Something Shiny, Something New - Visa

Visa, Inc., the world’s leader in digital payments, provides secure and reliable payment processing through VisaNet, its proprietary global payment processing network. Visa’s customers include 16,000 financial institutions, co-branded partners, fintechs and affinity partners that issue Visa-branded products and credentials accepted by 100 million merchant locations worldwide. Visa also offers a global ATM network; Visa Direct, a real-time push payments platform; and value-added services including fraud management, security services, data analytics and consulting services.

Global Leader

Visa’s (V) journey began in 1958, the year Bank of America launched the nation’s first consumer credit card program. International expansion followed in 1974 and, in 1975, Visa issued the first debit card. In 2007, regional businesses around the world were merged to form Visa, Inc.—a name chosen because it sounds the same in all languages. In 2008, Visa went public in one of the largest initial public offerings (IPOs) in history.

Today, Visa facilitates digital payments across more than 200 countries processing 164.7 billion transactions in fiscal 2021. Visa cards issued top 3.7 billion, including 1.16 billion credit cards and 2.56 billion debit cards. Visa generates revenue by facilitating transactions through its four-party payment “railway” which includes Visa, the card-issuing financial institution or credential-issuing fintech, the merchant and the merchant's bank. Visa collects minute slices of each transaction as fees through services, data processing and international transaction revenues.

During the fiscal year ended 9/30/2021, most of Visa's revenue was generated through these three streams. Visa generated about 35% of its revenue from Services based on payment volume of Visa-branded cards; 40% from Data Processing earned for transaction authorization, clearing and settlement based on the number of transactions processed; 20% from International cross-border transactions and currency conversion activity; and 5% from value added services including risk, fraud and dispute management, security services, tokenization, data solutions and consulting. Client incentives agreed to in customer contracts offset fiscal 2021 revenues by about 26%.

As the payment industry continues to evolve, Visa faces challenges from both disruption and regulatory risks, including anti-trust actions, government mandated fee caps and creation of alternative payment networks by governments and central banks. Visa also faces pressure from large merchants like Amazon to reduce fees.

However, given Visa’s dominant global position with its payment network infrastructure and sizable cost advantages, its trusted and reliable brand and management’s focus on innovation through self-disruption, Visa will likely continue to lead and benefit from the strong secular trend toward digital payments.

Profitable Growth

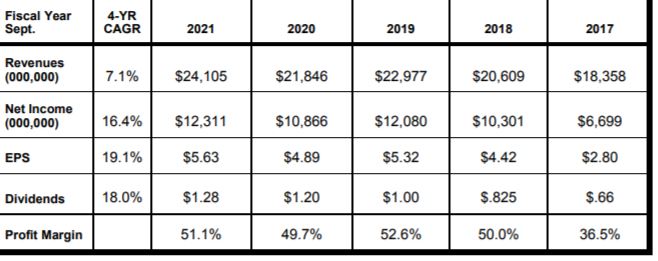

Visa generated healthy growth during the past five years with revenues compounding at a 7% annual rate as net income grew at a 16% annual pace and EPS increased at a 19% clip. The highly scalable nature of Visa’s payment infrastructure along with its inherent cost advantages enable the firm to consistently deliver net profit margins hovering around 50% and returns on shareholder equity exceeding 30%.

For fiscal 2021, Visa’s revenue increased 10% to $24.1 billion with net income charging ahead 13% to $12.3 billion and EPS up 15% to $5.63.

Robust Cash Flows

Visa maintains a strong balance sheet thanks to the company’s excellent free cash flow generation that has compounded at a 14% annual rate during the past five years. This enables the company to invest in the business, return cash to shareholders and acquire new, potentially disruptive platforms. During fiscal 2021, Visa returned $11.5 billion to shareholders through dividends of $2.8 billion and share repurchases of $8.7 billion at an average cost per share of $219.34.

Building on its history of increasing dividends annually since its IPO, Visa recently announced a 17% dividend increase to $1.50 per share. In June, Visa agreed to the $2.2 billion acquisition of Tink, a leading open banking platform in Europe that enables banks and fintechs to develop data-driven financial services and person-to-person transfers. Visa also plans to acquire Currencycloud, a global platform that enables banks and fintechs to provide currency exchange solutions for cross-border transactions.

Investors seeking to bank long-term returns should consider stuffing their wallets with shares of Visa, a high-quality global leader with profitable growth and robust cash flows.

Buy.

Disclaimer: Copying, reproduction or quotation is strictly prohibited without written permission. Information presented here was obtained from sources believed to be reliable but accuracy and ...

more

{kind=link}