The S&P 500 (Index: SPX) saw its upward momentum during the trading week ending Friday, 1 August 2025. The index closed the week at 6,238.01, down a little over 0.9% from the preceding week.

The U.S. stock market entered the week with positive momentum, gaining almost 1.5% on Monday, but that changed on Wednesday as a divided Fed signaled it would not only would hold the Federal Funds Rate steady, it would likely continue that policy through September, when it had previously been expected to resume cutting the U.S. economy's base interest rate. As they did, Fed officials cited the strength of the U.S. economy and the continued belief among Fed Chair Jerome Powell and several other members that tariffs will push inflation higher.

On Friday, the S&P 500 dropped 1.6% after the July 2025 jobs report came out, which was much worse than expected. In addition, previous month's estimates of the number of employed Americans was revised sharply lower. The much-lower-than-expected employment situation numbers signaled the U.S. economy is not growing as much as expected, which means the outlook for publicly-traded U.S. businesses is worse than expected, which led to the drop in their stock prices.

The problem of the Bureau of Labor Statistics reporting overly-optimistic employment data only to substantially revise them downward later has become a chronic issue in recent years, as the BLS' employment situation report has become much less reliable for policymaking. President Trump reacted by firing the Bureau of Labor Statistics manager who has overseen the production of the BLS' employment situation report on Friday. The downwared revisions may also have influenced the unexpected announcement of a Federal Reserve official who had been among those backing Jerome Powell's "no rate cut" policy because the previously reported jobs numbers appeared so strong.

Here is the latest update of the alternative futures chart, in which we find the trajectory of the S&P 500 is near the bottom of the redzone forecast range we added to the chart a week earlier.

- Snapshot on 1 Aug 2025")

After so many weeks in which trade deals and tariffs have been the leading story, it's strange that President Trump's decision on Friday, 1 August 2025 to proceed with higher tariffs on nations that haven't cut deals with the U.S. didn't appear to carry more weight in the week's market moving headlines. Here are the headlines of note pulled from the newstreams of the week that was.

Monday, 28 July 2025

- Signs and portents for the U.S. economy:

- Fed minions still expected to hold off resuming rate cuts in July 2025;

- Bigger trouble developing in China:

- ECB minions say they need to see Eurozone economy turn for worse before delivering another rate cut, Germanys Prime Minister says 'hold my beer':

- S&P, Nasdaq again close at record highs, trade choppy

Tuesday, 29 July 2025

- Signs and portents for the U.S. economy:

- Fed minions thinking about changing how they do things at Fed:

- Details of US trade deal being discovered in Japan:

- Wall Street slides amid a post-earnings slump as investors await FOMC decision

Wednesday, 30 July 2025

- Signs and portents for the U.S. economy:

- Fed minions hold rates steady as expected, won't commit to rate cut in September 2025:

- Bigger trouble developing in China:

- Eurozone GDP growth better than expected, ECB minions think getting China to export its deflation to Eurozone would be helpful:

- U.S. stocks recoup some losses to end mixed, but Fed's Powell rattles investors

Thursday, 31 July 2025

- Signs and portents for the U.S. economy:

- Fed minions see small uptick in PCE inflation, speculation builds negative jobs news might force them to cut rates:

- Bigger trouble developing in China:

- BOJ minions hold Japan's interest rates steady, but hint they're still thinking about hiking them in future:

- ECB minions get better economic data for Eurozone:

- Wall Street slumps to a negative close as trade jitters counter earnings euphoria

Friday, 1 August 2025

- Signs and portents for the U.S. economy:

- Fed minions see minion quit after bad jobs news is released, faces building pressure for rate cuts:

- Bigger stimulus developing in China:

- BOJ minions say US tariffs will likely have negative effect on Japan's business, economic growth, but are thinking about hiking Japan's interest rates again:

- ECB minions see some improvement in Eurozone economy, may not need to keep cutting rates:

- Wall Street sinks after 'worst major economic report in the post-pandemic era'

After the Fed held rates steady on Wednesday, 30 July 2025 and the big downward job revisions on Friday, 1 August 2025, the CME Group's FedWatch Tool forecasts the Fed will continue hold the Federal Funds Rate in a target range of 4.25-4.50% until its 17 September (2025-Q3) meeting, when it is expected to cut the rate by a quarter percent. Beyond that date, the FedWatch tool now anticipates additional quarter point rate cuts will take place at six-week intervals, on 29 October (2025-Q4) and 10 December (2025-Q4).

The Atlanta Fed's GDPNow tool projection of real GDP growth in the U.S. during the current quarter of 2025-Q2 dropped from +2.4% in the previous week to +2.1% this week.

More By This Author:

Median Household Income In June 2025Market Cap Vs. Dividend Yield For S&P 500 Companies

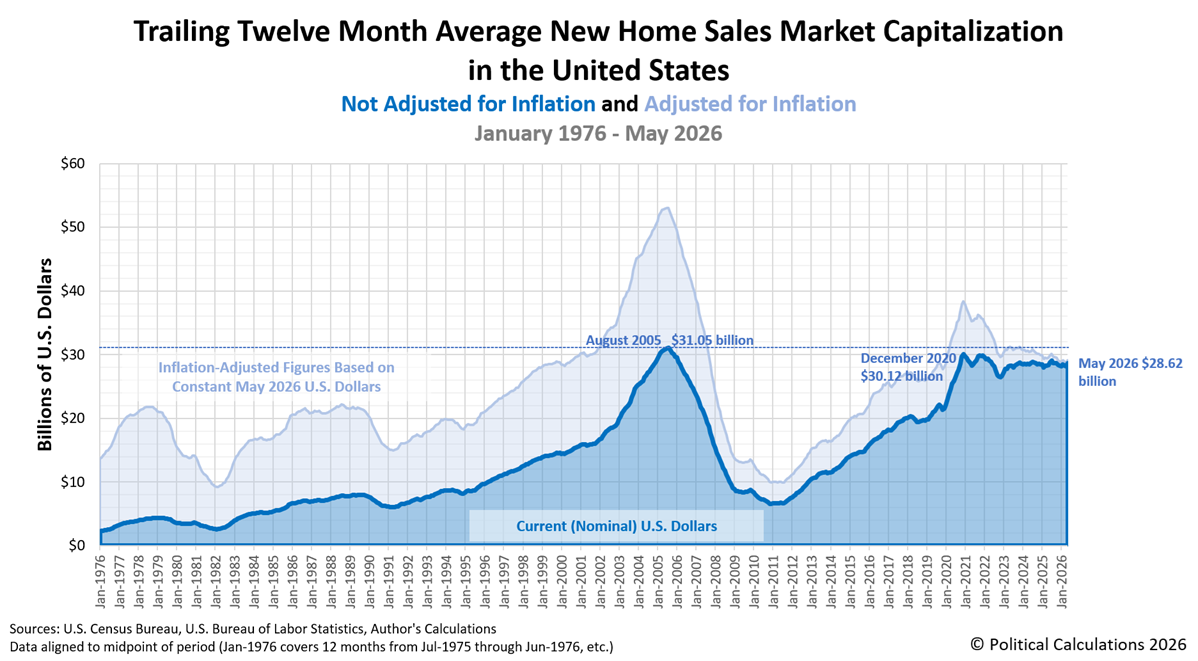

New Home Market Cap Rises As Number Of Sales Decline

Comments

Log in or sign up to join the conversation.