Over the past year, a stealth bear market formed that up until recently mostly affected high-growth stocks. You wouldn’t have known this was the case last year as the major averages held up fairly well.

The indexes weren’t telling the real story though, as many individual stocks plummeted substantially from their peaks. The S&P 500 is a good example – the top 10 stocks account for nearly 30% of the index’s total market capitalization. The major indexes are not the market, and the market is not the major indexes.

We can see how this played out in the images below as last year the percentage of stocks above their 200-day moving average steadily declined, while the S&P 500 steadily rose in value. A stealth bear market took shape as a high percentage of individual companies had fallen 20% or more from their respective highs.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Many stocks are now down 50-80% from their peaks, and most are still falling. The major indexes have finally started to roll over as even the top-weighted companies are not immune to this downside move. What was once stealth has now come to the forefront.

To give readers a sense of where things currently stand, as of yesterday just 45% of stocks within the S&P 500 were trading above their respective 200-day moving averages. It’s even worse for the Nasdaq, as just 36% were trading above the heavily watched level. While these are historically low percentages, things can certainly get worse. During the March 2020 COVID-related plunge, these numbers dropped to the low single digits.

The situation has evolved and we now have to determine if we have put in a low for the move (recorded in late January) or if it’s going to get worse. The back-and-forth political tension with Russia and Ukraine certainly isn’t helping the bull case.

If Russia invades Ukraine, the markets will likely respond negatively which could fuel another leg down for the major indexes. However, I could see this leading to panic selling and a short-term, fear-driven low in late February. March and April tend to be bullish from a historical and seasonal perspective.

We want to target pockets of the market that are showing relative strength and weathering the volatility. The one area that is showing these characteristics without question this year is energy. With recent inflation readings coming in well above expectations and surging prices seemingly out of the Fed’s control, energy is well-positioned to withstand any further market pullback in the short-term.

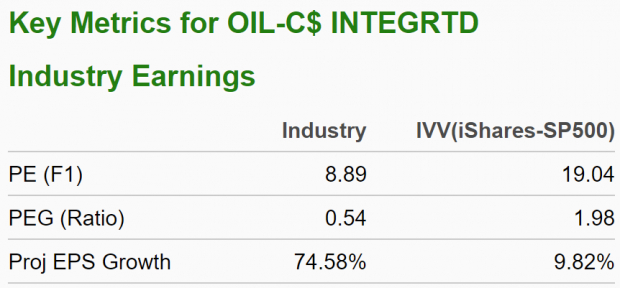

The various Zacks Ranking systems are confirming the notion that energy is the place to be. We’re going to focus on the Zacks Oil & Gas – Integrated – Canadian industry group, which currently ranks in the top 2% of all Zacks Ranked Industries. It is showing some favorable characteristics as illustrated below:

Image Source: Zacks Investment Research

The stocks contained within this industry group are witnessing extremely positive earnings estimate revisions. The industry group is part of the Zacks Oils & Energy sector, which ranks #3 out of all 16 Zacks Ranked Sectors.

Next, we’ll examine two Zacks Rank #1 (Strong Buy) stocks contained within this favorable industry and sector combination.

Cenovus Energy, Inc. (CVE)

Cenovus Energy is a Canadian integrated oil company. CVE develops, produces, and markets crude oil and natural gas in Canada, the United States, and Asia. The company has 50% ownership in two U.S. crude refineries which produce diesel, gasoline, jet fuel, asphalt, and related products. Cenovus Energy was founded in 2009 and is headquartered in Calgary.

At the end of last year, CVE had oil-equivalent proved reserves of 6.1 billion barrels, a 21% increase versus 2020. Cenovus expects to see annual production growth between 2-3% for the next several years. The Canadian oil company has a strong focus on returning capital to shareholders and anticipates allocating roughly 50% of excess free funds to shareholders this year. CVE plans to buy back up to 146.5 million shares in 2022.

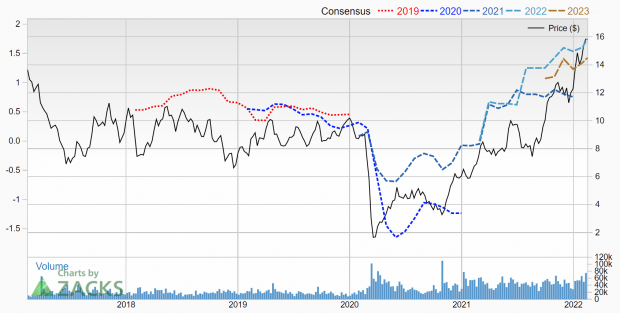

CVE’s Q4 earnings surpassed expectations when the company announced results last week. Cenovus delivered EPS of $0.43, a +4.88% surprise over the $0.41 consensus. CVE shares have advanced over 132% during the past year. Despite the impressive run, the company is still relatively undervalued at an 8.89 forward P/E.

Image Source: Zacks Investment Research

Analysts covering CVE are in agreement in terms of recent earnings estimate revisions. The first two quarters of this year look extremely positive for the bulls, as estimates have been revised upward by 23.08% and 9.3% respectively in the past 60 days. The Zacks Consensus Estimates for each quarter and their corresponding year-over-year growth rates are $0.48 (+500%) and $0.47 (+422.22%), respectively.

The situation appears similar when zooming out and viewing the entire year. The 2022 EPS estimate has been increased by +13.64% over the past two months. The Zacks Consensus Estimate now stands at $1.75, translating to a potential 116.05% growth rate relative to last year.

Imperial Oil Limited (IMO)

Imperial Oil is Canada’s largest integrated petroleum company. IMO explores for, produces, and sells crude oil and natural gas in Canada. Imperial is a subsidiary of Exxon Mobil Corporation. Its operations also include the refining and marketing of petroleum products in addition to the manufacture and sale of petrochemicals. IMO was incorporated in 1880 and is also based out of Calgary.

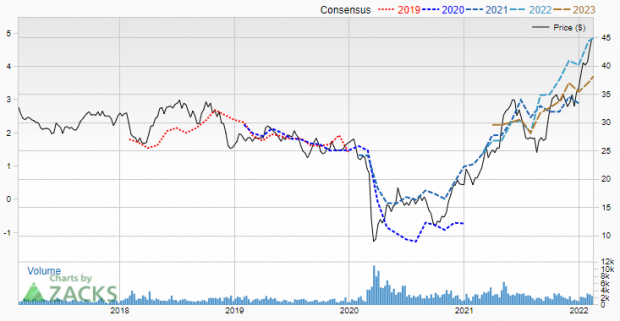

Similar to CVE, Imperial Oil has witnessed positive earnings estimate revisions as of late. Within the past month, expectations for Q1 and Q2 EPS have risen +14.41% and +5.93%, respectively. The Zacks Consensus Estimates and corresponding growth rates for the first two quarters of this year are now $1.27 (+202.38%) and $1.25 (+204.88%), respectively. Analysts are anticipating full-year EPS to rise 74.46% to $4.85.

Canada’s largest jet fuel supplier has posted an average earnings surprise of +0.25% over the past four quarters, helping push the stock nearly 118% higher over the past year. Even with the remarkable performance, IMO still trades at an attractive 9.03 forward P/E.

Image Source: Zacks Investment Research

Both IMO and CVE sport our top Zacks Growth Style Score of ‘A’, as well as our top overall VGM score. As the price of oil continues its ascent, these energy companies are in a good position to resume their outperformance.

Comments

Log in or sign up to join the conversation.