Image source: Pixabay

If you gauged yesterday’s results by broad equity index returns you would think that it was an overall a flat day with a slight negative bias toward technology. The Dow ended flat, the S&P 500 declined 0.27% and the Nasdaq Composite dropped 0.50%. The reality is that markets have a lot of moving parts and even more levers that can influence those parts. One of those levers is crude oil prices, and while the Energy sector is only about 3% of the weight of the S&P 500 index, crude price changes reverberate far and wide through the rest of that index. Sectors were essentially lower across the board except for 3 which were essentially flat and Energy, which gained 1.45% on crude prices rising just under 5% on news of the State Department recalling non-essential personnel from Iraq.

The SPDR S&P 500 ETF Trust (SPY) fell 0.29% as 5 of the Mag 7 including Home Depot (HD), Walmart (WMT), Intel (INTC), and Berkshire Hathaway (BRK-B) accounted for 125% of the fund’s returns. Fighting this drag included Microsoft (MSFT), Broadcom (AVGO), and in a dichotomy of sorts, both Philip Morris (PM) and UnitedHealth Group (UNH). Despite the implications of crude’s move today, gold only picked up about $30 to $3,353.59/oz and the Cboe Market Volatility Index (VIX) added a mere 0.21 points to 17.16.

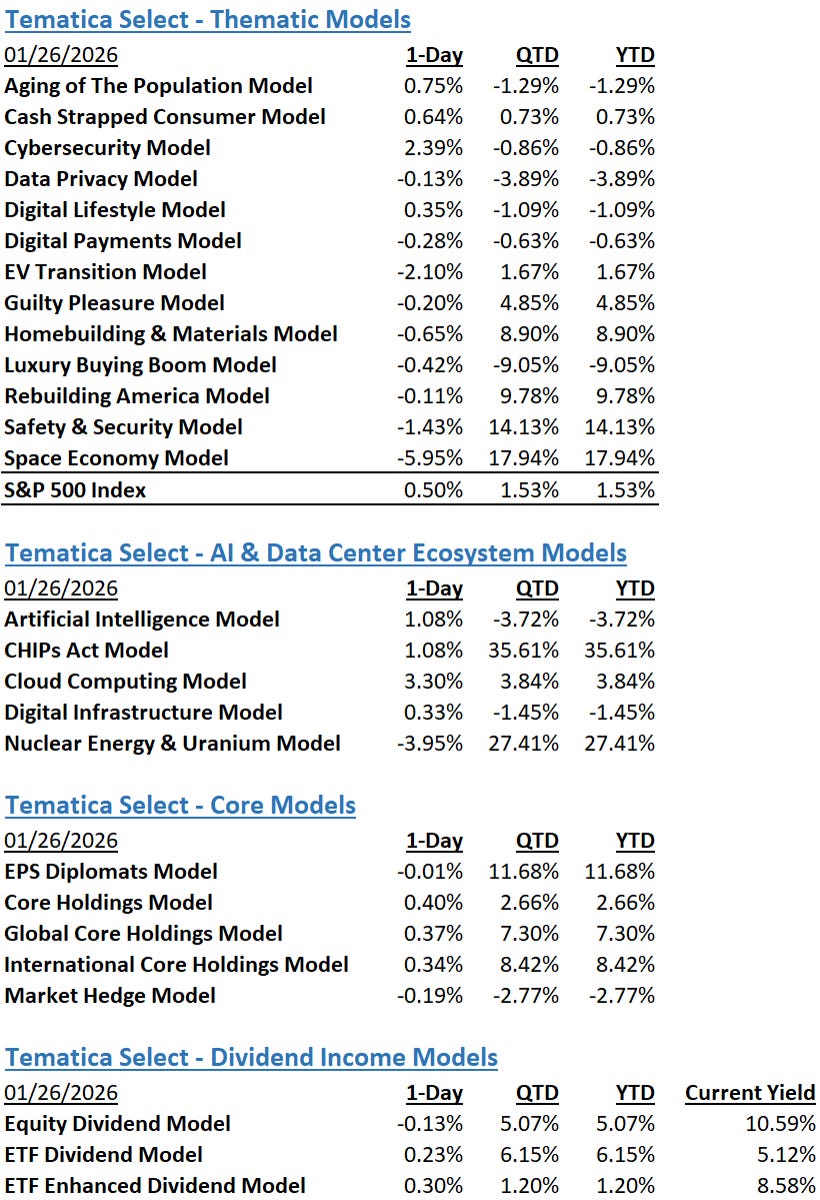

Markets as viewed through the Tematica Select Model Suite also told a more nuanced story with clear leadership coming from Nuclear Energy & Uranium (NUKE) while Safety & Security (SAFE), Space Economy (SPACE), and Guilty Pleasures (GUILT) among a number of other strategies posted gains. Yesterday’s laggards included Cash Strapped Consumer (PINCH), EV Transition (EVTRANS), and Homebuilding & Materials (HOMES).

Trade Deal Realities Bring Potential Market Headwinds

US equity futures point to a down open, continuing the market’s move lower yesterday, as rising tensions in the Middle East add to investors seeking more clarity on Washington's recent trade deals with China. Yesterday, President Trump shared on social media that a deal was done, and markets responded by giving up its gains following reports that China is putting a six-month limit on rare-earth export licenses for U.S. automakers and manufacturers. We’d like to say we’re surprised, but if you’ve been closely following our comments, you know we are not shocked to see this wrinkle.

Reports suggest the U.S. and China have until August to negotiate a broader trade agreement, and that deadline could be extended. This timing reaffirms our view that we are likely to see companies issue cautious guidance when they report their June quarter earnings season if they decide to issue guidance at all. Should we see U.S.-China trade discussions get extended as well, the potential for which we flagged in Wednesday morning’s comments, it would support corporate guidance skewing more conservatively.

To reclaim some positioning, President Donald Trump shared intentions to send letters to trading partners in the next one to two weeks setting unilateral tariff rates, ahead of a July 9 deadline to reimpose higher duties on dozens of economies. Adding to that, early this morning, Commerce Secretary Howard Lutnick indicated the European Union is likely to be among the last deals that the US has completed. Mixing in timing shared by Treasury Secretary Scott Bessent a few weeks back, Lutnick’s comment suggests any deal could be stretched well into 2H 2025, adding to our thinking 2H 2025 expectations may need to be reset.

Offsetting those concerns, shares of Oracle (ORCL) are up in premarket trading after the company raised its annual revenue forecast, driven by strong demand for its AI-related cloud services. For fiscal 2026, Oracle expects total revenue to be at least $67 billion, CEO Safra Catz said on a post-earnings call. With the new forecast, annual revenue is expected to grow by around 16.7%, compared with Oracle's prior projection of a 15% growth. Per Catz, the company expects its "total cloud growth rate — applications plus infrastructure — will increase from 24% in fiscal year 2025 to over 40% in fiscal year 2026…” We see that as a nice boost not only to our Artificial Intelligence model but to our Digital Infrastructure and Cloud Computing strategies as well.

Coming up at 8:30 AM ET, the May PPI data will be released, and it is expected to show sequential increases for headline and core figures. Instead of seeing sequential increases on a month-over-month basis for both headline and core CPI, the published figures showed not only sequential declines but increases of just 0.1% for both headline and core. The year-over-year figures were also lower than the market expected, with May core CPI at 2.8%, unchanged compared to April, while the headline figure ticked up to 2.4% from 2.3% in April, but less than the 2.5% expected by the market.

To say those cooler figures were not expected by the market, would be an understatement. Falling energy prices were a contributor, but we also saw declines in new car and apparel prices, which is counter-intuitive given implemented tariffs. What we’re likely seeing in the data is a combination of companies chewing through existing inventories, and some retailers leaning into promotions and discounting to drive comp sales. Walmart (WMT), e.l.f. Beauty (ELF), Best Buy (BBY), Ford (F), Procter & Gamble (PG), Macy’s (M), and Mattel (MAT) have either recently enacted tariff-related price hikes or plan to do so.

We continue to think the longer we go without trade deals and their agreed-upon and final details, the more likely we will see a more pronounced impact of existing tariffs in the data, on the economy and earnings expectations for 2H 2025. So far, forecasted consensus EPS growth for 2H 2025 reduced to 8.5% exiting May from 10.7% at the end of January. Gaming it out, more substantial cuts resulting from company guidance in the soon-to-be U.S. June quarter earnings season are a potential headwind for the market. That suggests it could be time to revisit our Market Hedge model.

More By This Author:

TSM May Revenue Soars, Multiple Models Leading The Market QTDLayoffs Heat Back Up, May PMI Data Points To Inflation Doing The Same

Enjoy The Court’s Tariff Ruling, Brace For Trump’s Response

Comments

Log in or sign up to join the conversation.