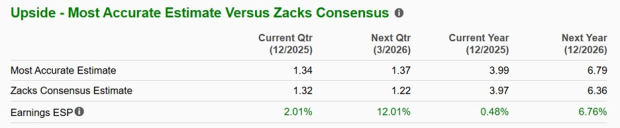

Furthermore, the Zacks ESP (Expected Surprise Prediction) suggests AMD could once again surpass earnings expectations, with the Most Accurate and recent estimate among Wall Street analysts having Q4 EPS pegged at $1.34 and 2% above the underlying Zacks Consensus (Current Qtr below).

Image Source: Zacks Investment Research

High Demand for AMD’s AI Accelerators

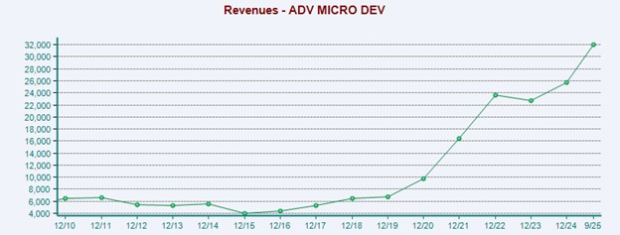

Rounding out fiscal 2025, AMD’s total sales are expected at $34.03 billion, a 32% spike from $25.79 billion in 2024. Plus, FY26 sales are projected to soar another 29% to $43.9 billion. It’s worth noting that analysts are already forecasting AMD’s AI revenue for 2026 to be between $14-$15 billion, driven by its MI355 and MI455 accelerator shipments.

The MI355 and MI455 accelerators are next-generation AI and HPC (high-performance computing) GPUs built on AMD’s compute DNA architecture (CDNA). These AI accelerators are designed to compete directly with Nvidia’s highest-end data-center chips by offering massive memory bandwidth, advanced low-precision formats, and extreme compute density.

Image Source: Zacks Investment Research

Positive EPS Revisions

AMD’s annual earnings are now expected to be up 20% for FY25 at $3.97 per share, versus EPS of $3.31 in 2024. Even better, FY26 EPS is forecasted to soar another 60% to $6.36.

More reassuring is that FY25 EPS revisions are slightly higher in the last 30 days, with FY26 EPS estimates rising more than 1% from projections of $6.27 a month ago.

Image Source: Zacks Investment Research

Conclusion & Final Thoughts

AMD’s hot start in 2026 isn’t hype; it’s the result of real demand for its AI hardware, strong analyst conviction, and a product roadmap that aligns perfectly with the AI infrastructure boom. At around $250 a share, AMD stock is currently trading at 37X forward earnings, which is a noticeable premium to the benchmark S&P 500 but offers a slight discount to Nvidia’s 40X.

Considering EPS revisions have been positive, and AMD has strengthened its position in the semiconductor market thanks to its AI accelerators, the rally in its stock could still have legs. For now, AMD stock sports a Zacks Rank #2 (Buy).

More By This Author:

Cenovus Vs. Enbridge: Is It Time To Step Away From Both Stocks?2026 Volatility Playbook: NVIDIA, Barrick, Newmont & More In AI, Gold & Power

Buy Meta Stock After Strong Q4 Results & CapEx Hike?

Comments

Log in or sign up to join the conversation.