Image Source: Mike Mozart, Flickr

At Walmart (WMT), boring is the new fabulous. The $390 billion retailing giant is a bellwether for consumer spending. So, it would follow that, as wallets become pinched, low growth and slim margins would be cause for concern. But Walmart benefits from being big, established, and, importantly, profitable, and the latter can’t be said for Amazon.com’s retail business. As the shine comes off of technology companies, Walmart’s failures are an afterthought.

The company led by Doug McMillon warned on Tuesday that a lack of visibility into its shoppers is causing Walmart to exercise caution. U.S. sales for the same set of stores are expected to rise to 2.5% in the company’s fiscal year which ends in January, the high end of Walmart’s guidance, but below analysts’ expectations of 3%, according to Refinitiv. Profits meanwhile are getting crunched. Earnings per share for the year are expected to be at least 45 cents lower than what the Street is forecasting.

The problem is that consumers are shifting their spending to groceries versus general merchandise, and food inflation is still stubborn. Walmart’s commitment to keeping prices low is reflected in its operating margins which currently hover at a slim 3%. To make up for operating statis, Walmart is casting about for new sales streams including advertising, which Cowen reckons could have a chunky margin of 30%. But any effects won’t kick in until after January 2024.

In isolation, that all seems bad. But in a beauty contest of retailers, Walmart looks decent. Amazon earlier this month reported an operating loss of $2.8 billion in its North American region last year. That is the e-commerce giant’s retail group, and it accounted for more than 60% of the top-line sells.

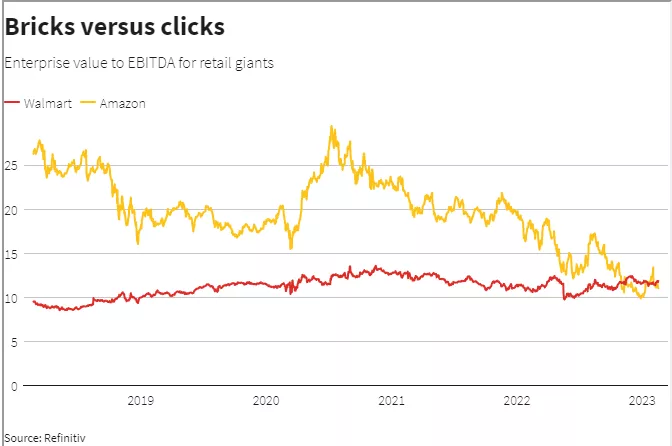

Meantime while the brick-and-mortar colossus’s Prime-like membership has failed to get off the ground – it represents less than 1% of the top line – that’s less of an issue when technology companies have fallen out of favor. Walmart’s enterprise value to this year’s EBITDA, at 12 times, is a hair more than Amazon’s. The ho-hum is having its moment.

Context News

Walmart reported on Feb. 21 that revenue for the quarter ending January rose 7.3% year-over-year to $164 billion. Comparable sales at its U.S. stores, excluding fuel, increased by 8.3%. Net earnings were $6.3 billion, compared with $3.6 billion in the same quarter in 2022. The company expects U.S. comparable store sales to increase 2% to 2.5% for the year ending January 2024 and adjusted earnings per share to be in the range of $5.90 to $6.05. Analysts are forecasting U.S. same-store sales of 3% and EPS of $6.50, according to Refinitiv.

More By This Author:

S&P 500 2022 Q4 Earnings Review: Swing And A MissSTOXX 600 Earnings Outlook 22Q4 - Tuesday, Feb. 21

Q4 2022 U.S. Retail Scorecard - Update

Comments

Log in or sign up to join the conversation.