|

Pre-Market Price Check |

|

| S&P 500 Futures: +0.83% | 10-Year Yield: 3.989 (+4 bps) |

| Nasdaq 100 Futures: +1.28% | WTI Crude: $61.63(+0.24%) |

| Dow Jones Futures: +0.51% | Gold Futures: $4,054 (-2.04%) |

| VIX: 18.23 (-12.27%) | Bitcoin (BTC): $115,128 (+1.34%) |

What’s Driving Stocks This Morning

A framework deal between the U.S. and China is lifting global sentiment this morning, with reports confirming that the two sides have agreed to delay the imposition of 100% tariffs, keeping the current 30% rate in place.

President Trump and President Xi are scheduled to meet Thursday to finalize the arrangement.

Treasury Secretary Scott Bessent added momentum by saying the deal will likely include major soybean purchases, a resolution on TikTok, and a delay in rare earth export controls.

The chip sector breathed a sigh of relief as Bessent also confirmed that current U.S. export restrictions on semiconductors will remain unchanged.

Optimism is also growing around the Fed, with traders expecting a rate cut at this week’s FOMC meeting.

Recent inflation softness and Fed rhetoric support that view, and the bond market is responding accordingly.

Meanwhile, mega-cap stocks are powering higher, with Microsoft rallying after Guggenheim slapped a $586 target on the stock.

M&A activity is back in focus, with Novartis announcing a $72 per share buyout of Avidity Biosciences and Huntington Bancshares acquiring Cadence Bank in a $7.4 billion all-stock deal.

Elsewhere, headlines are stacking up. Trump is reportedly eyeing military action targeting cocaine production in Venezuela and has increased tariffs on Canadian goods following a Reagan-themed campaign ad. He also warned of Russian submarine activity and suggested he’s open to lowering tariffs on Brazil under the right terms.

SoftBank made a splash with a $22.5 billion investment in OpenAI. And today’s Treasury auctions - $69B in 2-year notes and $70B in 5-year notes - could provide key signals on bond demand.

What to Watch Today

- FOMC meeting expectations and rate cut speculation

- Trump–Xi trade meeting preparation and rare earth fallout

- Treasury auctions for 2-year and 5-year notes

- Price action from Novartis/RNA and HBAN/CADE M&A activity

- AI infrastructure sentiment following SoftBank’s OpenAI deal

- Microsoft follow-through after major price target upgrade

- Bond market response to easing inflation and trade de-escalation

Stocks on the Move (Pre-Market)

Avidity Biosciences (RNA) is up 37.5% after Novartis announced a $72/share all-cash buyout, a major biotech headline amid a quiet M&A cycle.

Cadence Bank (CADE) jumps 24.1% after confirming it will be acquired by Huntington Bancshares (HBAN) for $7.4 billion in stock, sparking renewed regional bank interest.

Microsoft (MSFT) gains 2.3% pre-market after Guggenheim upgraded the stock to Buy and raised its target to $586, citing ongoing leadership in AI and cloud.

Snowflake (SNOW) is up 3.7% after reaffirming its Q3 and full-year FY26 revenue guidance, offering stability in a volatile software environment.

Upgrades

Microsoft (MSFT) upgraded to Buy from Neutral at Guggenheim with a $586 target, citing cloud dominance and AI upside.

Honeywell (HON) upgraded to Outperform at RBC, target $253, driven by strength in industrial automation and aerospace.

General Dynamics (GD) upgraded to Buy at Vertical Research with a $400 target amid rising defense demand.

Five Below (FIVE) upgraded to Overweight at JPMorgan, target $186, as value retail continues to outperform.

Downgrades

Berkshire Hathaway (BRK-A) downgraded to Underperform at Keefe Bruyette, target $700,000, due to valuation concerns.

Harley-Davidson (HOG) downgraded to Underweight at Morgan Stanley, target $25, as demand and macro headwinds weigh on margins.

Roper Technologies (ROP) downgraded to Sector Perform at RBC, target $539, on slowing organic growth expectations.

Wolverine Worldwide (WWW) downgraded to Hold at Williams Trading, target $27, as sales trends remain under pressure.

(Click on image to enlarge)

Today’s Bottom Line

This morning’s rally is built on tangible progress.

The U.S.–China trade truce removes a major overhang at a time when inflation is easing and the Fed looks increasingly dovish. The combination of mega-cap upgrades, AI investment momentum, and M&A tailwinds has created the most bullish setup in weeks.

If Thursday’s Trump–Xi meeting goes smoothly and the Fed follows through on a rate cut, the path clears for a potential year-end breakout, assuming earnings hold up.

Watch the bond auctions and chip names for confirmation.

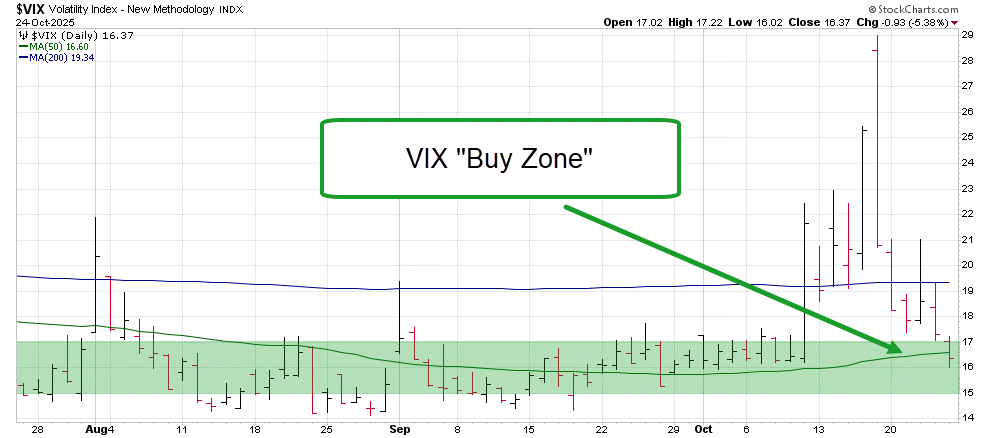

Watch that VIX in its “Buy Zone” as well. This “indicator” is batting 1.000 in 2025 as short-term shorts of fear unwinding have provided strong rallies for the markets.

Beat the market, without relying on brokers or biased institutions.

More By This Author:

Palantir Stock Pops On Positive Inflation Report: Here’s What To KnowChipmaker Nvidia Gets A Boost Following Positive CPI Report

Gold’s Rare Signal Is A Gift To Investors

Comments

Log in or sign up to join the conversation.