Why After A Massive Run, CoLucid Shares Still Look Attractive

It's been a difficult year to be a biotech investor. The SPDR Biotech ETF (XBI) is down 17% YTD. Things started out harshly in January 2016 with a precipitous drop of 35%, and despite a nice recovery during the middle of the year, the past month has been rather unkind to investors. Yet, not all companies have struggled in 2016. Shares of CoLucid Pharmceuticals, Inc. (NASDAQ: CLCD) are up a whopping 290% YTD, thanks largely to the release of positive topline data from the company's first Phase 3 trial with lasmiditan in September 2016.CLD

Lasmiditan is a first-in-class 5-HT1F receptor agonist currently in Phase 3 development for the treatment of acute migraine attack. The company reported positive topline data from the first Phase 3 trial in early September 2016. The data sent shares of CoLucid flying over 300% higher over the next week. The release of further data from that study and a strong institutional financing put the shares at nearly $40 earlier in October, up from below $5 back in February 2016.

The market value of CoLucid shares today is just below $600 million, and although this is a 5-fold increase from January 1st, I think there still may be significant upside left in the name. Below I attempt to address some of the key questions investors might have about the story.

- What is a migraine headache, anyway?

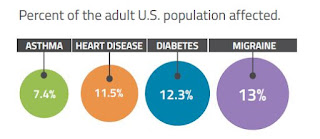

A migraine is a serious, debilitating neurological condition. The disease affects roughly 13% of the global population and is more common than asthma, heart disease, and diabetes in the U.S. (source: U.S. CDC, 2014). That equates to approximately 36 million individuals in the U.S., approximately 2% of which report having ≥ 15 or more episodes per month according to the 2011 Project Atlas study by the World Health Organization. Women affected outnumber men 4-to-1. In fact, migraines affect 30% of women over a lifetime and impacts life in almost 1 out of 4 households (source: American Headache Society).

- What causes a migraine?

Migraines are often idiopathic in nature but can be triggered by food, environmental factors, stress, weather, and exposure to light. There is even genetic predisposition to a migraine, with approximately 80% of migraine sufferers having a family history of a migraine affecting a first-degree relative (source: American Headache Society). Comorbidity with cardiovascular disease is also quite common, and patients with a migraine have a 54% increase in the risk of developing coronary artery disease (CAD) compared to the general population (9.9% vs. 6.4%) per IMS Health claims.

- Don't most migraine patients just take OTC medications, like ibuprofen or naproxen?

According to data from IMS Health, sourced from adjudicated claims for health plan enrollees across the U.S., roughly 4 million adults in the U.S. are diagnosed with migraine headaches, which is only slightly above 10% of the total afflicted population based on the WHO Project Atlas study. That means nearly 32 million Americans either do not know they have migraines - presumably they just assume they get really bad tension headaches - or know but chose to manage their disease without pharmaceutical intervention.

Of diagnosed patients, approximately 50% attempt to manage the disease by the use of OTC medications, including non-steroidal anti-inflammatory drugs (ibuprofen, naproxen, etc…), aspirin, and acetaminophen. However, for many moderate-to-severe migraine sufferers, NSAIDs, and other OTC medications do not provide sufficient relief. Thus, these 2 million individuals each year will visit a primary care physician (65%), neurologist (20%), or headache specialist (15%) seeking prescription medications to treat their disease.

However, even prescription drugs do not work for the most severely impacted. IMS Health reports that over 5 million ER visits per year are due to migraines. The direct medical costs associated with migraines in the U.S. approximate $17 billion. Over 90% of individuals with migraines report missing work due to an attack, leading to 112 million days of lost work annually (IMS Health, 2016). Another 50% say that migraines restrict activities or interfere with daily activities on a regular basis (Migraine.com). Indirect medical costs from lost work or lost productivity amount to another $15 billion in the U.S.

So while OTC medications to treat a migraine are quite common, the are effective in less than half of the patients. And, as noted above, the increase in incidence of comorbid cardiovascular disease is concerning to migraine patients taking frequent NSAID. NSAIDs do increase the risk of cardiovascular events in at-risk patients.

- Most migraine patients are prescribed triptans, right? Why do we need another class of drugs when triptans work and are now super cheap (generic)?

Within the prescription market, triptans control the majority of the share, accounting for 91% of migraine prescriptions and 72% of migraine units according to a June 2010 audit by IMS Health. Sumatriptan, sold by GlaxoSmithKline (NYSE: GSK) as Imitrex® is the triptan market leader, with approximately 75% market share. Imitrex generated peak sales in the U.S. of approximately $1.1 billion before the patent expiration in 2008. Pharmacies dispensed approximately 13 million prescriptions for Triptan or Triptan-products during 2014. One-third of these patients are taking multiple drugs to control their disease. Migraine prescription drug sales in seven countries (U.S. and Europe) were estimated to be $3.3 billion in 2015 and are expected to grow to $4.4 billion in 2020.

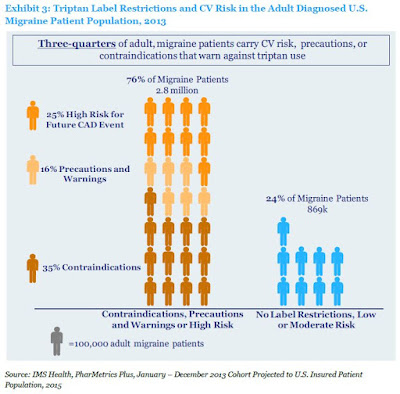

So these are a very popular choice for prescription-seeking migraine sufferers; however, despite the popularity of triptans, approximately 76% of triptan users have conditions or risk factors as defined by the Framingham Heart Study results (2003) that contraindicate or warn against triptan use (IMS Health, 2016). These triptan-intolerable patients included those at high risk for coronary artery disease, a history of stroke, peripheral vascular disease and chronically uncontrolled high blood pressure. These patients are also often on concomitant medications that could have potentially dangerous side-effects when used in combinations with triptans.

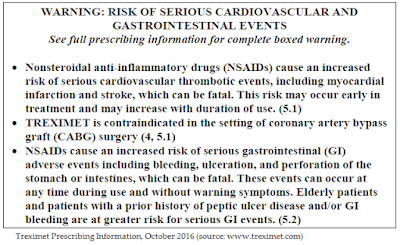

For example, the label for sumatriptan includes “Warnings and Precautions” that note potential risks for use of the drug in patients with a history of myocardial ischemia, myocardial infarction, and angina. Sumatriptan is contraindicated for use in these patients. The FDA also cautions on use of the drug in patients with a history of arrhythmias, chest, throat, neck, and/or jaw pain or pressure, or at risk for cerebrovascular events. Even worse, mixing a triptan with a NSAID like naproxen potentially creates even more risk. Below is a screenshot of the "Black Box" for Treximet®, a combination sumatriptan/naproxen tablet sold by Pernix Therapeutics (NASDAQ: PTX).

Based on this information, I believe there is a significant void in the market for an effective migraine treatment option that is not contraindicated for the majority of sufferers.

- What about opioids? Can't migraine sufferers just take an opioid instead?

This is a horrible idea if for no other reason than the opioid epidemic in this country is out of hand. We must find new, alternative medicines to control pain that does not involve dangerous opioids! That being said, according to IMS Health, 17% of adults suffering from migraine use butalbital and opioids to manage their disease. The drugs are effective in about two-thirds of the patients, but present an entirely new set of challenges and risk factors beyond triptans, including addiction and the potential for abuse/misuse.

- Ok, you've convinced me of the need. Now tell me about lasmiditan... it sounds like another triptan?

Despite similar phonetics, lasmiditan and sumatriptan are quite different. Lasmiditan is not a triptan!

Sumatriptan is an agonist of the 5-HT1B/1D serotonin receptor. Its primary method of action is vasoconstriction of the dilated cranial and basilar arteries. This reduces the inflammation associated with a migraine. Unfortunately, it also has broad-scale vasoconstriction effects, which is why the drug is dangerous to individuals with already constricted or blocked arteries, like those with CAD, hypertension, hyperlipidemia, or advanced diabetes. The drug does not penetrate the blood-brain barrier to any meaningful extent.

Lasmiditan is a new class of drugs called "ditans" that works through a non-vasoconstrictive mechanism. The drug targets the 5-HT1F serotonin receptor expressed in the trigeminal neural pathway. It penetrates the blood-brain barrier and selectively targets 5-HT1F without the broad vasoconstrictor activity that may negatively impact patients with cardiovascular disease. The drug more effectively treats the root cause of migraines rather than addressing the symptoms or downstream effects (like NSAIDs or triptans).

- Tell me about the Phase 3 data?

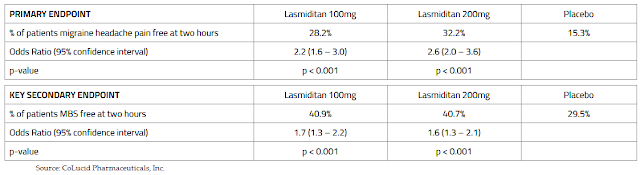

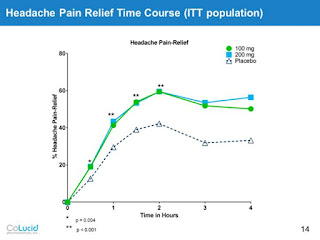

On September 6, 2016, CoLucid reported topline results from the Phase 3 SAMURAI clinical trial examining lasmiditan (100 mg and 200 mg) compared to placebo for the treatment of an acute migraine. The results were positive, with the trial meeting the primary and key secondary endpoints.

At the European Headache and Migraine Trust International Congress (EHMTIC 2016) in Glasgow, Scotland on September 17, 2016, CoLucid provided an additional analysis of the primary endpoint, this time reporting intent to treat (ITT) data on the percent of patients with migraine headache pain relief, defined as moderate or severe headache pain at baseline reduced to mild or no headache pain at two hours post-dose. The results show strong statistical significant in favor of lasmiditan.

At EHMTIC, the company also presented data showing that patients dosed with lasmiditan were less likely to use a second dose of study drug. Lasmiditan was effective on migraine headache pain freedom at the two-hour time point assessment following the second dose of a rescue medication as compared to placebo. The number of patients who took the second dose of study drug for recurrence was small (53 out of 1,671) with no significant difference among treatment groups.

Just earlier this month, CoLucid provided data on the rapid onset of action for lasmiditan - an endpoint that should be particularly meaningful to migraine sufferers. The data show a statistically significant effect in favor of lasmiditan at only 30 minutes for both the 100 mg and 200 mg dose. The results for the key MBS secondary endpoint were also statistically significant in favor of lasmiditan at only 30 minutes post-dose.

- What is the "MBS" secondary endpoint?

As part of the analysis, CoLucid included relief from a "most bothered symptom" (MBS) as a key secondary endpoint. Since migraine aura manifests such a diverse range of symptoms, including visual, sensory, motor, or verbal disturbance, and nausea, subjects indicated the presence or absence of nausea, phonophobia, or photophobia at baseline and were asked to pick the one symptom that was "most bothersome" and report if lasmiditan provided relief at two hours post-dose.

The MBS endpoint was patient-centric and measured treatment effect of study drug on associated symptoms. This design is superior to how many migraine drugs were approved over a decade ago where patients were simply asked if they had nausea, phonophobia, or photophobia regardless of the severity or presence at baseline. It's important to note that both the primary and key secondary endpoints of SAMURAI conform to the FDA’s Draft Guidance for Industry, Migraine: Developing Drugs for Acute Treatment, issued in October 2014.

- How do these data compare to existing treatments?

That's a good question because all the triptan drugs are generic and will likely cost pennies on the dollar compared to lasmiditan. Above, I noted that roughly three-fourths of these patients are dangerously taking triptans despite alarming risk factors or contraindications. The clinical data from the sumatriptan Phase 3 studies suggest half these patients fail the drug, although these studies are now nearly three decades old (Imitrex was approved in the U.S. in 1991).

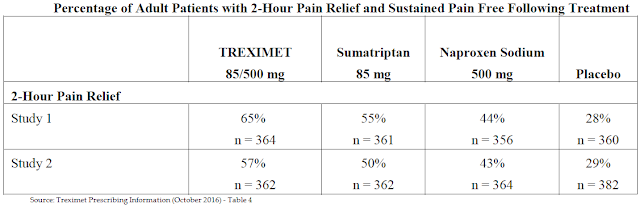

The most recent migraine study we can compare the SAMURAI data to is the Treximet clinical program conducted by Pozen/Glaxo roughly a decade ago (Treximet was approved in 2008). This is an excellent comparison because the study not only looked at the 2-hour pain relief of Treximet but also the individual components of sumatriptan and naproxen.

Treximet is a powerful drug. The data show it is superior to both sumatriptan and naproxen when taken individually; and, although cross-trial comparisons are clearly imperfect, perhaps a bit better than for lasmiditan (57-65% vs. 60%). That being said, Treximet's Black Box warning for potential GI and CV events caps broad-scale use of the drug. Lasmiditan may not have the efficacy punch of Treximet, but it should be far sensible for most patients.

- It sounds like safety is a key differentiator for lasmiditan. What was the AE profile of the drug in SAMURAI?

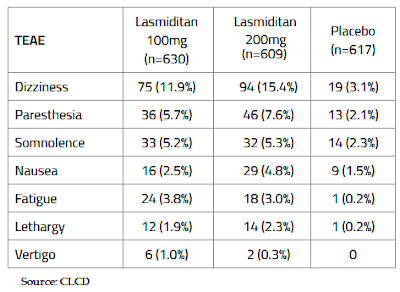

Lasmiditan was well tolerated, with the majority of treatment-emergent adverse events (TEAE) being nervous system related, and 91% of TEAE in lasmiditan treated patients being described as mild or moderate in nature. Importantly, there was not a significant increase in cardiovascular adverse events in patients who dosed with lasmiditan versus placebo. There were no serious adverse events in SAMURAI that were considered to be related to treatment. The following table sets forth the percentage of patients who experienced the specified adverse event within the safety population for each dose.

- But this was a single-dose study, correct?

Yes, SAMURAI was a single dose, 100 mg or 200 mg of lasmiditan or placebo, study. So it is fair to say no one was really expecting an increase in cardiovascular events after only a single dose of the drug. By comparison, the FDA placed a Black Box on Treximet for potential GI risk due to the naproxen component and the increase in risk of upper gastrointestinal complications that occurs with chronic dosing.

CoLucid is current conducting a long-term, open-label extension study to SAMAURI called GLADIATOR. The purpose of GLADIATOR is to further qualify the safety of lasmiditan over long-term, chronic pro re nata use. GLADIATOR will also satisfy FDA requirements on patient safety data necessary for the New Drug Application (NDA). Although the data to date has been highly encouraging with respect to the safety of lasmiditan, it is not until the results of GLADIATOR are made available that we will truly get a sense of the long-term safety of the drug. CoLucid expects over 2,500 patients to randomize into the program, which is expected to provide over 15,000 patient exposures to the drug for the U.S. NDA filing.

CoLucid provided an update to GLADIATOR in late September 2016. To date, 1,155 patients have been enrolled in GLADIATOR, a retention rate of an impressive 74% from SAMURAI. Lasmiditan 100 mg and 200 mg doses have been administered collectively over 7,500 times. Investigators report the drug has been well tolerated with no significant increase in cardiovascular adverse events in patients see to date.

- What's next?

Along with GLADIATOR, CoLucid is currently conducting a second Phase 3 program called SPARTAN. SPARTAN is nearly identical to SAMURAI, only the trial also includes a 50 mg dose of lasmiditan so that management can further explore the efficacy range of the drug and potentially expand the label to elderly patients above the age of 65. This is a population ineligible for current triptan use. I expect management will keep shareholders updated on SPARTAN over the next few months. The trial is likely to complete enrollment in early 2017 and report topline data around the middle of 2017.

Investors should note that both SAMURAI and SPARTAN are being conducted under a special protocol assessment (SPA) agreed upon by the U.S. FDA. Assuming the SPARTAN data matches up well with the positive SAMURAI data, CoLucid should be in position to file the lasmiditan NDA during the first half of 2018. The added time between the topline readout of SPARTAN and the filing is to allow management to complete all the necessary CMC work for the U.S. application. In the meantime, I would expect management to present the full data analysis from SAMURAI during the first half of 2017. Important and relevant medical conferences include the American Academy of Neurology (AAN) meeting in April 2017 and the American Headache Society (AHS) meeting in June 2017.

- Ok, this sounds very interesting... but what about that entirely new class of migraine antibodies being developed by several big pharma players?

Ah, you're asking about the calcitonin gene-related peptide (CGRP) receptor antagonists! Yes, several pharmaceutical companies, including Teva, Alder, Eli Lilly, Novartis, Amgen, and Allergan are developing CGRP inhibitors in Phase 3 clinical trials. Teva, Alder, Lilly, Amgen, and Novartis are developing monoclonal antibodies that inhibit CGRP. Allergan has an oral receptor antagonist also Phase 3 under development. It's an entirely new approach to migraine prevention.

The upside to the CGRP mAbs is they have no vasoconstrictive properties, fewer adverse effects, and may act longer than triptans. However, their development has been complicated by liver toxicity issues. Merck discontinued a CGRP receptor antagonist, telcagepant, because of liver toxicity in 2011. Merck decided to exit the space entirely, selling its backup compound, ubrogepant, to Allergan for $250 million in cash, with an undisclosed milestone and royalty backend in 2015.

Teva, Alder, Eli Lilly, Novartis, Amgen, and Allergan are hoping that the liver toxicity seen with telcagepant is not a class effect. There's precedent on both sides of this argument. Some very large drugs have had chemical cousins discontinued to even pulled from the market due to safety concerns (e.g. rosiglitazone and pioglitazone vs. troglitazone or celecoxib vs. rofecoxib)

The thing investors need to understand about the CGRP inhibitors is that they are being developed for migraine prevention, not acute treatment. Lasmiditan, Treximet, and the rest of the triptans are primarily used as acute treatment options. According to a paper published in Neurology by Lipton et al., 2007, only 13% of triptan use is for prophylactic therapy. The drugs are simply too dangerous to use on a regular basis. In fact, the label for Imitrex specifically states it is not to be used prophylactically and that use in excess of 10 days per month might actually exacerbate migraine frequency and symptoms!

So the CGRP inhibitors are really a new market opportunity. It is conceivable that of the 2 million patients currently taking medications for acute treatment of migraines, many will try approved CGRP inhibitors assuming they work and are safe. Below is a snapshot of the Phase 2b data from Alder BioPharmaceuticals (NASDAQ: ALDR) showing the effectiveness of ALD403, a CGRP monoclonal antibody, in reducing migraine "days per month" in at-risk patients.

The results are only statistically significant for the top doses tested and likely only clinically meaningful at the 50% reduction level. So even if we assume that CRGP inhibitors capture 50% market share (1 million patients) and are only moderately effective (placebo-adjusted) in reducing migraine days by 50%, this new class of drug will only remove about one-quarter of the patients 50% of the time. That's 125,000 patients or 6.25% of the addressable market.

But I think investors need to view the bigger picture here. Right now there are hardly any major players actively promoting migraine drugs. Allergan does run some DTC advertising with Botox® but it is mostly print and sparse. The triptans are all generic and Pernix Therapeutics does not have the marketing muscle to move the needle with Treximet alone. Investors need to appreciate the potential growth in both the diagnosed patient population and population on medications once some big, heavy-hitters like Teva, Amgen, Allergan, and Eli Lilly come to market.

- So you believe that new prophylactic options may actually increase use of acute treatment options?

It's the size of the pie. I think once CGRP inhibitors are approved and companies like Teva, Amgen, Allergan, and Lilly - certainly all no strangers to DTC advertising - are out promoting their respective drugs, the migraine pie gets significantly bigger. I think we could go from 4 million patients diagnosed to 5-6 million in only a few years. I think the number on medication easily goes from 2 million today to 3-4 million in a few years, thanks to the power of big pharma marketing.

Once a patient is diagnosed, they are now fair game for CoLucid and lasmiditan. Once a physician is talking to their patient about all the available options for migraine treatment, whether it be for acute and prophylactic use, I think lasmiditan gets a slice of that pie.

In a sense, this reminds me of the asthma market with Advair®, approved for prevention of asthmatic events, and short-acting beta2-agonist that are used as rescue medications. Patients with severe asthma do not stop carrying rescue medication simply because they dosed Advair earlier in the day. The same can be said for diabetics that dose basal insulin like Lantus®. These patients still require bolus insulin like Humalog® at mealtime.

- So what are we looking at in terms of market size?

As noted above, I think the diagnosed market goes from 4 million to 6 million rather quickly in the coming years. Even if we maintain the "50% on drug" ratio, the market size should increase from 2 million to 3 million patients, and I think that is being very conservative.

- How big a drug do you see lasmiditan becoming? What are peak sales?

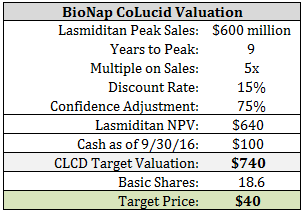

At this stage, the peak sales for lasmiditan are not easily calculable. Although the data from SAMURAI look very good and compare well to the data from Imitrex and Treximet, in a perfect world I'd like to see the full data from GLADIATOR and SPARTAN before I built a detailed model. That being said, it's not a perfect world so we'll have to make do with what we have.

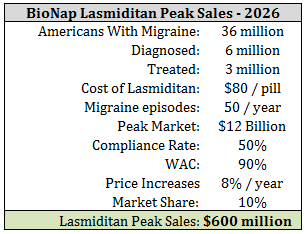

I'll start by assuming 3 million patients on therapy by 2020. I assume the average migraine sufferer has 4 episodes per month or 50 episodes per year. I think this is the level at which a patient will seek medical attention. If we price lasmiditan at parity to Treximet® at $80 per pill, the yearly cost per patient, assuming 100% compliance (a false premise), is $4,000. This would suggest a peak market of $12 billion.

We need to make several adjustments to that figure, including the fact that 1) $80 is patient (insurance) cost and not AWC to CoLucid, 2) CoLucid will likely provide significant co-pay support for lasmiditan users, at least early on in the launch, and 3) compliance rates are probably more like 50% per patient than 100%. We also need to come up with a reasonable market share, which I forecast to be 10%. Multiplying all this through and we arrive at potential peak sales for lasmiditan at roughly $600 million.

- Do they have cash?

Yes, plenty! The company raised nearly $70 million in September 2016. I expect them to report over $100 million in the bank as of September 30, 2016, when they report third quarter financial results in the coming weeks. I find this to be sufficient to complete GLADIATOR and SPARTAN and position the company for approval of lasmiditan after the U.S. NDA filing. Once the application is under review, I think we will see either a take-out or commercial partnership for the drug.

- What do you think CoLucid is worth?

What CoLucid is worth is based off an assumption of what the peak sales of lasmiditan might be, and since I've already stated above that this is difficult to forecast at this stage, please keep in mind that my valuation is equally as imperfect as my peak sales assumption. That being said, if I'm correct that lasmiditan has peak sales of $600 million in 2026, then I think CoLucid is undervalued today.

My assumptions can be seen below.

Some final points on the valuation of CoLucid need to be made. As the data from GLADIATOR and SPARTAN become available, my confidence level should increase. So, investors can assume there is upside beyond $40 per share based on the successful outcome of these ongoing programs. Secondly, as we get closer to the NDA filing and eventual approval of lasmiditan, the confidence level increases and the time-value discount shrinks.

On a relative valuation basis, I noted in 2015 that Allergan paid Merck $250 million for ubrogepant. The drug had only Phase 2 data and its cousin, telcagepant was discontinued only a few years earlier for liver toxicity issues. Merck is also due development and regulatory milestones plus royalties on sales from Allergan, so the NPV of the ubrogepant deal was likely $400-500 million. That's not too far below what investors are paying for CoLucid today, and lasmiditan has completed its first Phase 3 trial.

Additionally, Alder BioPharmaceuticals is currently worth $1.4 billion, over twice what CoLucid is worth today and Alder is now only conducting its Phase 3 program with ALD403. It is fair to say that investors are assuming the prophylactic market will be significantly larger than the acute treatment market if CGRP inhibitors are successful, but as of today, that is a rather big leap of faith considering 87% of the current migraine market is for acute use only. Alder's $1.4 billion market value for a Phase 3 migraine drug, knowing that they are likely to battle some rather big players in Amgen, Allergan, Lilly, and Teva, is perplexing relative to CoLucid's $600 million value. In this light, my calculation for a fair value of CoLucid at $740 million (i.e. $40 per share) looks rather conservative.

Please see important information about BioNap and our relationship with CLCD in our Disclaimer.

BioNap holds no position in ...

more

What does everyone think of this idea?

I like the idea and like how you formatted the article itself. You did a good job of outlining the problem as well as the opportunity, while explaining everything along the way.