Why Hasn't FedEx (FDX) Climbed Alongside United Parcel Service (UPS)?

Image: Bigstock

FedEx FDX and United Parcel Service UPS are two very well-known names in the transportation (Air Freight and Cargo) industry.

Over the last year, these two shipping giants have posted diverging price action. UPS has been trending upwards, consistently making new highs. By contrast, FDX has done quite the opposite and has struggled to regain and hold a consistent uptrend.

Let’s take a look into why United Parcel Service has been outperforming FedEx over the last year, comparing key metrics and earnings data.

UPS

UPS’s current market cap sits at around $183 billion and its stock price hit all-time highs of $235 in early February. Since then, it has declined roughly 12% to around $210.

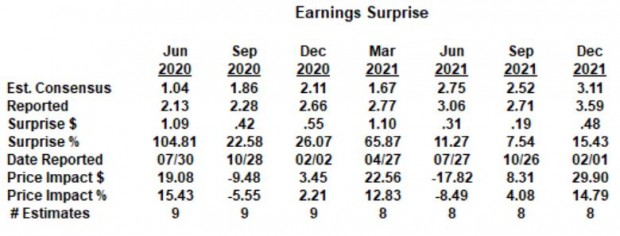

The company’s earnings reports have been nothing short of impressive. UPS has beat estimates seven times in a row, with an average beat of a staggering 36%. In the most recent earnings report in February, it beat estimates by nearly 16% and raised its earnings per share to $3.59 from $3.11.

Image Source: Zacks Investment Research

The consensus estimate trend for fiscal 2022 and 2023 for UPS has climbed recently, with FY22 up 7.7%, or $0.91 to $12.81. Fiscal 2023 has seen an increase of 4.2% over the last 60 days, up to $13.23 from $12.70.

UPS also enjoys raising its dividends, with a five-year annualized dividend growth rate of 5.1%. It’s raised its dividend in each of the last five years, and its yield comes in at 2.9% at the moment.

The company has beat revenue estimates in each of its last seven quarters for an average surprise of 7.4%, increasing its top line by nearly 47% from 2017 to 2021. Additionally, UPS’s revenue of nearly $100 billion over the last twelve months is enough to rank it at the very top of the industry.

UPS currently has a forward 12-month P/E ratio of 16.6X, roughly 53% higher than its low of 10.8X in March of 2020 and 28% lower than its high of 23.1X in October of 2020. The metric has been range-bound and fluctuated between a value of 15X and 20X since July of last year.

United Parcel Services currently has a Value Style Score of A, a Growth Style Score of C, and a Momentum Style Score of C. Its overall VGM Score is a B and is a Zacks Rank #3 (Hold). In FY22, EPS is expected to grow to $12.81, and in FY23, EPS is expected to grow to $13.23.

United Parcel Service, Inc. Price, Consensus and EPS Surprise

United Parcel Service, Inc. price-consensus-eps-surprise-chart | United Parcel Service, Inc. Quote

FedEx

FDX’s current market cap is much lower, sitting at around $57 billion. Its current share price is approximately $215, representing a rather steep decline of 32% off its all-time high of $315 in May of 2021. Year-to-date, FedEx has experienced shaky price action and has dropped by nearly 17%.

Diving into the company’s recent earnings reports, we see that FDX has not beat earnings estimates as often as UPS. Within the last seven reports, FedEx has missed estimates twice. It missed in June of 2021 when it hit its all-time highs of $320 a share, and in the following report in September. The firm’s most recent earnings report had a respectable 14.18% surprise, raising its EPS to $4.83. Year over year, EPS grew by 47%.

FedEx Corporation Price, Consensus and EPS Surprise

FedEx Corporation price-consensus-eps-surprise-chart | FedEx Corporation Quote

The consensus estimate trend for fiscal 2021 and 2022 has seen very slight increases over the last 60 days. For fiscal 2021, the trend is up 0.53%, or $0.11, to $20.82. Fiscal 2022’s consensus trend has increased by 0.26% to $23.22.

FedEx’s annual dividend yield is currently 1.4%. In three of the last five years, FedEx has increased its dividend, resulting in a five-year annualized dividend growth rate of 11.2%.

The company has beat revenue estimates in seven straight earnings reports, with its most recent sales surprise coming in at 4.2%. FedEx’s top line has seen an increase of nearly 40% from fiscal 2017 to the end of fiscal 2021 and currently sits just behind UPS at a rank of two in the industry, with sales of nearly $90 billion over the last twelve months.

FDX’s current forward 12-month P/E ratio is 9.8X, down 43% off its high of 22.5X and up nearly 30% from its low of 7.6X over the last five years. The metric has been decreasing since early June of 2021.

Image Source: Zacks Investment Research

FedEx currently has “A” grades for Value and Momentum and a “B” for Growth in the Zacks Style Scores system. Its overall VGM Score is a B and is a Zacks Rank #3 (Hold). For FY22, it’s expecting an EPS of $20.82 and in FY23, it is expecting an EPS of $23.22.

Summarizing FedEx’s Recent Struggles

UPS has shown very little signs of slowing down and has been able to continue its uptrend within the market, however, FedEx, a very similar company by nature, has seen unfavorable price action. FedEx has been an interesting name to follow in the market over the last year and has some scratching their heads.

UPS’s consensus estimate trend has been rising at a much faster rate for fiscal 2022 and fiscal 2023. United Parcel Service has also increased its dividend more often than FDX, and UPS has strung together seven straight earnings beats.

Ever since the EPS miss in June, FedEx has not been able to get its feet back underneath of it, down nearly 33% from its all-time high.

Disclaimer: Neither Zacks Investment Research, Inc. nor its Information Providers can guarantee the accuracy, completeness, timeliness, or correct sequencing of any of the Information on the Web ...

more