Image Source: Pexels

Markets are uneventful today on light holiday volume. Economic data detailing unemployment claims, pending home sales, retail inventories, and international goods trade failed to influence investor sentiment. Stocks are up slightly while bonds are selling off marginally as interest rates bounce.

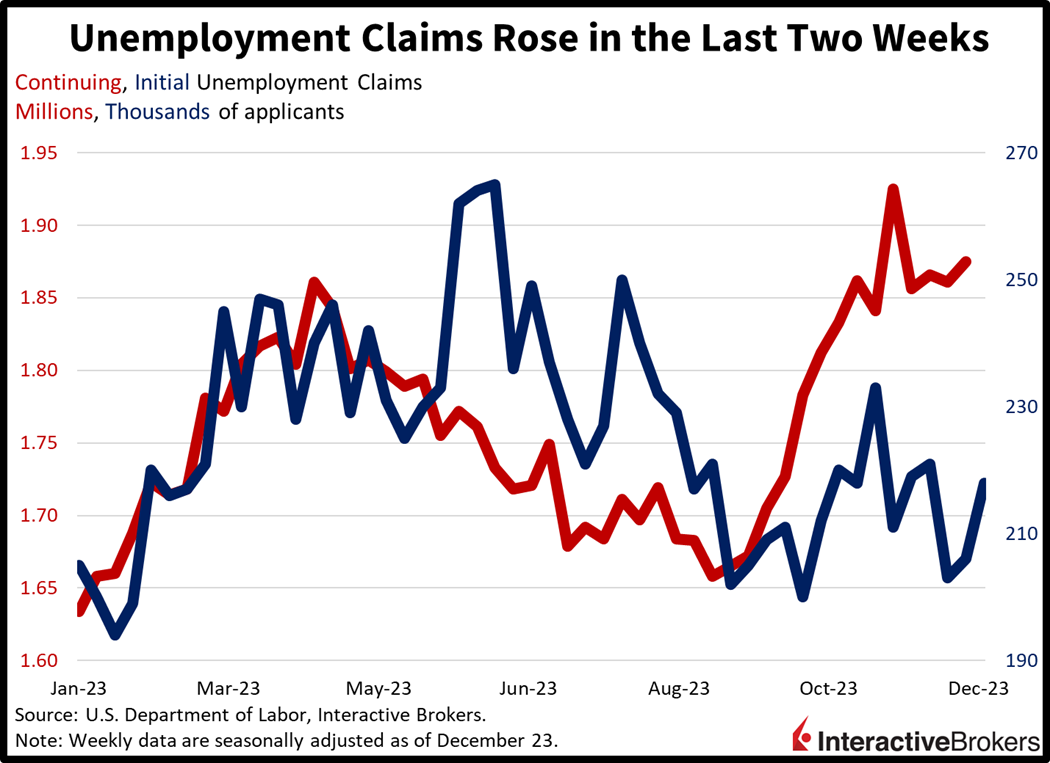

Unemployment Lines Extend

The labor market loosened in the last two weeks, as unemployment offices experienced higher traffic volumes. Initial unemployment claims totaled 218,000 during the week ended December 23, above the previous week’s 206,000 and exceeding the 210,000 projected. The four-week moving average did slip slightly, however, from 212,250 to 212,000. Continuing unemployment claims rose to 1.875 million during the period ended December 16, meanwhile, exactly as expected. The previous week’s figure came in at 1.861 million. Similar to initial claims, the four-week moving average for continuing claims dipped despite the increase in the weekly figure. The moving average declined from 1.877 million to 1.865 during the period.

Light Inventory Hampering Pending Home Sales

Softer mortgage rates couldn’t offset the tight supply story for the residential real estate sector last month, according to one data point. Pending home sales came in unchanged during November, despite economists anticipating a 1% month-over-month (m/m) pace of growth. November’s figure did arrive better than October’s 1.2% decline, however. Across regions, the West, Midwest and Northeast offered gains of 4.2%, 0.8% and 0.5% m/m. Unfortunately, a 2.3% decline in the South hampered progress.

Goods Sellers Trim Inventories

Persistent weakness in manufacturing led to both wholesalers and retailers decreasing their inventories last month. The retail inventory segment excluding automobiles declined 0.8% m/m, slipping at a slower rate than October’s 1.1%. Wholesalers saw their inventories drop 0.2% m/m, also a lighter rate of decline from October’s 0.4% fall.

From a trade deficit angle, the US’s goods trade balance dropped to $90.27 billion in November from $89.56 billion in October.

Markets Trade on Light Volumes

Markets are sluggish on light volume with most stock indices modestly higher, rates up and the dollar lower. For stocks, the Dow Jones, Nasdaq Composite and S&P 500 indices are up 0.1% each. The small-cap Russell 2000 Index is lagging, however: it’s down 0.3%. Sector breadth is mixed, as health care, communication services, utilities, financials and consumer staples trade higher while the other 6 segments are lower. Energy stocks are leading the downside, as the price of oil buckles on improving conditions near the Suez Canal; they’re down 0.9% as a group. Maersk, France’s CMA CGM and other large shipping companies are comfortable transporting products through the Red Sea at the moment. WTI crude oil is down 0.3%, or $0.22, to $73.56 on the news. The 2- and 10-year Treasury maturities are trading at 4.27% and 3.82%, 3 and 2 basis points (bps) higher on the session. The Dollar Index is down 2 bps to 100.94, as the US currency loses ground relative to the franc, yuan, yen, and Aussie and Canadian dollars. The greenback is gaining against the euro and pound sterling though.

Valuation is Dangerous Here

As we shift into 2024, the main risk to this market is valuation. I believe inflation (CPI) has troughed at 3% alongside bond yields at the long-end, which make the current valuation proposition unattractive and outright risky. A forward earnings yield of 5% (Forward P/E of 20) is too much to pay, considering that earnings estimates will be tough to achieve amidst a 10-year that is going back above 4%. Indeed, to meet earnings expectations, companies will have to trim labor, scale down operations and focus on margins due to revenue headwinds, activities that don’t promote longer-term growth. Next year is a down year, with the S&P 500 finishing at 4,100, on slower consumer demand, excessive optimism concerning Fed rate cuts and deficit fueled, higher-for-ever long-term interest rates.

More By This Author:

Real Estate Prices Will Keep Climbing Unless The Fed Stops Them

The Last Trade Before Christmas

Geopolitical Conditions Intensify Amidst Firmer Econ Data

Comments

Log in or sign up to join the conversation.