Image Source: Unsplash

Adobe (ADBE) is a global software company best known for creative tools like Photoshop, Illustrator, Premiere Pro, and Acrobat. But it’s not just a design company anymore.

Adobe is expanding deep into enterprise software with AI-driven tools for marketing automation, customer journey orchestration, and content management. Its products are used by everyone from solo freelancers to Fortune 500 brands. While the stock has been falling lately, there’s more going on under the surface.

The IDDA Analysis framework is used to analyze companies and determine which are right for you. There are five steps to the process:

- Capital Analysis – Your personal risk tolerance.

- Intentional Analysis – Your unique financial goals and timelines based on your age, health, and lifestyle.

- Fundamental Analysis – The viability of the asset based on company performance, financial health, and market position.

- Sentimental Analysis – The current emotions of Wall Street and other market participants.

- Technical Analysis – Historical price action to identify key psychological levels and market patterns.

Let’s dive into the IDDA analysis to assess Adobe’s fundamental, sentimental, and technical outlook.

IDDA Point 1&2: Capital & Intentional

The capital and intentional analysis need to be conducted by you.

Select your assets in alignment with your financial goals. Listen to your intuition about each asset, but remember to invest based on your own values, not just because of recommendations from others.

IDDA Point 3: Fundamental

Profit Margins Stay Strong

Adobe is still one of the most profitable software companies in the world. Its gross margin is close to 89%, and net profit margin sits around 30%. It also has a high return on equity (over 50%) and generates nearly $9.5 billion in free cash flow annually. These numbers show Adobe still runs a very efficient and healthy business.

Dominant Position in Creative Software

Adobe continues to dominate the creative market with products like Photoshop, Illustrator, and Premiere. In 2024, Creative Cloud alone brought in over $12 billion, making up the bulk of Adobe’s $15.8 billion Digital Media segment. This segment still accounts for about 74% of total revenue.

AI Integration Across Platforms

Adobe is expanding AI tools like Firefly into all major apps. It also launched GenStudio and Agent Orchestrator for enterprise clients. These tools help companies automate content creation and customer interactions. The integration of generative AI keeps Adobe competitive as the industry shifts.

Revenue Growth Slowing Down

While Adobe is still growing, the pace is slowing. Revenue grew about 10.6% year over year, down from 14% over the past five years. EPS growth is also decelerating. Investors are used to higher growth from Adobe, so this cooldown is raising some concerns.

Short-Term Liquidity Pressure

Adobe’s current ratio is just under 1. This means its short-term assets barely cover short-term liabilities. While it’s not a red flag for a cash-rich company like Adobe, it’s still something to watch—especially if unexpected costs arise.

Enterprise Expansion in Digital Experience

Adobe’s Digital Experience segment brought in $5.37 billion in 2024, making up 25% of total revenue. New tools like Brand Concierge and Agent Orchestrator target big companies and expand Adobe’s role in marketing, automation, and customer experience. These could become major revenue drivers in the next few years.

Failed Figma Acquisition Shows Limits

Adobe’s $20 billion Figma acquisition was blocked by regulators. That deal was supposed to help Adobe stay ahead in design collaboration. Now, Adobe has to compete with Figma head-to-head, which could slow growth in that product category.

Strong Free Cash Flow and Debt Control

Adobe has about $5.7 billion in cash and only $6.5 billion in debt. Its debt-to-free cash flow ratio is just 0.65, meaning it could pay off all debt in under a year if needed. This gives Adobe flexibility even if revenue growth softens.

Fundamental Risk: Low to Medium

Adobe has strong financials and high profitability, but slower growth, rising competition, and tighter liquidity bump up the risk slightly. Still, the fundamentals remain solid for long-term investors.

IDDA Point 4: Sentimental

Overall sentiment is bearish for Adobe as of August 2025.

Strengths

Strong partnerships with NVIDIA, AWS, Microsoft, and Amazon continue to position Adobe as a key player in the AI and enterprise automation space. These collaborations boost credibility and long-term potential.

Adobe is a leader in ethical AI development. Its commitment to transparency and responsible use through the Content Authenticity Initiative reduces regulatory risk and builds public trust.

Institutional investors still hold large positions in Adobe. While price targets have been adjusted, many long-term funds continue to believe in Adobe’s competitive moat.

Adobe’s enterprise-facing AI products, like Agent Orchestrator and GenStudio, are gaining traction with big brands. That adds confidence about future adoption and monetization.

Risks

Investors are frustrated that Adobe’s AI tools have not translated into meaningful short-term revenue growth. The hype around Firefly and GenStudio has not yet delivered financial results.

Adobe has now posted four consecutive earnings drops after announcements. Even when the company beats expectations, the stock sells off. That signals weak investor confidence and fatigue.

Some analysts have downgraded Adobe to sell, citing intense competition from smaller AI-first companies like Midjourney, Runway, and Canva. These tools are seen as easier to use and more affordable.

The blocked Figma deal highlighted antitrust concerns and forced Adobe to grow organically. That limits aggressive expansion plans and has made Wall Street cautious.

Broader market rotation into faster-growing AI names like NVIDIA and Palantir has left Adobe out of the spotlight. Investors chasing high-momentum stocks are overlooking Adobe’s long-term setup.

Sentimental Risk: Medium to High

The sentiment around Adobe is weak right now. Many investors feel let down by the lack of immediate AI payoff and are worried about rising competition. Long-term believers are staying put, but short-term traders are nervous or selling. This creates emotional pressure on the stock, even if fundamentals stay strong.

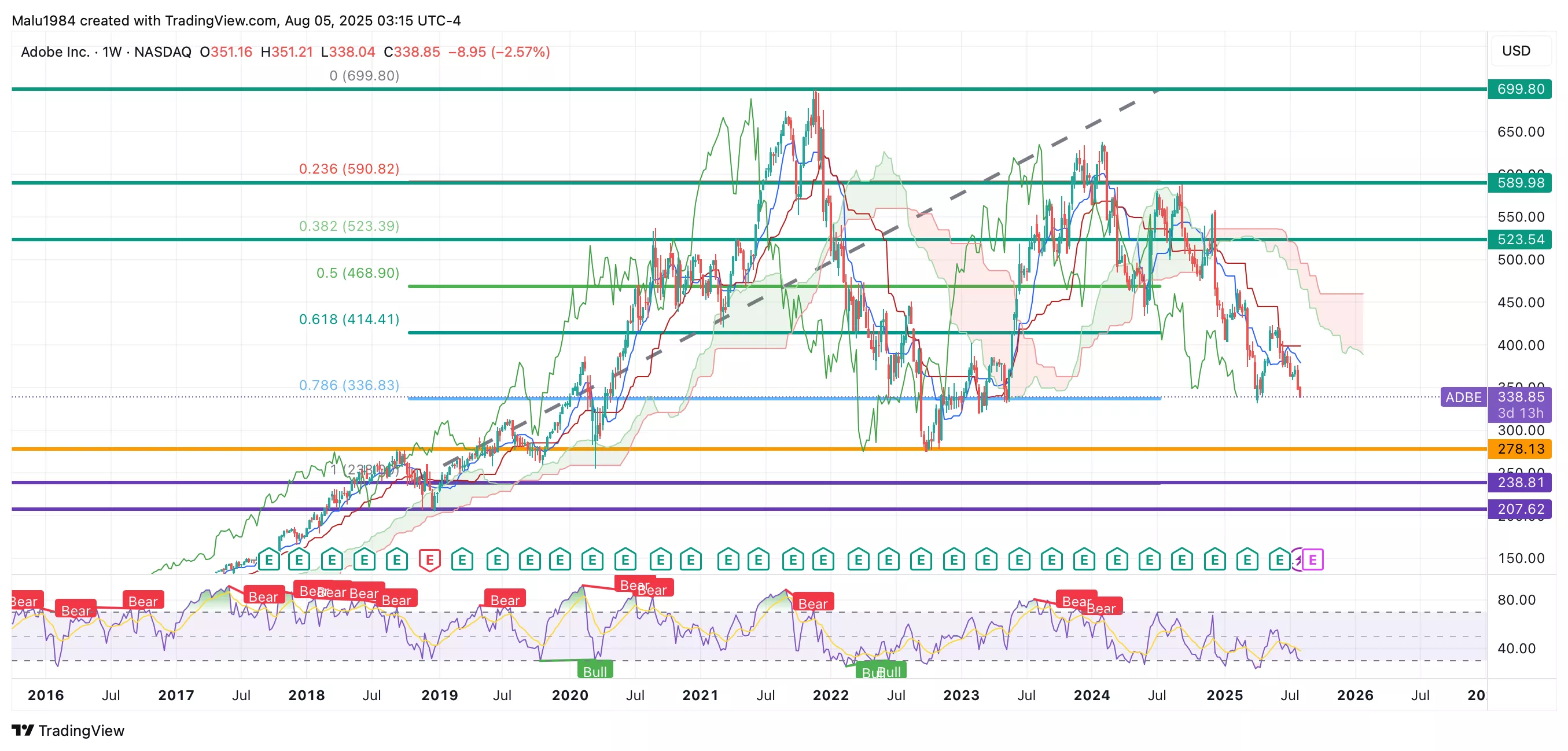

IDDA POINT 5 – TECHNICAL

Weekly Chart

Price is trading below the Ichimoku Cloud, which signals a bearish trend.

The conversion line (Tenkan-sen) is below the baseline (Kijun-sen), another bearish confirmation.

There is no sign of a bullish crossover yet, and the cloud ahead is thick and red, suggesting continued downside pressure.

The RSI is at 30, which puts the stock on the edge of oversold territory. That means price could bounce—but it could also stay low for a while if selling pressure continues.

No strong reversal pattern has formed yet. The stock has been in a steady downtrend since January 2024 with lower highs and lower lows.

Overall, the technical outlook is bearish. The chart shows clear weakness with strong downward momentum and aligned bearish signals. But with RSI touching oversold levels, some short-term bounce or consolidation could happen—especially if sentiment shifts or positive news emerges. This stock may offer opportunity for long-term investors or swing traders watching for signs of reversal.

(Click on image to enlarge)

Buy Limit (BL) levels:

$278.13 – High Risk

$238.81 – Moderate Risk

$207.62 – Low Risk

Profit taking (PT) levels:

$523.54 – High Risk

$589.98 – Moderate Risk

$699.80 – Low Risk

Here are the Invest Diva ‘Confidence Compass’ questions to ask yourself before buying at each level:

- If I buy at this price and the price drops by another 50%, how would I feel? Would I panic, or would I buy more to dollar-cost average at lower prices? (hint: this question also reveals your CONFIDENCE in the asset you’re planning to invest in).

- If I don’t buy at this price and the stock suddenly turns around and starts going up again, will I beat myself up for not having bought at this level?

Remember: Investing is personal, and what is right for me might not be right for you. Always do your own due diligence. You should ONLY invest based on your own risk tolerance and your timeframe for reaching your portfolio goals

Technical Risk: Medium to High

The price is trading below the cloud with bearish signals from both Ichimoku and RSI. While oversold conditions could lead to a bounce, there’s no clear support or reversal pattern yet. The downtrend remains intact, making the short-term outlook risky for new entries.

Summary: Final Thoughts

Adobe’s fundamentals are still rock solid. It’s highly profitable, generates strong cash flow, and leads the creative software space. Its push into enterprise AI—with tools like GenStudio, Firefly, and Agent Orchestrator—shows long-term vision. Partnerships with NVIDIA, AWS, and Microsoft add weight to that vision.

But short-term growth is slowing. Revenue and earnings are still growing, just not at the pace investors got used to. The blocked Figma deal hurt momentum, and Adobe now has to compete directly with rising AI-first challengers. Its liquidity ratios have also weakened slightly.

Sentiment is mixed. On one hand, the stock has dropped for months, and short-term investors seem frustrated by the lack of fast AI payoffs. On the other hand, most analysts on Seeking Alpha remain bullish, pointing to Adobe’s strong fundamentals and long-term strategy. So while the mood in the market feels bearish, not everyone has lost faith.

Technically, the chart looks weak. Price is below the Ichimoku Cloud, RSI is sitting near oversold, and no bullish reversal has appeared. That adds short-term risk for traders and momentum investors.

Overall Opinion: Cautiously Bullish

The business is solid, but Wall Street’s patience is thin. For long-term investors, this may be the moment others are missing—especially if Adobe starts turning AI buzz into real numbers.

Overall Risk: Medium to High

The company isn’t the problem. The market mood is. With fundamentals intact but emotion and price action dragging, risk is elevated—but opportunity may be hiding in plain sight.

More By This Author:

3 Clues Applied Digital Stock Might Be The Sleeper Giant No One’s WatchingMicrosoft Stock Is Surging After Earnings But If You Miss This AI Signal, You Might Miss The Bigger Opportunity

Wall Street Is Focused On Meta Stock Numbers But This Quiet AI Move Could Unlock Bigger Gains

Comments

Log in or sign up to join the conversation.