Summary

* Tandy Leather (TLFA) is an absolute, historical, and relatively cheap valuation anomaly. The only national brand in a highly fragmented industry.

* Two decades of reporting consistent profits, high double-digit ROIC, and a compounding book value. The progress was stalled by accounting irregularities from inventory valuation and Covid pandemic.

* Amazon-resistant as the customers want to touch, smell and feel the product.

* Ownership of unencumbered real estate with a tax assessment value of around 8 million.

* Retained earnings per share increased 80.10% over the prior 5 years from December 2013 (4.06) to MRQ (7.32). In contrast with these intrinsic value improvements, the market price declined -68.74% over the same time period.

* Friday (11/13/20) an 8k filing was published. Comments include the following: positive YOY growth in September and October; anticipating the completion of the audit, re-listing on the Nasdaq; significant progress on consumer-facing initiatives, systems improvements, new web platform, centralized eCommerce, digital marketing, and other investments.

Tandy Leather is an illiquid nano-cap specialty physical store retailer in the dying niche of leather crafting. TLFA sells leather, leather crafts, and related supplies. It's in 42 states, 7 Canadian provinces, 115 North American stores. Spain is the only remaining location outside North America.

Inventory errors impacting multiple years were uncovered during December 2018. This discovery forced the restatement of financials. Nasdaq delisted the stock in August 2020. Yet, Tandy's delisting caused selling and created an investable opportunity. The stock is oversold for a consistent historically profitable, and asset rich company. A new CEO hired at the end of 2018 with a prudent capital allocating board now drives the Tandy opportunity.

Opportunity: Tandy's deep discounted valuation is absolute, historical, and relative.

The liquidation value of existing tangible assets is enough evidence to invest. However, the opportunity is more significant. A talented new CEO, the return of safe retail store shopping, Amazon resistance, and the material company ownership by the board will help move valuation higher. Additionally, the current delisting eliminates around 1.5 million in annual costs. This change alone improves EBIT by double digits. Although, after the restatement, relisting is likely to occur on the Nasdaq..

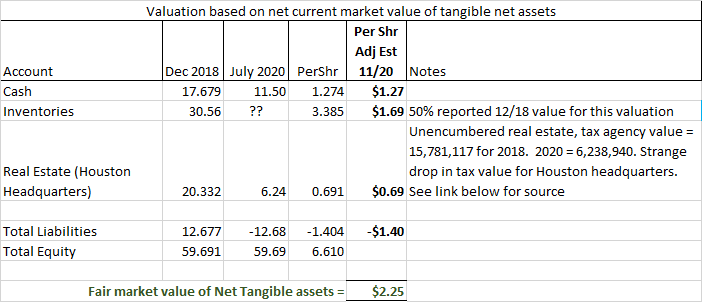

Tangible asset breakup value, excluding the sale of their operation.

Notes on the above table.

In August 2020 the 8k reported limited financial data for the period ending 07/2020. Cash balance was 11.50 million or 1.28 per share. Inventory balance reported the year ended December 2018 was 30.57 million or 3.85 per share. I reduced the value by 50% for this analysis. Ownership of unencumbered real estate with a tax assessment value of 15,781,117 for 2018. But in 2020 they report 6,238,940. Strange, a large tax value drop for Houston. Source: Tarrant County Tax Office (https://bit.ly/3eK3YIW)

Total liabilities were 12.68 million or 1.40 per share.

This simple analysis gives us an ultra conservative fair market value for net tangible assets of 2.35 per share.

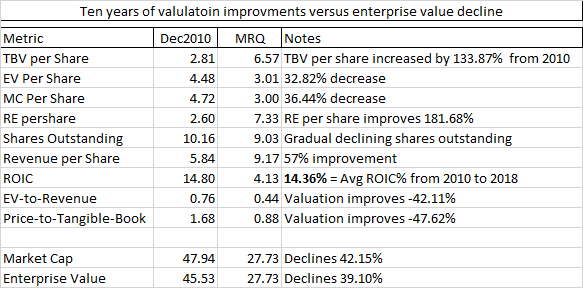

TLFA has compounded intrinsic value for years. Yet, the enterprise value declined sharply. The table below shows the irrational market value disconnect.

Notes on the above table.

Ten years of consistently profitable operations for the table above. The opportunity is obvious. ROIC averages 14.36%, retained earnings per share increased 181.68% over the ten-year period from 2010. Tangible book value per share improved by 133%. Yet, the enterprise value per share DECREASED -32.82% over the same ten year period. See more with the above table.

Additional factors listed below impacting a future higher stock price.

Tandy is illiquid and ignored with no analyst coverage. Its the only national retail brand in a highly fragmented industry. Further, CEO Janet Carr developed a strategic path with reported tangible progress before COVID and accounting irregularities.

Tandy Leather is Amazon-resistant as the customers want to touch, smell, and feel the product. The stores offer a continuous flow of classes. Hands-on help with projects/repairs from skilled staff. Endless positive 4.75 average customer reviews on Yelp - "level of service is unheard of these days," "Never met more kind and helpful employees in retail," "people are fantastic". Also, management owns 42.20% of the shares outstanding. Board member and value investors Jeff Gramm/Bandera Partners own 32% of share outstanding at an average price of ~ $8.44. Board member James Pappas/JCP Investments (9.60% at an average price of $7.50).

June 2, 2020 Management Presentation

The presentation graph above shows the vast opportunities for growth that exist for Tandy with hobbyists and businesses.

Risk:

A Covid resurgence during winter 2020 weakens its financial position. Sales continue their slow decline as their niche shrink. Additionally, difficulty in finding skilled labor and higher associated payroll costs. The growing cost to maintain a national retail storefront.

The legal, consulting, temp CFO, severance, and accounting fees for the year-long financial restatement will cost millions. The actual amount is material and unknown.

UPDATE

News report released after the market closed on November 13, 2020, and the above writeup. No material changes to the financial numbers reported above.

Tandy must restate prior financial statements before full financial results are reported. Therefore, it's not reporting regular financial results until the restatement is completed. But, limited financial results were reported on November 13, 2020.

Preliminary sales were approximately $15.8 million. A decrease of 3.1% compared to prior year's $16.3 million.As of September 30, 2020, the Company had $0.4 million of debt and $10.1 million of cash.

Janet Carr,CEO, said, "We were pleased with our third quarter sales performance following the shutdown of our entire store fleet from COVID-19 in Q2. In the third quarter, we were able to reopen substantially all of our remaining store fleet after the permanent closure of 8 stores. Strong web sales continued in Q3, even as stores have reopened. TOTAL SALES GROWTH IMPROVED THROUGH THE QUARTER WITH POSITIVE YEAR-OVER-YEAR GROWTH IN SEPTEMBER AND CONTINUING THROUGH OCTOBER.While the future remains hard to predict in the current economic climate and with COVID-19 case rates rising again, we have confidence in the overall trajectory of the business."

Financial restatement continues for the fiscal year-end 2018 10-K. And, financial statement audits for the fiscal year 2019 and the first three quarters of fiscal 2020. Tandy will apply to re-list its common stock on Nasdaq following the filing of all of its outstanding reports with the SEC.

Ms. Carr added, "We are looking forward to the completion of the audit of our restated financials, our re-listing on the Nasdaq, and a return to a regular, fulsome discussion of our financial results with investors.During this period, and despite the distraction and economic environment, we have made significant progress on our consumer-facing initiatives, implemented new comprehensive systems improvements, launched a new web platform and centralized eCommerce fulfillment capability and substantially increased digital marketing, and made other investments in building the foundation for our long-term growth."

Conclusion

TLFA offers a large margin of safety and a deep discounted extreme valuation in this overpriced market. Price alone would be enough due diligence. However, the opportunity is enhanced with the new CEO, Nasdaq relisting, investments in new systems, process improvements. Additionally, investors can wait for market recognition, mean reversion, continued profitability, or certain longer-term favorable corporate action.

Comments

Log in or sign up to join the conversation.