The Best Lithium Stocks: Industry Investment Analysis From Mining To Batteries

Lithium, also dubbed “white petroleum,” is one the flashier metals that you will come across. While it is white or gray in typical form, when it is thrown into a fire it turns bright red. Lithium mineral was documented in the 1790’s, but it wasn’t until 1855 that the element was separated and identified.

Lithium (atomic symbol Li) has many unique characteristics. It’s light and soft – soft enough to be cut with a butter knife and light enough to float on water. Further, the metal has a relatively low melting point but a high boiling point. Its uses vary dramatically, from the manufacture of aircraft and batteries to mental health medicine.

In 1991 Sony popularized the lithium-ion battery and now it has become a vital part of nearly every electronic device. Naturally, the use of electronics has taken off with mobile phones leading the way in the last decade. However, electric vehicles are becoming the true drivers of demand, as an electric car requires 5,000 to 10,000 times as much lithium as a mobile phone.

This has caused an interest in investing in the Lithium industry to surge.

This guide gives an overview of the Lithium Industry as well as detailed analysis on lithium stocks and lithium investing.

Lithium Industry Overview

In 2009 the lithium-ion battery made up roughly 21% of all lithium consumption. Last year about 46% of lithium produced went to batteries – more than doubling its share (in a growing market) in less than a decade. Other important uses include ceramics and glass (27% of the market) and lubricating greases (7%).

Extracting Lithium

There are two main ways of extracting lithium: mining and brine water. Interestingly, about 87% of lithium is extracted via brine water from briny lakes known as salars. The highest concentrations of these lakes are found in Chile and Argentina. Lithium is obtained via evaporation in the form of lithium carbonate, the raw material used in lithium-ion batteries. This process also leaves behind magnesium, calcium, sodium and potassium.

While brine mining is a lengthy endeavor – normally taking 8 months to 3 years – it is still usually easier and cheaper than hard rock mining.

The remaining 13% of lithium is found in traditional mining operations. The concentration of lithium is greater in hard rock mines, but the cost to operate these mines and the environmental and geological impact is much greater. Still, a hard rock mine in operation can be competitive with an upstart brine mine.

While there are 145 minerals containing lithium, just five are used in lithium extraction. Moreover, of these five, spodumene makes up the lion’s share (~90%) of mineral-derived lithium. The mineral is heated, cooled and mixed with sulfuric acid to create lithium carbonate.

Finally, there is a very small amount of lithium that is being recycled from electronics. This method does not provide pure enough lithium to make new batteries, but it is suitable for other uses such as glass and ceramics.

Supply

Total lithium production in 2017 amounted to 43,000 MT (metric tons).

Here are the top lithium producing countries in 2017:

- Australia = 18,700 MT (43.5% of worldwide production)

- Chile = 14,100 MT (32.8%)

- Argentina = 5,500 MT (12.8%)

- China = 3,000 MT (7.0%)

- Zimbabwe = 1,000 MT (2.3%)

As you can see the production of lithium is highly concentrated, with 98.4% of it being produced by just five countries. Indeed, Australia and Chile alone accounted for three-fourths of the production market last year.

Total worldwide lithium reserves are estimated to be 16 million tons (372 times last year’s production). Here are the top lithium reserve countries:

- Chile = 7,500,000 MT (46.9% of worldwide reserves)

- China = 3,200,000 MT (20.0%)

- Australia = 2,700,000 MT (16.9%)

- Argentina = 2,000,000 MT (12.5%)

Here too the lithium reserves are quite concentrated in just a handful of countries. While some reserves exist in other countries throughout the world (60,000 MT in Portugal, 48,000 MT in Brazil, 35,000 MT in the U.S. and 23,000 MT in Zimbabwe for instance) these are not “long-term pools” of resources available to be extracted.

Long-term mining activity will continue to be driven by Chile, China, Australia and Argentina.

Demand

The demand for lithium currently has three main drivers:

- Continued mobile device adoption

- Energy storage for electric grids / renewable energy

- Electric vehicles

As noted above, short and intermediate-term demand for lithium will likely depend on the dynamics of the electric vehicle market. Mobil device adoption will continue to be a driver, but electric vehicles require thousands of times as much lithium and hence have a much larger influence. Batteries for storage for renewable energy could be an important driver down the line, but that is viewed as more of a long-term demand driver.

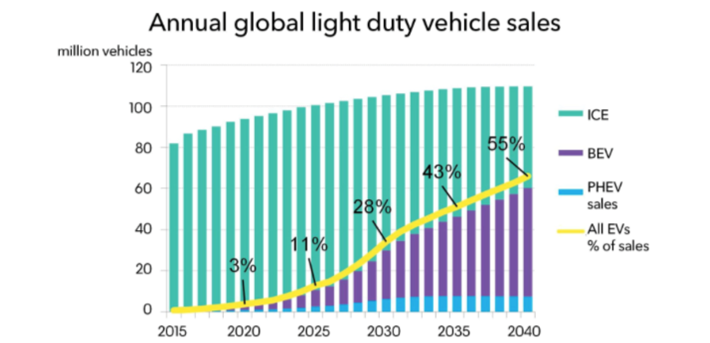

Bloomberg anticipates electric vehicle sales, which came in at 1.1 million last year, to rise to 11 million by 2025 and to 30 million by 2030, as electric battery costs become cheaper than internal combustion engines. Moreover, the expectation is that China will lead the charge (literally) with electric vehicles making up 33% of the global fleet and 55% of all new car sales by 2040.

Source: Bloomberg New Energy Finance

Additionally, while demand forecasts vary widely, it is largely expected that electric vehicle production will test supply in the years and decades to come. Indeed, some believe that electric vehicle adoption will be stymied by the availability (or lack thereof) of key components like lithium, as the recent ramp up in demand moves much faster the ability to establish new mines, which often take years.

However, despite tremendous expectations, it should be noted that while lithium is an essential part to electric vehicles, it is not necessarily a fundamental cost driver. To give you an example, Tesla’s Model S’ entire battery pack weighs about 1,200 pounds, but the amount of lithium equivalent used is only about 15 pounds.

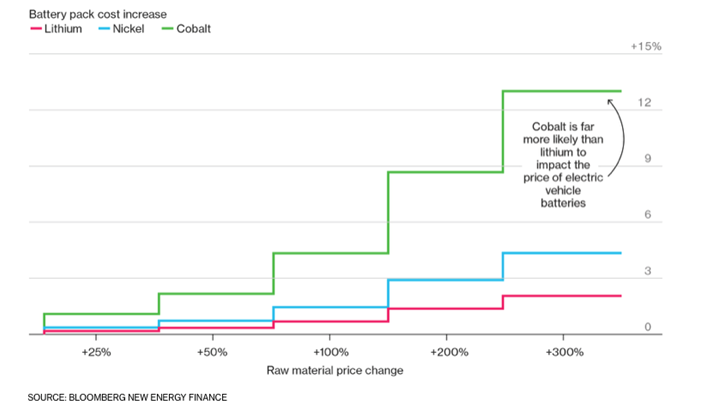

Source: Bloomberg New Energy Finance

More important cost drivers could include Nickel and Cobalt, making up 73% and 14% of a typical battery, as compared to 11% for lithium. Tesla’s Elon Musk calls lithium “the salt on the salad,” noting the relatively low expense of the material as compared to the overall cost of the vehicle.

While there are ample reserves of lithium available, the demand has picked up tremendously leading to supply-side constraints. Pricing can be volatile.

Source: Global X Funds, Bloomberg

Investing In Lithium

There is a way to directly (if not broadly) invest in the industry: The Global X Lithium & Battery Tech ETF (ticker: LIT).

The ETF “invests in the full lithium cycle, from mining and refining the metal, through battery production.” The fund’s objective is to “provide investment results that correspond to the price and yield performance, before fees and expenses, of the Solactive Global Lithium Index.

The “before fees” portion is important, as management fees stand at 0.75% annually. Moreover, the current dividend yield is just 0.34%. The fund was started on July 22nd, 2010 and since that time has generated performance of 0.99% annually (as compared to 1.63% for the index and double-digit annual returns from an S&P 500 index).

While the ETF’s performance has been uninspiring, interest has ballooned in the security – as assets under management have gone from $68 million in June of 2016 up to $728 million in November of 2018 despite poor relative performance versus the S&P 500.

The fund holds 42 securities, but the top 10 positions make up over three-fourths of the ETF:

- Albemarle (17.8% of assets)

- FMC (16.9%)

- Quimica Y Minera Chil-Sp (9.3%)

- Tesla (5.7%)

- BYD (5.3%)

- LG Chem (4.9%)

- GS Yuasa (4.9%)

- Enersys (4.8%)

- Panasonic (4.2%)

- Samsung (4.1%)

We do not find this ETF attractive – the management fee and past record thus far have proven to be unimpressive – but it does offer an opportunity to discuss the major players in the industry.

Lithium Mining Stocks

For a long time the lithium mining industry was controlled by the “big three:” Albemarle (ALB), Sociedad Quimica Y Minera de Chile (SQM) and FMC (FMC). Rockwood Holdings was also a large player, but Albemarle acquired it several years ago. These three businesses accounted for 85% of the world’s lithium market share.

However, more recently China has entered the market in a big way. For instance, Australia’s largest mine, the Greenbushes, is 51% controlled by China’s Tianqi Lithium and 49% owned by Albemarle. Today the market share of the “big three” has dropped to 53%, while Chinese companies control about 40% of the world’s lithium market share.

Here are the five largest lithium-mining businesses:

- SQM

- Albemarle

- FMC

- Tianqi Lithium

- Jiangxi Ganfeng Lithium

While the Chinese stocks cannot be invested in easily, the top three lithium-mining businesses do offer publicly traded shares:

Lithium Mining Stock:Sociedad Quimica Y Minera de Chile (SQM)

Sociedad Quimica Y Minera de Chile ADR, more succinctly known as SQM, is a Chilean commodities producer with operations in lithium, potassium fertilizers, iodine and solar salts. Last year the company generated $2.2 billion in revenues and $428 million in net income.

On a per share basis, shares trade hands around $43; the company earned $1.68 in the last twelve months and paid out $1.78958 in dividends. These numbers equate to a trailing earnings multiple of 25.6 times earnings, with a 4.2% dividend yield and a 107% payout ratio. Keep in mind that the company’s dividend policy is to pay out all of its profits in dividends unless certain balance sheet requirements are not being met.

In addition to a dividend policy that allows for significant dividend fluctuations, we also caution that the security is subject to significant swings in earnings – ranging from $225 million in 2015 ($0.84 per share) up to $475 million in 2013 ($1.77 per share, two years prior). Moreover, the share price has swung dramatically as well – falling 75% from 2011 to 2015 and jumping back 275% to 2017 (only to fall 28% this year).

Still, the balance sheet looks strong. As of the most recent report the company held $760 million in cash and equivalents and $4.1 billion in total assets against $535 million in current liabilities and $2.1 billion in total liabilities.

SQM’s most impressive assets are the low-cost lithium deposits in Chile’s Salar de Atacama, which has both the highest concentration of lithium globally and benefits from the high evaporation rates in the Chilean desert. The company also has about half the market share in potassium nitrate and is the world’s largest producer of iodine. These three industries ought to benefit from the ongoing trends toward electric vehicles, increased crop production and healthcare spending.

The company has a long-term contract with Chile to extract 414,000 metric tons of lithium through 2030. Thereafter it is expected that this will be renewed, but this is somewhat unknown given Chile’s issues with former company Chairman Julio Ponce (which has since been resolved).

Lithium Mining Stock: Albemarle (ALB)

Albemarle Corporation is headquartered in the U.S. but operates in over 100 countries. The company has four operating units: Lithium & Advanced Materials (48% of 2017 sales and 55% of operating income), Bromine Specialties (22%, 22%), Refining Solutions (21%, 19%) and Other (9%, 4%).

Last year the company generated $3.1 billion in revenue and earned $433 million. Shares are currently trading hands around $97 and in the last twelve months Albemarle has reported $6.23 in earnings-per-share and paid out $1.325 in dividends. Those numbers equate to a trailing P/E ratio of 15.6, a dividend yield of 1.4%, and a 21% payout ratio.

Keep in mind that much like SQM, Albemarle’s profits are quite volatile. While the company has earned $6.23 in the last 12 months, this number has been as low as $1.94 and $1.69 in 2009 and 2014. Although we do note that the business has been profitable every year in the last decade.

As of the most recent quarterly report, Albemarle had $641 million in cash and equivalents and $7.5 billion in total assets compared to $1.1 billion in current liabilities and $3.8 billion in total liabilities. Despite volatile profits, Albemarle has a reasonable balance sheet that can continue to improve with a low dividend payout ratio.

Albemarle produces lithium from salt brine assets in Chile and two joint ventures in Australian mines. The company is also the second largest producer of bromine and a top producer of catalysts used in oil refining. Albemarle has a long-term contract through 2043 with the Chilean government to be able to extract around 80,000 tons of lithium per year.

Lithium Mining Stock: FMC Corporation (FMC)

FMC Corporation, also based in the U.S., operates in two segments: FMC Agricultural Solutions and FMC Lithium. Last year the company generated $2.9 billion in sales and earned $368 million in net profits.

The share price sits around $80 and in the last 12 months the company has reported earnings-per-share of $5.42 and paid out $0.66 in dividends. (That marks 14 straight quarterly payments of $0.165.) Those numbers equate to a trailing P/E ratio of 14.8, a dividend yield of 0.8%, and a payout ratio of 12%.

Precisely like SQM and Albemarle, earnings have improved significantly this year but in years past the underlying profit machine has been quite volatile. Earnings-per-share have come in as low as $2.08 and $2.47 in 2009 and 2015.

As of the most recent quarterly report FMC held $177 in cash and equivalents and $9.4 billion in total assets against $2.3 billion in current liabilities and $6.3 billion in total liabilities.

FMC is more of a crop chemical producer, as lithium only accounts for about a fifth of its profits. Moreover, while the company holds an 84.25% equity stake in Livent, the company’s former lithium segment, FMC plans to divest the rest of the stake in 2019.

Source: Morningstar, Value Line

Lithium Battery Stocks

The producer side is fairly concentrated although recently China has been taking significant market share from the “Big 3.” On the application side, there are a wide variety of battery makers and the market share is still somwhat up for grabs.

Here’s a sampling of the top-10 lithium-ion battery manufactures in the world according to ELE Times:

- Samsung SDI

- Panasonic

- Toshiba

- LG Chem

- Tesla

- A123 Systems

- eCobalt Solutions

- BYD

- Contemporary Amperex Technology

- Johnson Controls

As far as investable equity positions for U.S. investors go, Samsung, Toshiba, LG Chem, A123 Systems, eCobalt Solutions, BYD and Contemporary Amperex Technology are headquartered outside of the U.S. / listed on a foreign exchange. Which gives you a fair idea of where the majority of batteries are being produced.

Notably, Warren Buffett’s Berkshire Hathaway owns about a seventh of Chinese based BYD. Additionally, note that Johnson Controls recently sold off its Power Solutions business (including batteries) for $11.4 billion in net proceeds to Brookfield Business Partners L.P.

That leaves just two companies from the above list: Panasonic and Tesla.

Lithium Battery Stock:Panasonic (PCRFY)

Interestingly, Panasonic (PCRFY) supplies batteries for Tesla. However, this is only one portion of the Japanese business. Panasonic’s operating segments include Automotive & Industrial Systems (32%), Eco Solutions (18%), Connected Solutions (13%), Appliances (29%) and Other (8%).

Last year the company generated $75 billion in revenue and earned $2.2 billion in net profit. The share price is around $10 and Panasonic has reported earnings-per-share of $0.97 and paid out $0.27 in dividends over the last 12 months. That equates to a trailing multiple of about 10 times earnings, with a 2.7% dividend yield and 28% payout ratio.

As a general theme, earnings have been volatile. Panasonic reported significantly negative earnings in 2008, 2009, 2011 and 2012. However, since 2013 earnings-per-share have doubled. In the company’s most recent quarterly report Panasonic held $9.4 billion in cash and equivalents and $56.9 billion in total assets against $28.2 billion in current liabilities and $39.3 billion in total liabilities.

Panasonic is a diversified business, going well beyond the lithium battery market, with arms in electronic component mounting, appliances and home building products. This has the benefit of safety (when one division does poorly, other divisions can often make up the shortfall) but it can also dilute the growth potential a “pure play” lithium battery maker might have. Still, Panasonic is well positioned in the industry.

Lithium Battery Stock:Tesla

Tesla (TSLA) is a new business – founded in 2003 and publicly offered in 2010 – but it is a juggernaut in the industry. Here’s how the company describes itself:

“Tesla’s mission is to accelerate the world’s transition to sustainable energy. Since our founding in 2003, Tesla has broken new barriers in developing high-performance automobiles that are not only the world’s best and highest-selling pure electric vehicles— with long range and absolutely no tailpipe emissions —but also the safest, highest-rated cars on the road in the world. Beyond the flagship Model S sedan and the falcon-winged door Model X sports utility vehicle, we also offer a smaller, simpler and more affordable mid-sized sedan, Model 3, which we expect will truly propel electric vehicles into the mainstream.”

“In addition, with the opening of the Gigafactory and the acquisition of SolarCity, Tesla now offers a full suite of energy products that incorporates solar, storage, and grid services. As the world’s only fully integrated sustainable energy company, Tesla is at the vanguard of the world’s inevitable shift towards a sustainable energy platform.”

There is no doubt the company has a unique value proposition moving in a leading market for the future. However, the problem from a potential investment standpoint could be twofold: overall profitability and ongoing expectations.

From 2010 through 2017, Tesla racked up almost $5 billion in net losses. This has weighed heavily on both the balance sheet and the share count. The share count increased nearly 80% in this eight-year stretch, jumping from 95 million in 2010 to 169 million last year. Further, the company now holds almost $10 billion in debt, requiring ~$600 million in annual interest payments.

This puts a big burden on future endeavors. The good news is that the company just reported a net profit for the last quarter. The lesser news is that overall earnings will still be negative this year. Moreover, earnings expectations are all over the map for next year, but it remains that interest payments will make up a large portion of what the company might otherwise bring to the bottom line.

Further, the company’s penchant to continue to expand requires significant cash that may not be easy (or pleasant) to continue to raise through share offerings or debt. And if we see an economic downturn in the years to come, this could dramatically test the both company’s customer base and its balance sheet at a time when neither are in a position to be tested.

Additionally, valuation is a key consideration. So far you could not think about the firm on a trailing earnings basis, but instead on expectations for the future. Eventually, these expectations need to formulate into earnings.

The company enjoys a leading position in a growth industry, but you have to make difficult guesses about 1) how quickly the industry will grow, 2) what market share Tesla will take and 3) whether or not sustaining profits can ultimately be generated.

Source: Morningstar, Value Line

The Best Lithium Stocks

When you look across the publicly traded lithium market it’s hard to find a “pure play” lithium stock. Even among the lithium producers, each one has separate and important operations in other areas. Even an ETF focused specifically on lithium casts a wide net in a variety of industries.

On the mining side, you have the “Big 3” along with a group of Chinese companies working to take significant share. In general, the mining side looks somewhat interesting from an economic standpoint due to the inelastic demand of the raw material. Because lithium is essential, but not a huge cost driver in battery production, battery makers are unlikely to significantly curb demand in the case of higher prices. While miners cannot dictate higher prices by themselves, they are likely to benefit from higher prices if they come about from supply shortages / faster demand growth.

In our view, SQM and Albemarle look the most interesting on the mining side due to their premium position in Chile – a position offering the deepest reserves coupled with high concentrations and ideal environment.

While both businesses have seen significant upticks in profits as of late, the two securities offer separate value propositions. SQM is an ADR trading around 26 times earnings while paying out basically all of its profits in the form of a dividend. Alternatively, Albemarle is trading around 16 times earnings while paying out only a fifth or so of its profits as cash dividends.

The balance sheets are comparable, but the capital allocation decision-making is dramatically different. In this way, it’s our view that Albemarle looks a bit more attractive. What it lacks in dividend yield, it could make up for in lesser economic times if the company can intelligently deploy the surplus between profits and dividends. Moreover, with around half of its business in lithium, the company stands to benefit tremendously should the demand develop as anticipated in the decades to come.

On the battery side, it’s even more difficult to find a “pure play” lithium stock. There are plenty of companies in the market, but from an investment standpoint there is still a lot of uncertainty. Even Panasonic, which initially may look attractive due to its P/E ratio around 10 times earnings with a 2.7% dividend yield and diversified business line, has a record of negative earnings several times in the last decade.

While there very well could be many “winners” in the industry over the long-term, current investors will likely have to deal with substantial earnings volatility and high expectations in the short to intermediate-term.

Final Thoughts

Lithium is here to stay. There’s a reason that it has gained popularity, especially in the last decade. It’s a versatile metal that has afforded tremendous improvements in how we work, communicate and get around. Moreover, future demand appears robust as the move towards mobile devices, renewable energy and electric vehicles appears to be on the upswing (with the potential for a very long tail).

However, I am reminded of a Ben Graham quote:

“Obvious prospects for physical growth in a business do not translate into obvious profits for investors.”

The takeaway is twofold. Picking a growth industry, in general, may not be particularly difficult. For instance, it’s conceivable that just before (or even during) the ramp-up of trains, automobiles, planes, and the Internet a potential investor could point to these areas as “growth industries.” And indeed, they would have been correct. An investor pointing to the Internet, in say the mid-1990’s for example, would still be seeing that growth industry play out today.

Yet there are two problems. First, picking a growth industry may not be exceptionally difficult, but picking “winners” can test the best analyst. Out of the automobile or Internet just a handful of “winners” emerged, while hundreds or thousands were cast aside – once hyped, once with great expectations, but eventually for naught.

The second consideration is valuation. Even if you do happen to pick the “winners” you still have to be concerned about the price you pay. As a hypothetical, a security trading at say 40 times earnings that grows by 10% annually for a decade and later trades at say 20 times earnings would provide investors with returns of just 2.6% per annum. The consideration is not just, “will a company grow?” but more importantly, “will it grow fast enough to justify the current valuation?” Expressed differently, will current investors capture their “fair share” of investment results?

Additionally, while lithium appears poised to be in strong demand for the foreseeable future, you should also take into consideration the possibility of new technologies coming along as well. Demand alone is exciting, but it could lead to unexpected results if it creates enough new entrants.

Overall we are upbeat on the metal and its prospects over the intermediate to long-term, with the above caveats in mind. If you are interested in the industry, we would first look to Albemarle as roughly half of its profits are derived from lithium, it has stakes in important reserve areas around the world, the dividend payout ratio is modest and shares are currently offering a reasonable value proposition, especially if growth continues to formulate.

Otherwise, we place many of the other related securities in the “too hard” pile, as there are many unknowns coupled with tremendous expectations.

Disclaimer: Sure Dividend is published as an information service. It includes opinions as to buying, selling and holding various stocks and other securities. However, the publishers of Sure ...

more

I would add $NMX.CA and $ORRP