Spark Networks (LOV), A Risky Value Outlier

Spark Networks (LOV) is a global dating company. It focuses on the growing 40+ age demographic. And, religious minded singles looking for serious relationships.

Spark Networks has a growing portfolio of dating apps with branded websites. The company has around one million monthly paying subscribers. Brand names are Zoosk, EliteSingles, SilverSingles, Christian Mingle, Jdate, JSwipe. Affinitas GmbH merged with Spark Networks in 2017 to create the publicly listed LOV (Spark Networks) with the addition of Zoosk in 2019. Headquarters are in Berlin, Germany, with offices in New York and Utah.

The market is ignoring Spark's transformation and the extreme valuation discount to competitors. Yes, it's risky. But the rewards are asymmetrical if they prove further progress. Improvements include a new C-level management team. Research and development of 54.10M spent over the last two years for crucial product enhancements. Investor transparency by transitioning to U.S. domestic filer with quarterly filings and an investor outreach campaign.

Many of their prior one/two-year investments and changes will be realized in the second half of 2021. Such benefits are live streaming video (launch Q3 2021), social discovery functionality, improved matching algorithms, portfolio rebranded/look, customer relationship management. As a result, management expects higher 2021 revenue.

Financial results 1st Qtr 2021

May 17, 2021, the company reports Q1 results for the first time as a domestic filer. Sparks is now reporting quarterly, improving financial /operational transparency, and building a shareholder base.

Spark is presenting at several institutional investor conferences this quarter. The goal is to communicate details on overlooked growth and opportunities for improved profitability.

The target demographic is 40 plus and faith based. This segment is growing 7% faster than the market. Also, management is forecasting organic growth for Zoosk, EliteSingles, SilverSingles, and Christian Mingle.

Financial results were flat this quarter. Although, product enhancements continued along with finalizing the CFO search. YOY quarterly revenue decreased by $1.3M to $56.4 million compared to $57.7 million. The decline in revenue is because of a 3% decrease in average paying subscribers driven by Zoosk. The three largest legacy brands, SilverSingles, EliteSingles, and Christian Mingle, grew at low double-digits in North America.

The first quarter adjusted EBITDA was $4.8 million. A decrease of $2.7 million compared to $7.5 million in the first quarter of 2020. The decline is due to Zoosk and coupled with a headcount increase. Average paying subscribers decreased by 27,837 or 3% to 896,344 in the first quarter of 2021, compared to 924,181 in the same period for 2020. Spark's monthly average revenue per user (monthly ARPU) increased to $20.97 in the first quarter of 2021, compared to $20.8 in the same period of 2020.

The company ended the quarter with $17.3 million in cash and $96.1 million in debt. As of March 31, 2021, equity was $91.8 million, compared to about $94.9 million as of December 31, 2020.

Management reiterated 2021 guidance of $238 million to $244 million in revenues and adjusted EBITDA of $33 million to $36 million. Forecasted second quarter 2021 revenue is in the $54 million to $56 million range and adjusted EBITDA of $6 million to $7 million.

A significant opportunity exists in the fast growing 40 plus faith-based relationships segments, combined with their recognized brands and product improvement, which should push growth for years.

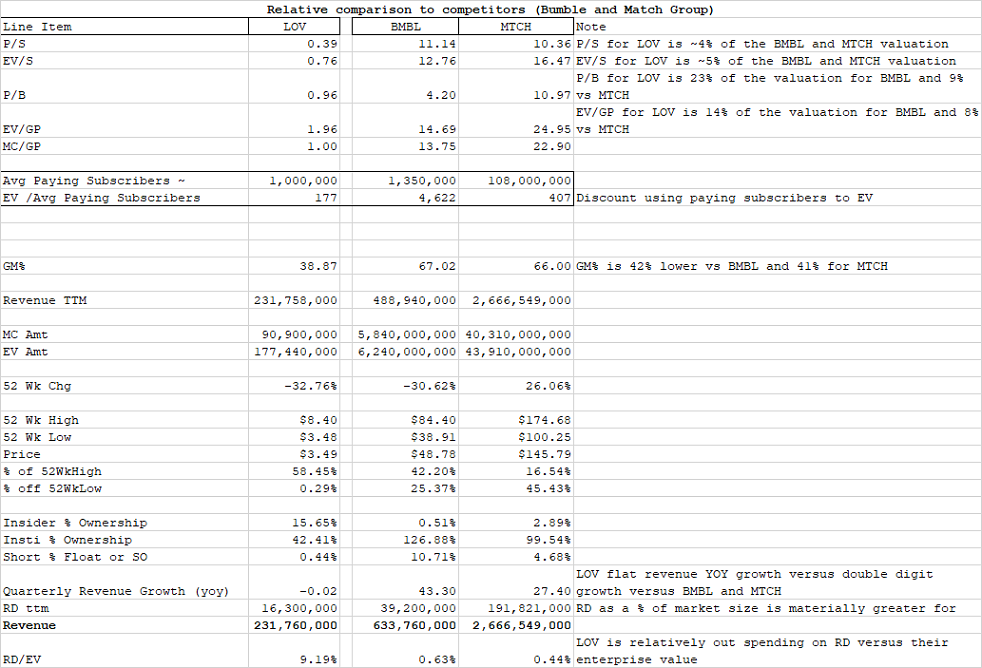

Relative valuation:

Relative valuation is impressive for LOV. It's a stretch to compare LOV to profitable industry leaders and much larger BMBL(Bumble) and MTCH (Match Group). But, Spark's price or enterprise to sales, gross profit, book value is startling at a ~90% lower valuation(see below). Lower valuation per subscriber versus MTCH and BMBL. Further, LOV is near its 52 weeks low and outspent on research and development relative to its market value for the prior two years.

Risks:

The inability to refinance large debt.

Negative cash flow, and failure to post positive net income.

Excessive advertising expense to maintain subscribers.

Permanent damage to the brand's value if subscribers decline. And critical mass is not reached to make the brand attractive for new online daters.

Delta Covid variant could impact demand for online dating.

Conclusion:

LOV is RISKY! But it trades at an EXTREME relative discount. And, the discount coupled with the transformation progress makes LOV a RISKY BUY. The extreme discount includes market value to sales, gross profit, book value, and research development. Further, the market's valuation on its per subscriber contribution is the industry's lowest. (see table above). Also, the online dating market is growing with limited competition from four national companies, including Spark Networks. In addition, MTCH and BMBL are public. Further, LOV is the worldwide leader in faith-based dating brands, coupled with the 40+ seeking a long-term relationship.

Spark is at the end of its transformation with new management, expense reduction opportunities, product enhancements, and consolidating brands under a single platform. Additionally, debt refinancing is likely with the new CFO and has an attractive asset-light business model with recurring revenues trading at multiples seen with a distressed retailer. Management is forecasting improved results. Free cash flow reported was 25.95M for the prior period 06/2018 to 12/2020, 37.17M for CFFO. Further, Spark transitioned to U.S. domestic filer with quarterly filings and with an investor outreach campaign. The new management team is incentivized with equity (12.09M in stock-based compensation from 06/2018 to 12/2020). The new team replaces a prior management disaster.

Long: LOV