- Q3 under pressure despite record deliveries

- China, Europe competition weighs heavy

- Regulatory credits drop hit profitability

- Focus shifts to EV costs and robotaxis

Tesla reports after the market close on Wednesday, October 22, 2025.

Analyst commentary suggests the quarter will still be under pressure: the company faces margin and demand headwinds, particularly in China and Europe, as competition intensifies and its model lineup ages.

A key headwind is the sharp drop in regulatory-credit revenue that once significantly boosted Tesla’s profitability.

Beyond the headline numbers, investors will closely monitor several strategic signals: management’s update on the lower-cost vehicle strategy, progress on autonomous-driving and robotaxi ambitions, and how quickly Tesla can re-accelerate its core car business while defending margins.

With broader industry demand showing signs of flattening and margins squeezed, the narrative is shifting more toward credibility.

Can Tesla stabilize its current business and meaningfully advance its long-term vision of software, AI, and robotics?

Expected Numbers & Potential Stock Move:

- Revenue: ~ $24.4 billion, down ~2% year-on-year

- Adjusted EPS: ~ $0.75 per share (≈-7% year-on-year)

- Potential stock move (based on options): +/- 6%

More By This Author:

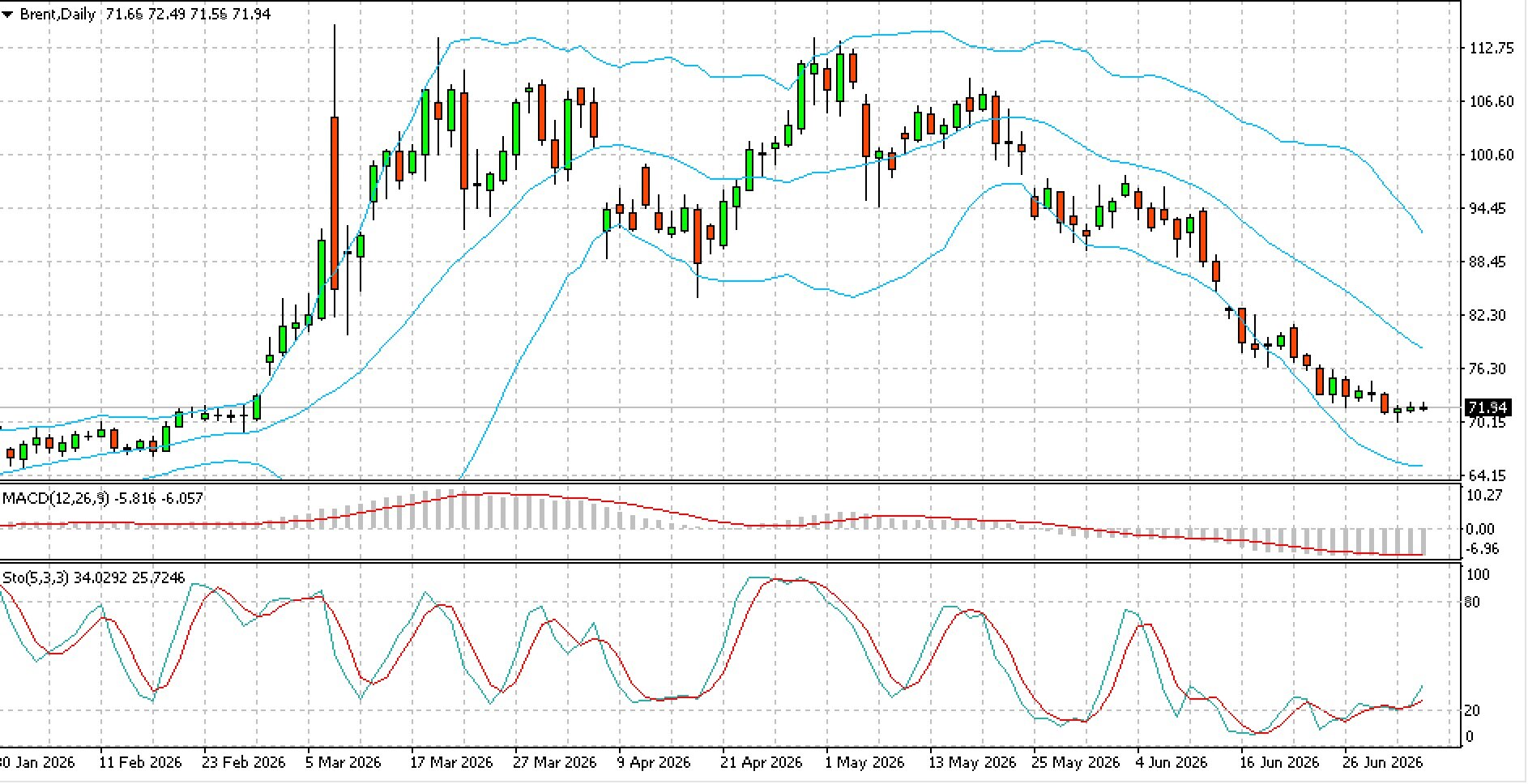

Brent’s Slide – Geopolitics & Oversupply In PlayS&P 500 Outlook: Dovish Signals Vs Trade Risks

This Week: AUD RBA Tone, US CPI Impulse & UK Growth Check

Comments

Log in or sign up to join the conversation.