U. S. stocks extended their decline from the first week of 2022. Bank earnings disappointed investors. In economic data, retail sales and consumer sentiment declined. Inflation remained high. Investors questioned the strength of the economy to get through the omicron risk.

U. S. fell for a second consecutive week. Bank stocks, which had been rising in recent weeks against the backdrop of rising interest rates, dropped as their earnings reports underwhelmed investors. JPMorgan guided profits to fall short of targets due to higher expenses, the threat of the omicron virus variant, and lower trading revenues.

In economic data, retail sales fell 1.9% in December, more than the 0.1% decline expected by economists surveyed by Dow Jones. Shortage of goods and a steep increase in omicron-related infections impacted retail sales.

The University of Michigan’s preliminary January consumer sentiment reading fell 1.8 points in January to 68.8. The decline in consumer sentiment reflected the pain lower-income Americans face from inflation.

Inflation stayed high and generally in line with economists’ expectations. The consumer price index showed a year-over-year increase of 7%, the highest four decades, while the producer price index report reflected a rise of 9.7% over the same period.

The above data raised doubts on the economy having enough strength to overcome the pressure from the omicron virus while the Federal Reserve tapers monetary stimulus to counter inflation.

By the end of the week, investors rotated out of cyclical value stocks and sought bargains in out-of-favor large-cap growth stocks.

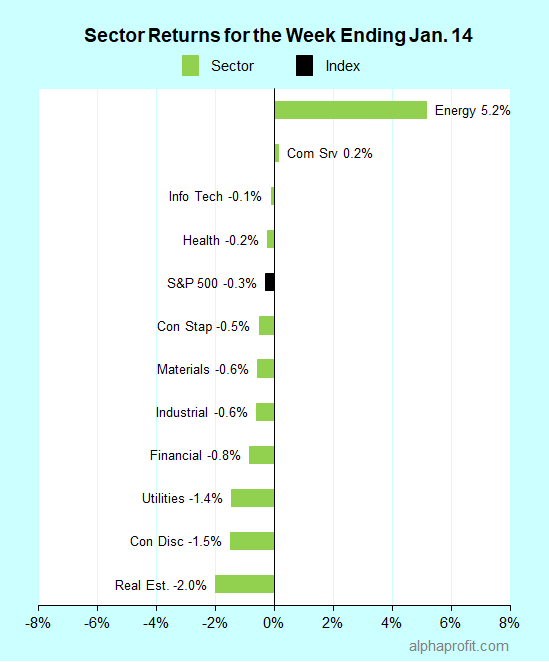

For the week ending January 14, the S&P 500 (SPY) fell 0.3%. Two of the 11 sectors gained..

Leaders and laggards for the week ending January 14, 2022.

Market breadth was neutral, with the number of advancing stocks in the S&P 500 almost equaling the number of decliners.

Energy (XLE) and communication services (XLC) ended above the flat line.

Real estate (XLRE), consumer discretionary (XLY), and utilities (XLU) lagged the S&P 500, losing 1.4% or more.

The S&P 500’s top 10 winners included consumer discretionary, energy, health care, and information technology companies.

1. Consumer Discretionary

Gaining 13%, Las Vegas Sands (LVS) was the top performer in the S&P 500 for the week. Sand’s competitor Wynn Resorts (WYNN) rose 8%. Casino stocks rose after the Macau government clarified the number of casinos allowed to operate there would remain limited to six.

Robust quarterly results & forecasts and comments on firm pricing & rising margins from non-S&P 500 index homebuilder KB Home lifted share prices across this group. Index member PulteGroup (PHM) ended 9% higher for the week.

2. Energy

APA Corp. (APA), Halliburton (HAL), Pioneer Natural Resources (PXD), and Phillips 66 (PSX) rose 8-12% each, following oils 6% gain for the week. Oil rose on a weaker U. S. dollar and escalating supply concerns, spurred by the tension between the U. S. and Russia vis-à-vis Ukraine.

3. Information Technology

Semiconductor capital equipment makers Applied Materials (AMAT) and Lam Research (AMATLRCX) rose 11% and 9%, respectively, after semiconductor chipmaker Taiwan Semiconductor said it intends to spend over $40 billion expanding and upgrading capacity in 2022 due to unprecedented chip shortage.

4. Health care

Illumina (ILMN) shares rose 9% after the gene-sequencing technology company upped its 2022 revenue forecast and announced new partnerships with four healthcare companies.

Comments

Log in or sign up to join the conversation.