Berkshire Hathaway (BRK-B) has an equity investment portfolio worth over $360 billion, as of the end of the 2022 first quarter.

Berkshire Hathaway’s portfolio is filled with quality stocks. You can follow Warren Buffett stocks to find picks for your portfolio. That’s because Buffett (and other institutional investors) are required to periodically show their holdings in a 13F Filing.

As of March 31st, 2022, Buffett’s Berkshire Hathaway owned over half a million shares of Mondelez International (MDLZ) for a market value of $36 million. Mondelez represents about 0.1% of Berkshire Hathaway’s investment portfolio. This marks it as one of the smallest positions in the portfolio.

This article will analyze the consumer defensive company in greater detail.

Business Overview

Mondelez was formed in 1989 as a result of the merger between Philip Morris and General Foods Corp. The company has undergone a slew of mergers and spinoffs since that time, including its North American grocery business, which was called Kraft Foods. That unit is now part of Kraft Heinz (KHC) and the remainder of the business is what we know as Mondelez today.

On April 26th, Mondelez reported first quarter 2022 results. Net revenue rose 7.3% year-over-year, driven by organic net revenue growth of 8.6%. Adjusted earnings per share was $0.84 for the quarter, a 6.3% year-over-year improvement over $0.61 in the prior year period.

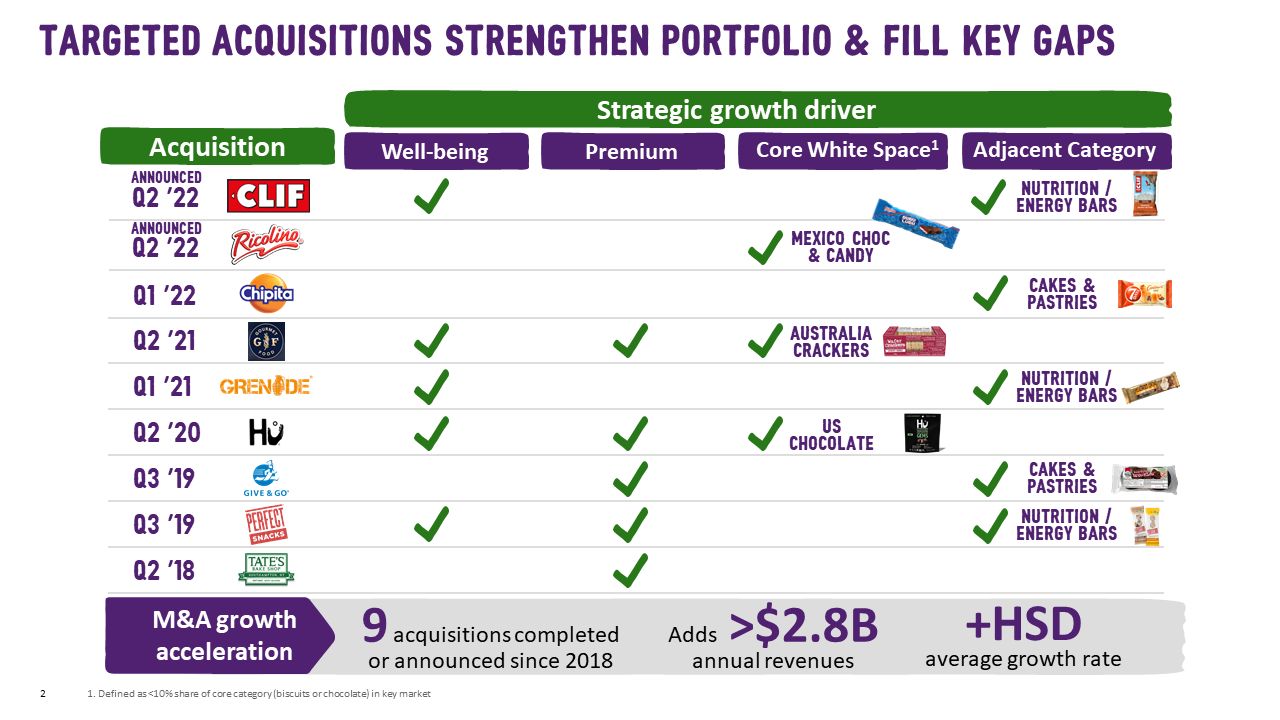

Subsequent to the quarter-end, Mondelez announced the acquisition of Clif Bar & Company for $2.9 billion with additional contingent earnout consideration. This acquisition expands the company’s presence in baked snacks and follows the company’s game plan to focus on faster growing food segments.

Latin America saw the strongest organic net revenue growth of 25.7%, as a result of pricing and vol/mix. Second strongest organic net revenue growth of 8.9% was in Asia, Middle East, & Africa, followed by 7.7% growth in North America, and 4.9% growth in Europe.

Mondelez provided updated 2022 guidance which sees 4+% organic net revenue growth, and mid-to-high single-digit adjusted EPS growth on a constant currency basis. Mondelez also expects more than $3 billion of free cash flow.

We estimate that Mondelez International can generate $3.04 in earnings-per-share for the fiscal 2022 year.

Growth Prospects

Since the spinoff, Mondelez has seen a steady EPS growth of 8.3%. The company has actively bought back a large number of shares. Since 2018, Mondelez has cumulatively repurchased $7.0 billion worth of shares. We expect the company to continue repurchasing shares, as it is embedded in their shareholder return programs.

Additionally, Mondelez’ has a good history of organic revenue growth, which should continue. The company has employed cost reductions in the past and is now focusing on accelerating the business and its brands. Specifically, the company intends to focus on the core of biscuits and chocolate.

Source: Investor Presentation

The company holds a not insignificant market share in the biscuits and chocolate businesses, at 17% and 12%, respectively. Additionally, Mondelez will attempt to bolster its small market share in the candy business, where it currently only holds a 5% share.

Mondelez will also continue to acquire strong brands to add to their portfolio, such as the recent acquisition of Clif Bar & Company. This acquisition has created a $1 billion global snack bar business for Mondelez which positions it well to generate higher long-term growth.

Source: Investor Press Release

The company’s exposure to emerging markets is likely to experience higher organic net revenue growth in the high single digits versus the typically low single-digit growth at the company’s developed markets.

However, operating costs could weigh somewhat on earnings growth if energy prices remain relatively high versus the past few years.

We estimate Mondelez can grow earnings at a 7.0% average annual rate over the intermediate term, assuming that international markets will continue to drive growth in a more normalized economic environment.

Competitive Advantages & Recession Performance

Mondelez is a market leader in processed foods worldwide. The company boasts its geographical footprint, with about one third of revenues coming from high-growth emerging markets, as a competitive advantage. Additionally, it operates in attractive and resilient categories in the food business, and has strong, iconic brands with pricing power.

Mondelez operates in resilient food categories, and given the consumer staple products it sells, it should be fairly resilient to recessions. However, this does not mean we see Mondelez as immune to recessions.

Mondelez has raised its dividend for eight consecutive years so far. Mondelez’ dividend payout ratio is below 50% of earnings today. The payout is safe, so we don’t expect a dividend cut to be a material risk, even in a recession. The company was able to generate free cash flow north of $3 billion even during the pandemic year of 2020. We expect continued dividend growth from Mondelez that matches its earnings growth.

Valuation & Expected Returns

Shares of Mondelez have traded for a 5- and 10-year average price-to-earnings multiple of 20.0 and 21.0, respectively. Shares are now trading in between both of these averages, which indicates that shares could be near fair value at the current 20.7 times earnings. However, we prefer to remain conservative, and peg fair value at the lower range.

Our fair value estimate for Mondelez stock is 20.0 times earnings. If this proves correct, the stock will incur a -0.6% annualized loss in its returns through 2027.

Shares of Mondelez currently yield 2.2%, which is just above its 5- and 10-year average yields of 2.1%. On a dividend yield basis, Mondelez shares seem to be trading at roughly fair value.

Putting it all together, the combination of valuation changes, EPS growth, and dividends produces total expected returns of 8.4% per year over the next five years. This makes Mondelez International a hold.

Final Thoughts

Mondelez International is a leader in processed foods and has just made a significant acquisition with Clif Bar & Company. Being a consumer defensive business, it has held up well against the broader market so far in 2022, as it has shed only -5% of its share price.

The company appears to be trading near its fair value, but its growth catalysts remain intact. The dividend, while higher than the broad market at 2.2%, is not overly impressive. Due to the rich valuation in Mondelez shares today, it may be better to wait for a dip before initiating a position.

More By This Author:

Warren Buffett Stocks: Marsh & McLennan

Warren Buffett Stocks: Markel Corporation

Warren Buffett Stocks: Johnson & Johnson

Comments

Log in or sign up to join the conversation.