Top 4 Dividend Stocks To Hold Now

In my latest article, I’ve highlighted 4 popular dividend stocks to sell. As I wrote at the end of this article, I don’t appreciate when people criticize without bringing something on the table. For this reason, I’m offering you 4 interesting stock picks for 2017 that could easily replace the other bad seeds.

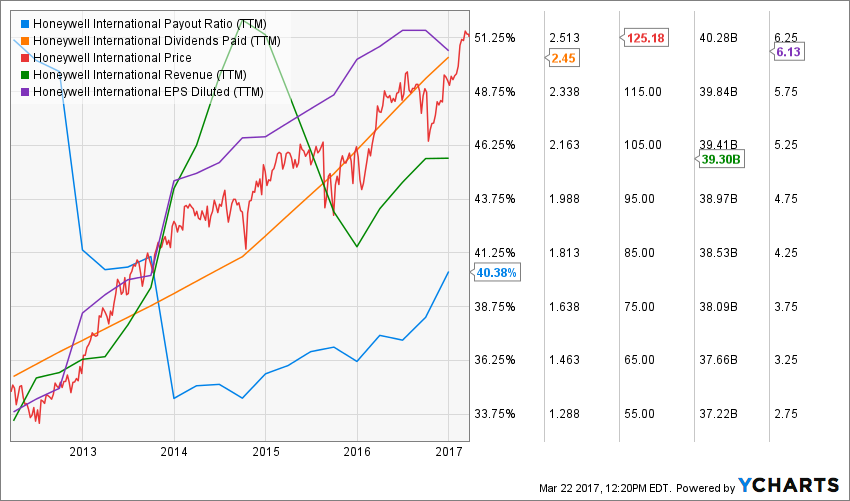

Honeywell International (HON)

Business model:

Honeywell invents and manufactures technologies to address some of the world’s toughest challenges initiated by revolutionary macrotrends in science, technology and society. The company evolves in three different industries: Aerospace & Transportation, Automation & Control system, Materials & Chemicals. The company recently combined the aerospace and the transportation segment in order to improve scaling economy.

Main strengths:

The company has put additional focus on software engineering with nearly 11,000 engineers working on software instead of more classic industrial goods. The software business is better as it enables more combinations of services and drives higher margins. Honeywell certainly has some solid ground for future growth.

Potential risks:

While margins improvements were quite phenomenal, we can’t expect to see the company keeps increasing its margins. Therefore, further numbers shouldn’t be that impressive. Also, HON automation segment may suffer from the oil and gas industry slump.

Dividend growth perspective:

management had announced last year that the dividend payout ratio will increase in the upcoming 4 years. In 2015, the dividend payment increase was of 15% and 11.76% in 2016. I’m not putting on my pink colored glasses and expecting a 12% dividend growth for the next 10 years, but I can appreciate the growth will be significant for several years to come.

Investment thesis:

Honeywell has made impressive efforts to improve their internal practices over the past 15 years after failing to merge with General Electrics (GE). Those efforts paid well as the company operating margins improved from 7.6% in 2004 to 15.2% in 2014. Those impressive margin increase lead HON EPS to increase by 10% in 2015 as the company is facing a challenging economy. The company was also able to increase its dividend by 10% CAGR over the past 5 years. HON is a leader in the aerospace control and safety systems and should benefit from its leadership position during the commercial aircraft upcycle.

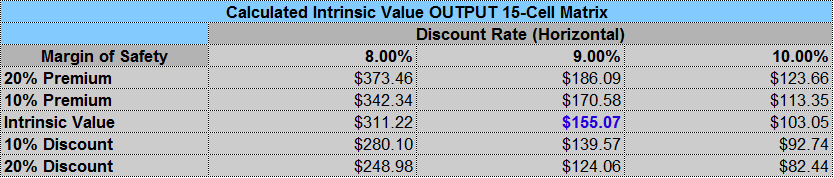

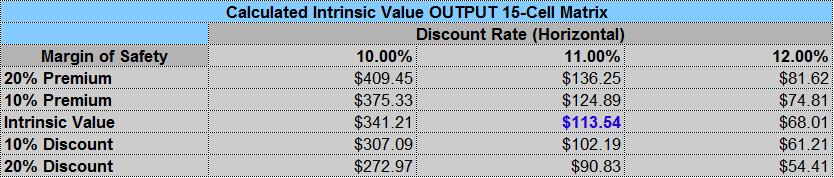

Valuation:

Source: Dividend Monk Toolkit Excel Calculation Spreadsheet

Lowe’s (LOW)

Business model:

Lowe’s is the second-largest home-improvement retailer in the world with over $59 billion in annual revenues. Strong from its position in the U.S., Lowe’s benefits from the recent rebound of the world’s largest economy. LOW is also expanding through acquisitions as management recently closed the purchase of Rona in Canada. Lowe’s doesn’t only focus on selling you home renovation and improvement products, it also uses their experienced salesforce to provide you with additional advice. The company has also successfully built a solution-based segment within its stores. By offering a complete solution from start to finish, Lowe’s make sure to “capture” the customer for its entire project purchases.

Main strengths:

Mainly due to its size and high tech product management platform, Lowe’s is able to generate substantial economies scale. The firm has created an integrated supply chain that efficiently routes nearly 75% of all Lowe’s merchandise through one of 15 regional distribution centers. Its omnipresence in North America enables Lowe’s to benefit from strong construction business in Canada and the United States. This alone should be enough to bring consistent growth for years to come.

Potential risks:

As we see it, the biggest risk for LOW is definitely another economic slowdown. There are still several uncertainties in the air and a contraction of the US economy would definitely put a halt to LOW’s strong growth perspectives. The company margin will be under pressure in the upcoming years as competition with Home Depot intensifies and Rona’s lower margins are included in Lowe’s numbers.

Dividend growth perspective:

LOW shows a very strong business model generating a consistent cash flow stream. While the company will benefit from additional cash flow during a strong economic cycle, its distribution network efficiency will continue to provide management additional room for dividend increases in the future. The secret of LOW’s long dividend increase history is found in a very low payout ratio (35%) and a very low yield too (less than 1.50%). Management’s conservative approach makes the company’s dividend growth sustainable for several years to come.

Investment thesis:

Focus on a recovering U.S. economy and additional growth from acquisitions should continue to push LOW’s stock price higher. Its strong brand and the way it helps its customers to go through bigger projects by offering a “one-stop-shop-&-advice” service will secure LOW’s market share and improve margins over the long haul. Lowe’s has been able to transform a simple home product store into a great service offering for home projects. There is definitely more room for growth in the upcoming years.

Valuation:

Source: Dividend Monk Toolkit Excel Calculation Spreadsheet

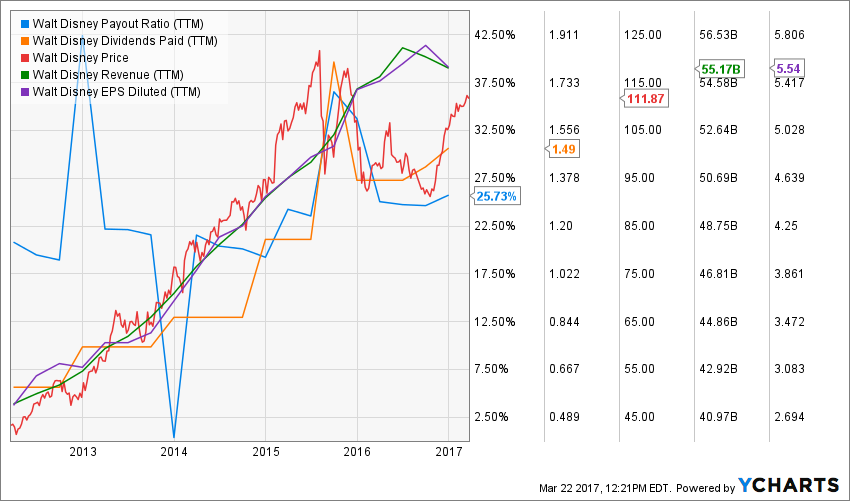

Disney (DIS)

Business model:

DIS has become more than entertainment parks and Mickey. It is now the largest entertainment business in the world. Walt Disney is divided into five different segments: Media Networks, Parks and Resorts, Studio Entertainments, Consumer Products and Interactive. The Media division (ABC, The Disney Channel and ESPN) leads DIS revenue shares with 44% of the company total sales.

Main strengths:

Disney has built one of the most respectable brand in the world. Its attention to details makes their theme parks and movies almost perfect each time. They also show a strong synergy between all their divisions. Therefore, whenever Disney makes a good move, it is able to duplicate its returns through derivative products across its other divisions. The recent Start Wars success is a great example of how a blockbuster movie engaged more enthusiasm for theme parks and figurines.

Potential risks:

Over the past 18th months, many financial analysts have spit in the soup. The main reason being the inevitable death of the cable industry. This will not happen in 2017, but analysts are concerned about the highly profitable ESPN network slowly losing their customers for streaming options. This could hurt the stock price over a short period of time again in 2017, but we remain strongly bullish for DIS over the long haul.

Dividend growth perspective:

Disney is not known for its dividend payments. It is usually paying a shy 1% yield even with a strong dividend growth policy. The good news is that the yield is now closer to 1.50% as the stock price stagnated while the dividend continued to grow. 5 years ago, DIS dividend payment was at $0.60 per share for the year and it will be paying $1.49 in 2016. The payout ratio is still very low at 24.63%. This shows you how strong the dividend growth potential is.

Investment thesis:

DIS has become more than entertainment parks and Mickey. It is now the largest entertainment business in the world. Walt Disney is divided into five different segments: Media Networks, Parks and Resorts, Studio Entertainments, Consumer Products and Interactive. The Media division (ABC, The Disney Channel and ESPN) leads DIS revenue shares with 44% of the company total sales.

Disney divisions will benefit from the US consumers spending more, especially with the coming of the new Star Wars trilogy. Finally, Disney is the strongest brand for family entertainment and this competitive advantage is nearly impossible to replicate.

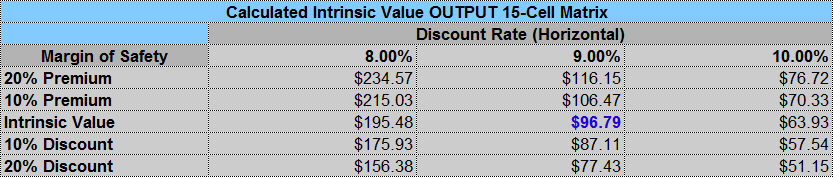

Valuation:

Source: Dividend Monk Toolkit Excel Calculation Spreadsheet

BlackRock (BLK)

Business model:

BlackRock is the world largest asset manager, period. The company offers a variety of products for all asset classes (from fixed income to equity and alternative investments). Over the past decade, BLK grew a lot faster due to the popularity of its ETFs product line; iShares (there is something with this “i” thing, huh?).

Main strengths:

BlackRock benefits from a core business model where 61% of AUM is coming from institutional clients. Due to shifting costs and BLK solid reputation, this is a very sticky business. BLK also benefits from Govt regulation modifications pushing brokers and advisors to use more cost-efficient investing products. Since BLK is the largest ETF manufacturer, it will automatically drive its sales up.

Potential risks:

Investing firms are always one crash away from a bad year. In the event of a bubble burst as we had in 2008, BLK shares will definitely plummet. However, I see this outcome as very unlikely at the moment. The economy is growing, employment in the U.S. is strong and the stock market continues to move forward.

Dividend growth perspective:

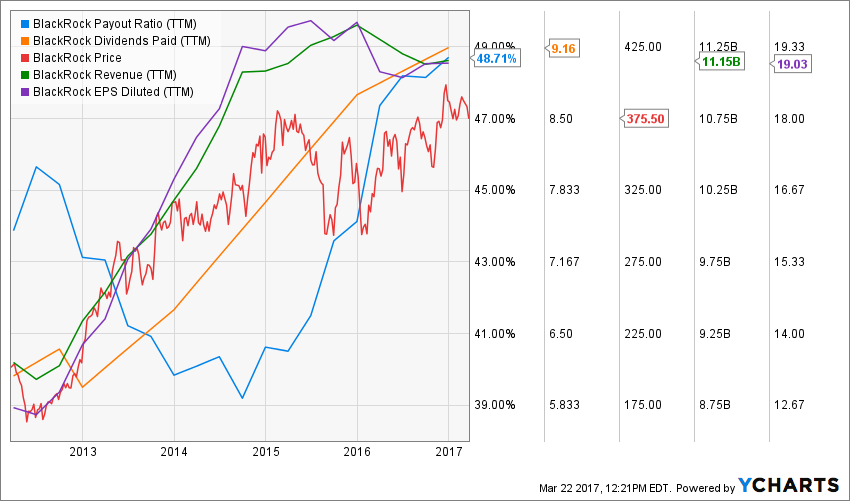

BLK has increased its dividend payment for 7 consecutive years now. With a payout ratio around 50%, management has lots of room to continue its dividend growth policy for several years to come. Since BLK benefits from a strong growth vector through its ETFs products, you can expect this company to show on many dividend investor radars in the years to come.

Investment thesis:

BlackRock is a leader in its industry and has built a solid relationship with its clients. They operate a sticky business with institutional client and they are a leader in a growing investing trend. As BLK offers a wide variety of products, it will manage making money regardless if investors are bullish or bearish.

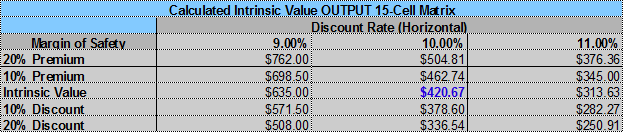

Valuation:

Source: Dividend Monk Toolkit Excel Calculation Spreadsheet

How I selected those 4 companies

Before I select any companies to be part of my portfolio, I go through an exhaustive investment process. Each company must meet the 7 dividend investing principles. Those principles have been established based on several academic studies and over a decade of my financial experience in the stock market. I not only think those stocks will do well in 2017, but I believe they will do well in the long run too. In my opinion, those are keepers for a dividend growth portfolio.

Disclosure: Each month, we do a review of a specific industry at our membership website; Dividend Stocks Rock. In addition to have full access ...

more