Image Source: Unsplash

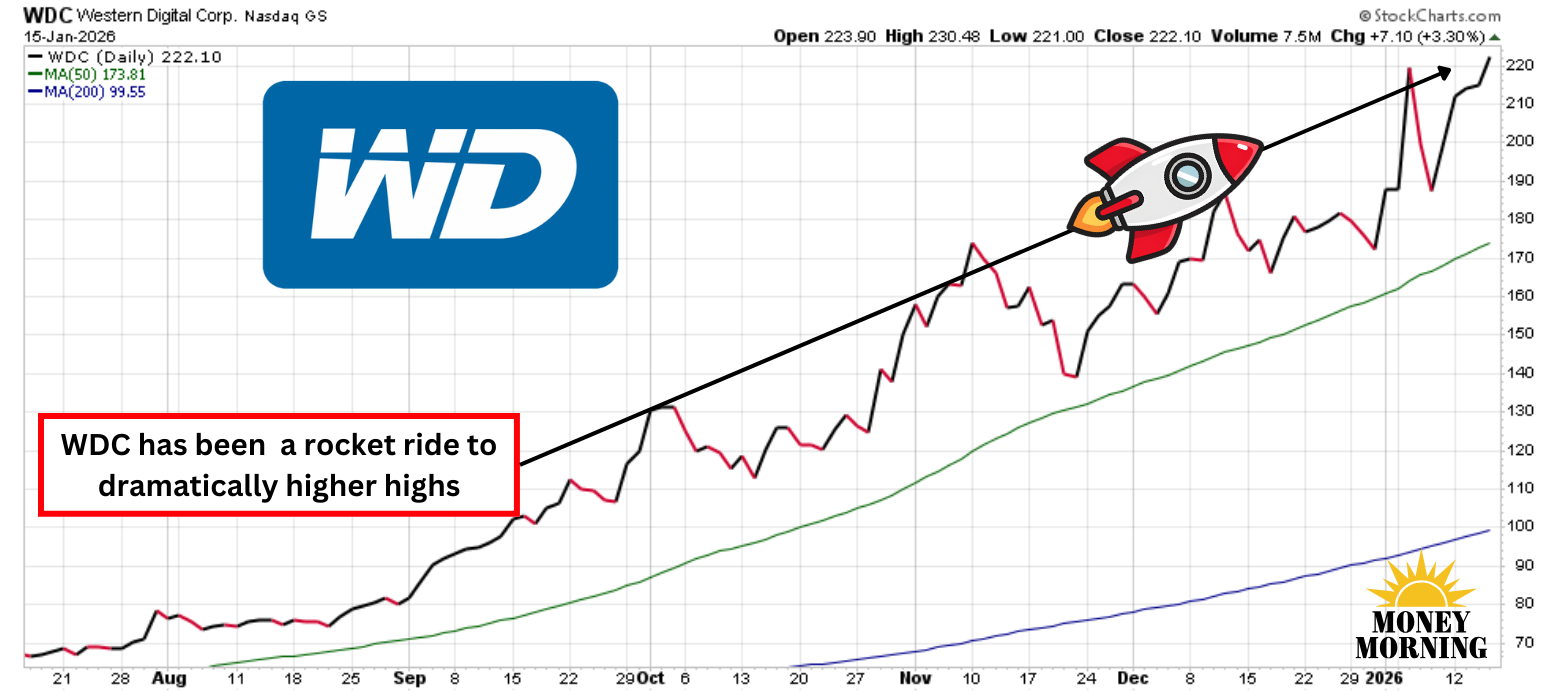

Western Digital (WDC) capped 2025 as one of the S&P 500's top-performing stocks, surging an astounding 282% and outpacing the index's 16% gain. It was only edged out by SanDisk (SNDK), which it had spun off earlier in the year and which rode similar AI-driven tailwinds.

This momentum has spilled into 2026, with WDC shares climbing 29% in just the first two weeks of the year. Wall Street is fully on board, with analysts repeatedly hiking price targets as the stock blasts through prior levels. Yet, amid this rocket-like ascent, investors are wondering whether this AI-fueled ride can continue, or is a sudden crash landing on the horizon?

Fueling the Ascent: Partnerships with Hyperscalers

WDC's surge is powered by its pivotal role in the AI data explosion, particularly through deepening ties with hyperscalers – the massive cloud providers like Amazon (AMZN), Google, and Microsoft (MSFT) that crave ever-greater storage capacity. These partnerships are fortifying WDC's competitive moat, as AI applications, including multimodal large language models and agentic systems, generate unprecedented data volumes.

All seven of WDC's top hyperscaler customers have issued purchase orders for next-generation Heat-Assisted Magnetic Recording (HAMR) drives through the first half of 2026, with five extending through the full year and one securing supply into 2027.

WDC fills this need with cutting-edge solutions like enterprise Perpendicular Magnetic Recording (ePMR) drives, offering up to 26 terabytes (TB) in conventional magnetic recording (CMR) and 32TB in Ultra Shingled Magnetic Recording (UltraSMR) formats. Shipments of these exceeded 2.2 million units in the September quarter alone. HAMR technology, set for a volume ramp-up in early 2027, promises even higher capacities.

Hyperscalers turn to WDC for its reliability, scalability, and superior total cost of ownership (TCO), which optimize massive data center builds as AI demands soar. This positions WDC as a go-to supplier in a market where data growth shows no signs of abating.

(Click on image to enlarge)

Analysts Keep Raising the Bar

Bullish sentiment is echoed on Wall Street, where analysts are scrambling to keep up with WDC's momentum. Wells Fargo recently boosted its target from $180 to $260, implying 21% upside from pre-upgrade levels, while maintaining an overweight rating. Barclays reiterated its overweight call, lifting its target to $240 from $200. Last month, Morgan Stanley hiked its target to $228.

With shares jumping over 4% in premarket trading today to around $231 – already surpassing Morgan Stanley's mark – more upgrades could follow as earnings revisions trend upward. The consensus remains a strong buy, with targets averaging $183.50 but climbing.

Bottom Line

Despite a 368% gain over the past year, WDC trades at a discounted 23x forward earnings and less than 1X its long-term earnings growth rate of 33%. The AI data center buildout shows no slowdown – Taiwan Semiconductor Manufacturing's (TSM) earnings yesterday suggests it is actually picking up steam. With robust hyperscaler orders and innovative tech like HAMR on deck, WDC appears to have plenty of fuel left in the tank for a continued ascent.

More By This Author:

Bitmine Immersion Makes $200 Million DeFi Bet On MrBeast

With $100 In Sight, This Is The Best Silver Play Today

Why Marathon Petroleum Will Be The Biggest Winner In Venezuela

Comments

Log in or sign up to join the conversation.