Summary

US Steel’s price pattern is closely related to the business cycle.

US Steel underperforms the market when business slows down.

US Steel will continue to underperform the market.

Image: United States Steel

United States Steel Corporation (X) produces and sells flat-rolled and tubular steel products primarily in North America and Europe. It operates through three segments: North American Flat-Rolled (Flat-Rolled), U. S. Steel Europe (USSE), and Tubular Products (Tubular).

The Flat-Rolled segment offers slabs, strip mill plates, sheets and tin mill products, as well as all iron ore and coke. This segment serves customers in the service center, conversion, automotive, construction, container, and appliance and electrical markets.

The USSE segment provides slabs, strip mill plate, sheet, tin mill products, and spiral welded pipes, as well as refractory ceramic materials. This segment serves customers in the construction, container, appliance and electrical, service center, conversion, oil, gas, and petrochemical markets.

The Tubular segment offers seamless and electric resistance welded steel casing and tubing products, as well as standard and line pipe and mechanical tubing products primarily to customers in the oil, gas, and petrochemical markets. The company also provides railroad services and real estate operations.

Source: StockCharts.com, The Peter Dag Portfolio Strategy and Management

The stock of US Steel shows a well-defined downtrend channel since 2007. The price behavior also shows considerable volatility. This volatility is not a random event. It represents the expectations of US Steel’s performance caused by changes in the business cycle.

The inventory cycle is helpful to explain why the price of US Steel responds to the business cycle.

Source: Profiting in Bull or Bear Markets - How Business Cycles Impact The Financial Markets

Business managers must filter all the news coming from different sources such as pandemics, cartels, supply chain difficulties, foreign or domestic supplier availability, trends in commodities and interest rates, changes in value of the dollar, and the Fed. Eventually they must make a crucial decision: how much to produce to replenish the inventories at levels needed to meet the demand for their goods.

The business cycle transitions through four phases as management changes its inventory policies. In Phase 1 and Phase 2 business decides to build inventories to meet growing demand. This decision results in increases in the purchase of raw materials, hiring more people, increase in borrowing to finance operations and improve and expand capacity.

This is the time the business cycle grows through Phase 1 and Phase 2. This is also the time commodities, copper, iron ore, other metals, crude oil, lumber, agriculturals, interest rates, and inflation rise. The increase in these prices is a testimonial the economy is strengthening.

The problem arises toward the end of Phase 3. The continued rise in commodities, copper, iron ore, other metals, crude oil, lumber, agriculturals, and in overall inflation eventually reduces consumers’ purchasing power in a meaningful way. The consumers’ response is a slowdown in spending.

The outcome is in Phase 3 managers begin to experience rising inventories compared to sales with a direct impact on their financial performance. The need to reduce inventories involves cuts in the purchase of raw materials, reduction in the workforce, and declines in borrowing. This process continues until inventories are in line with demand. The inventory to sales ratio keeps rising during these times as inventories rise faster than sales. During Phase 3 and Phase 4, because of the action of business, commodities, including iron and most metals, decline, wages slow down, and interest rates decline.

When inventories are finally adjusted to the desired level, matching their growth with the growth of demand, the business cycle transitions from Phase 4 to Phase 1. At this point the inventory to sales ratio starts declining again. It reflects sales rising faster than inventories. Business will have to increase production to restock inventories. And the business cycle moves to Phase 1. The markets will respond promptly.

US Steel acts positively to the forces driving the price of iron ore and other metals and labor costs when business is in the process of building up inventories (Phase 1 and Phase 2). This is the time price increases are likely to hold.

However, when the business cycle transitions into Phase 3 and Phase 4, demand for steel-based products such as autos declines, and profitability suffers. The price of the stock weakens reflecting these adverse times.

Sources: StockCharts.com, The Peter Dag Portfolio Strategy and Management

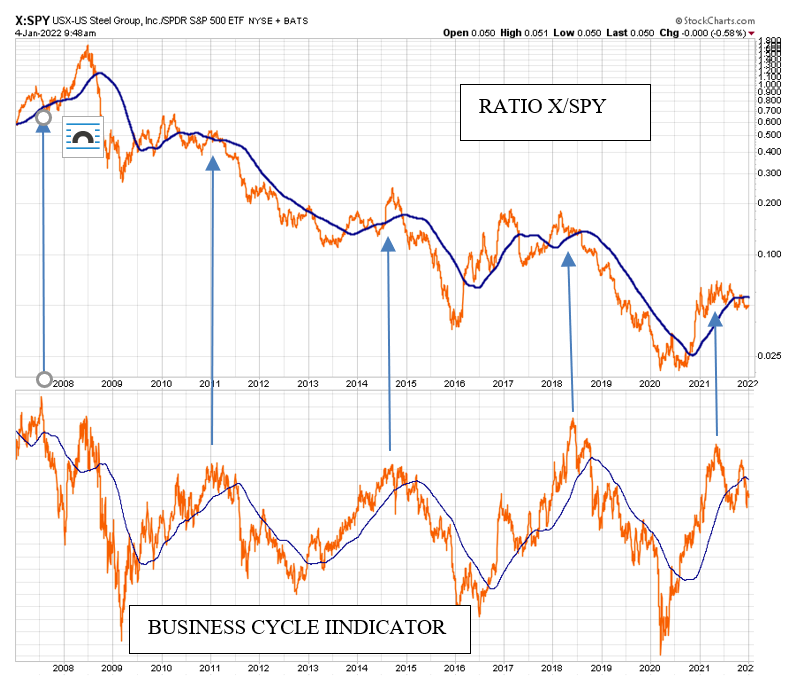

When does the price of US Steel outperforms the market? The above chart gives us the answer.

The above chart shows two panels. The graphs in the above panel represent the ratio between X and SPY. The second graph is its 200-day moving average. The graphs rise when X outperforms SPY. The graphs decline when X under-performs SPY. Investors are going to outperform the market if they invest in X when the graphs rise. The graph also indicates X has underperformed the market at least since 2007.

The bottom panel shows the business cycle indicator, a proprietary gauge updated regularly in The Peter Dag Portfolio Strategy and Management. This indicator is computed in real-time from market data. Its turning points coincide also with the cyclical turning points of the growth of employment in manufacturing and credit spreads.

The relation of X to the business cycle is quite telling. X outperforms the market when the business cycle rises, reflecting stronger economic growth and rising commodity prices. The ratio X /SPY declines, reflecting the underperformance of X relative to SPY, when the business cycle declines, reflecting slower economic growth and lower commodity prices.

The recent weakness in the business cycle indicator suggests X will continue to underperform SPY (the ratio will keep declining).

Key takeaways

- The business cycle will decline, reflecting slower economic growth. The slowdown is mostly driven by rising inflation, causing the decline in demand due to the contraction in consumers’ disposable personal income after inflation.

- X will continue to underperform SPY as long as the business cycle indicator declines.

- The business cycle indicator will rise following a decline of inflation. Growth in M2 must fall from the current 13% to about 6%. Real disposable income will also rise accompanied by improving consumer sentiment (University of Michigan survey).

- X will start outperforming the market at that time.

Comments

Log in or sign up to join the conversation.