Image Source: Unsplash

Market Wrap

Markets got a taste of concentration risk as one of only three companies (formerly) valued over $3 trillion fell out of bed as Nvidia (NVDA) fell 16.86% and took close to $600 billion of market value with it. The issue at hand was the announcement of DeepSeek, a Chinese Chat-GPT competitor that claimed to outpace the incumbent while using less hardware (processors) as well as less power. The prospect of lower GPU sales coupled with lower energy requirements hit Technology (-4.96%) and Utilities (-2.37%) hardest yesterday, with Industrials (-1.40%) and Energy (-1.04%) also feeling some pain. The remaining sectors ranged from a flat Materials (0.02%) to Consumer Staples gaining 2.69%.

Unsurprisingly, the Nasdaq Composite led broad equity indexes lower, dropping 3.07%, followed by the S&P 500 which shed 1.46% with Information Technology names contributing to just under 125% of the day's result, and the Russell 2000, closing 1.03% lower. The Dow was the only broad index left unscathed as it posted a 0.65% gain on the day.

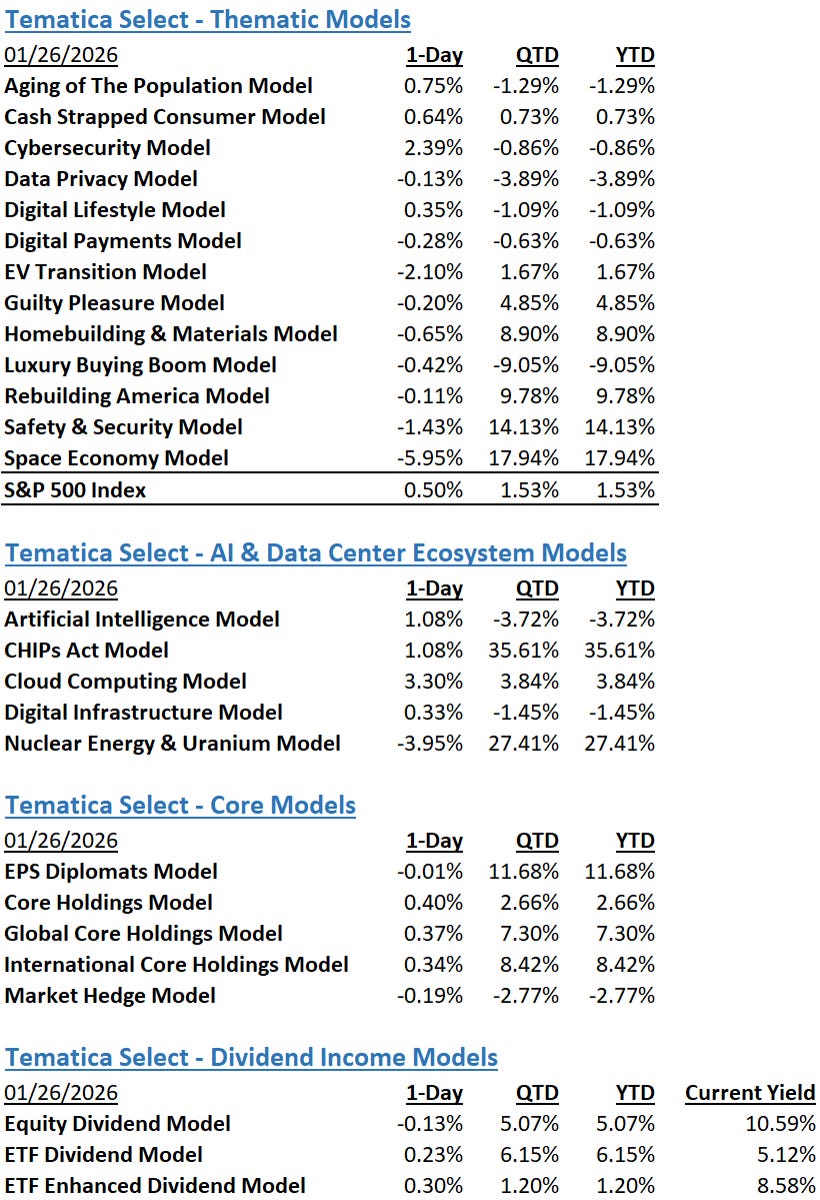

The Tematica Select Model Suite saw some pain in Digital Infrastructure and Nuclear Energy & Uranium yesterday and to a lesser extent, CHIPs Act, AI, and Cloud Computing. Still, the leaderboard saw Core Holdings, Homebuilding & Materials, and Guilty Pleasure fill out the first three slots with positive results and given the Cboe Market Volatility Index’s (VIX) 20% rise, we saw Market Hedge in the fourth slot.

Trump Tariff Indications, Earnings Accelerate, What to Watch

US equity futures point to a rebound following yesterday’s sharp sell off, with shares of Nvidia (NVDA) gaining in premarket trading helping pull the S&P 500 and Nasdaq Composite higher. Other than some rear view facing November housing price data and December Durable Goods Orders, the market will continue to focus on corporate earnings and potential Trump tariffs as it waits for tomorrow’s outcome of the Fed’s latest two-day policy meeting. On the earnings front we have Boeing (BA), General Motors (GM), Lockheed Martin (LMT), SAP SE (SAP), and Synchrony Financial (SYF) report), which should bring fresh data points for our Safety & Security, EV Transition, Artificial Intelligence, Cloud Computing, and Digital Payments models.

Asked about a report yesterday that incoming Treasury Secretary Scott Bessent favored starting with a global rate of 2.5%, Trump said he didn’t think Bessent supported that and wouldn’t favor it himself. Trump went on to say he wanted a rate “much bigger” than 2.5% indicating potential tariffs on semiconductors, pharmaceuticals, steel, copper and aluminum as well as automobiles from Canada and Mexico.

In what has become typical Trump fashion, the president appears to be keeping his options open sharing “I have it in my mind what it’s going to be but I won’t be setting it yet, but it’ll be enough to protect our country…” On the campaign trail last year, Trump indicated tariffs as high as 20%, but that is viewed as an extreme position. Growing speculation calls for a gradual introduction with moderate increases rather than stiff penalties out of the gate.

Our view is Trump and his administration needs to walk and talk tough to bring about new trade deals but not sabotage the economy and the battle against inflation. That’s a high tightrope without a net, and that has us keeping a close eye on the dollar, 10-year Treasury yields, and Fed Chair Powell’s comments tomorrow afternoon.

(Click on image to enlarge)

(Click on image to enlarge)

More By This Author:

Trump’s WEF Address, Earnings Season ContinuesDigesting Trump’s Early Actions, Earnings Season Comments

More Big Bank Earnings, TSM Reports, December Retail Sales Ahead

Comments

Log in or sign up to join the conversation.