Small-Caps Set To Sizzle

In this week’s Dirty Dozen [CHART PACK], we look at the worst bond returns in over 200 years, cover more reasons to be bullish on small-caps long-term, discuss the key thing to watch for risk-on to continue, check in on our ETHUSD long trade, talk about why US large caps are still grossly overvalued, and peek in on what stocks retail are buying, plus more…

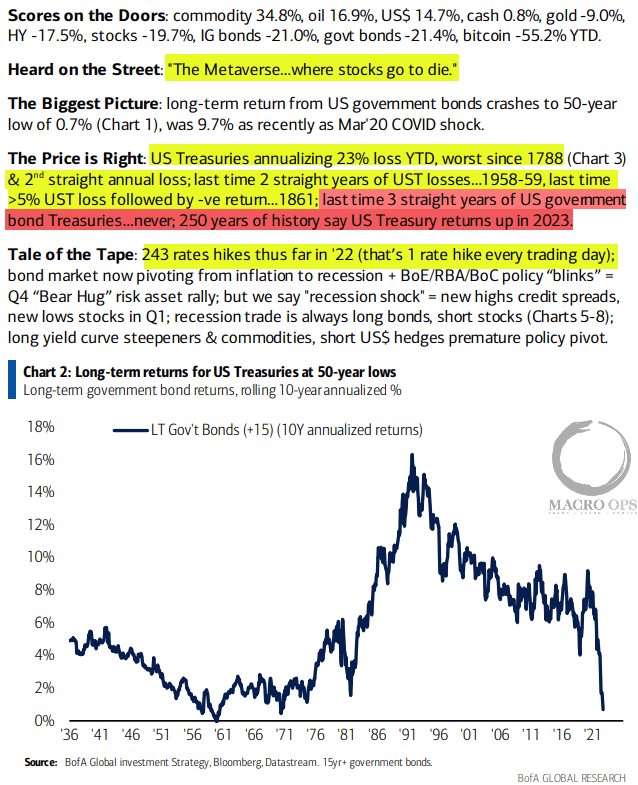

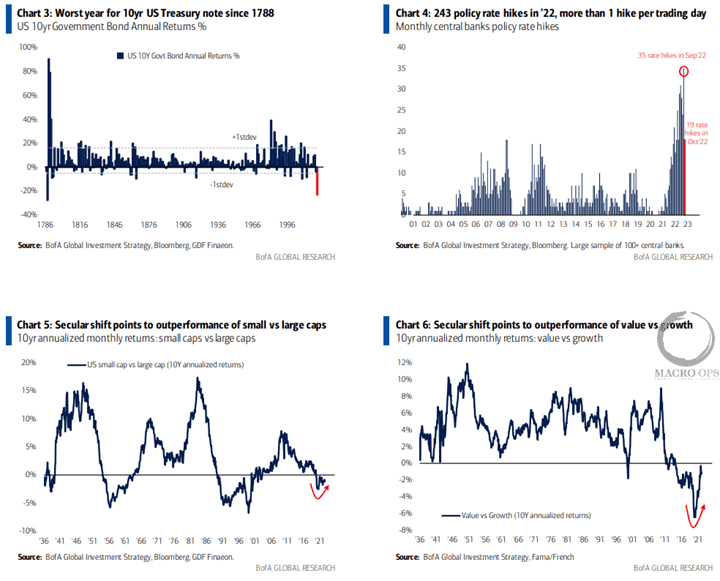

- US Treasuries annualizing 23% loss YTD, worst since 1788 & 2nd straight annual loss… last time 3 straight years of US government bond Treasuries… never; 250 years of history say US Treasury returns up in 2023. BofA Flow Show summary with highlights by me.

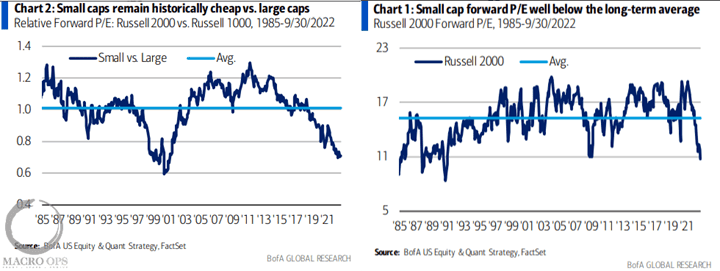

- Secular shift points to outperformance of small vs large caps…

- We discussed the absolute and relative value that small-caps offer earlier this month (link here).

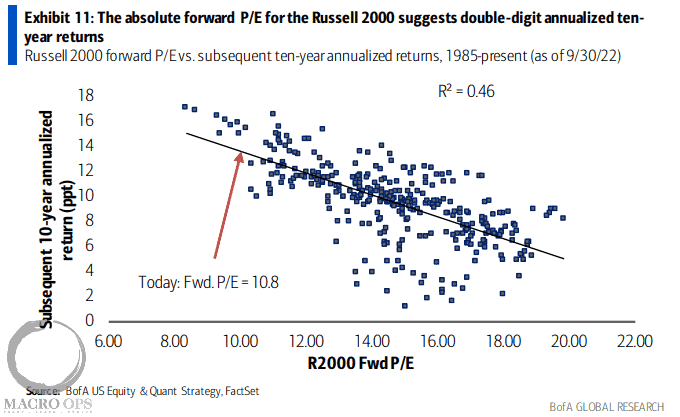

- Historically, when small caps have traded at a forward PE of 10x, they’ve seen double-digit annualized returns over the following decade.

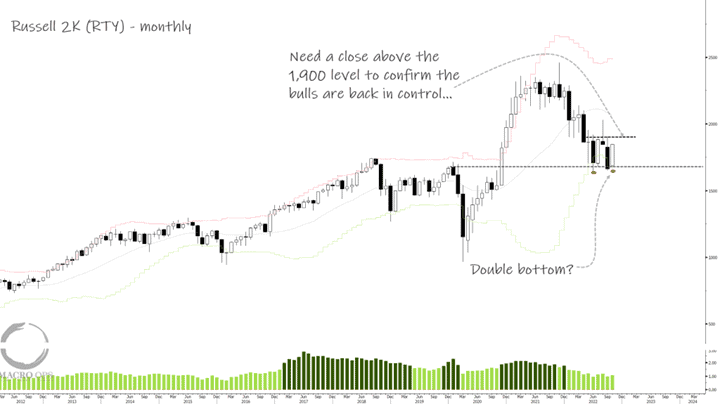

- Out of the major US indices, R2K has the best-looking monthly setup. Strong close on its highs. Potential double bottom in place. A monthly close above 1,900 would be a significant risk-on signal.

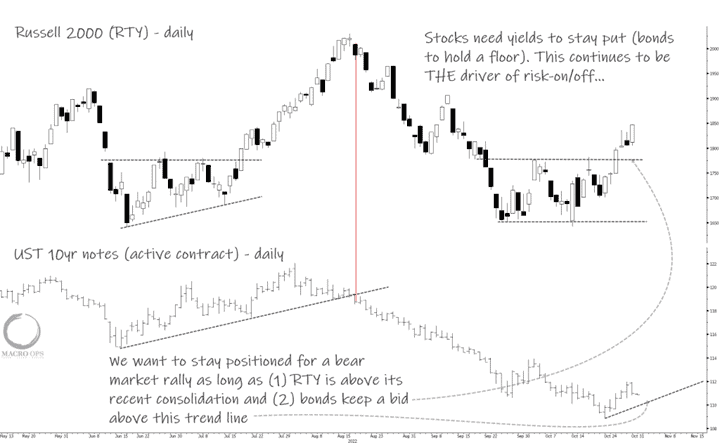

- But we’re playing a counter-trend rally here and the key thing to watch continues to yield. The breakdown in bonds killed the last rally in stocks and they’ll do the same here if they can’t hold their recent floor.

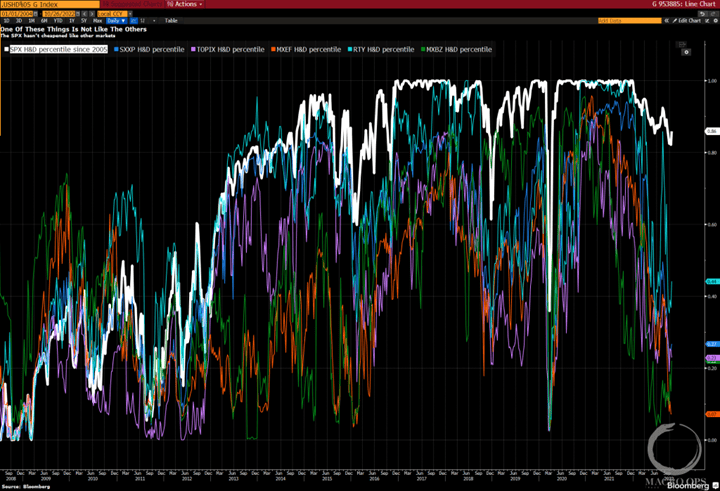

- Here’s a great chart from BBG’s Cameron Crise which shows a time series of his “hopes-and-dreams” indicator. This indicator “represents the proportion of equity-index valuation not explained by book value or the net present value of the next three years’ earnings”. A lower reading equals a more reasonable valuation — fewer hopes and dreams baked into the price.

The SPX is represented by the white line which remains considerably higher than other major markets.

(Click on image to enlarge)

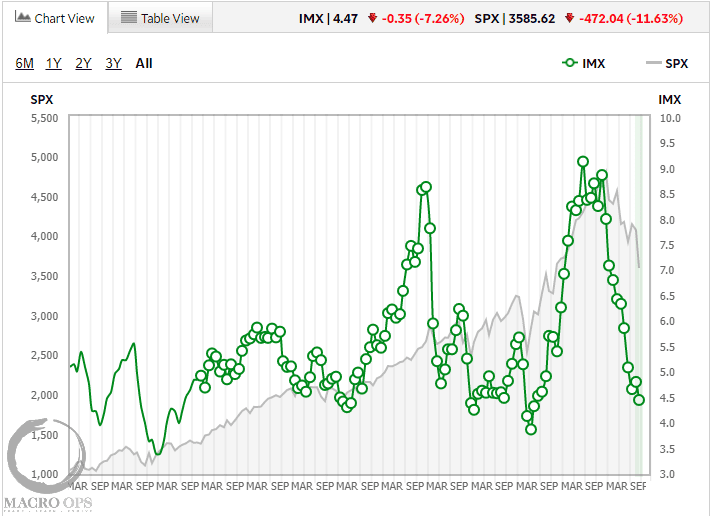

- One measure I like to occasionally check in on is TD Ameritrade’s IMX as it shows hard positioning data. The IMX tracks the “holdings, positions, trading activity, and other data from a sample of 11 million funded client accounts.” Here are some interesting highlights from their September report.

“Investment exposure in TD Ameritrade client accounts decreased last period…TD Ameritrade clients were, however, net buyers of equities in September. Despite every S&P sector trading significantly lower during the period, the sector mix showed buying interest in every S&P 500 sector except for Health Care. The buying interest was particularly strong in the Information Technology sector, which was down nearly 15% during the September period.”

The most popular names bought amongst TDA clients were: TSLA, AMZN, GOOGL, MSFT, AAPL, NVDA, and AMC. The names that were most sold were: XOM, NFLX, BP, and MS.

- Strong private balance sheets suggest the Fed may have a tougher time hitting the brakes on the economy, which means rate hikes might need to go on for longer than expected.

Via the WSJ “Household, nonfinancial corporate and small-business sectors ran a surplus of total income over total spending equal to 1.1% of the gross domestic product in the quarter of April to June, according to economists at Goldman Sachs Group Inc. Using a three-year average, the measure is healthier than on the eve of any U.S. recession since the 1950s.”

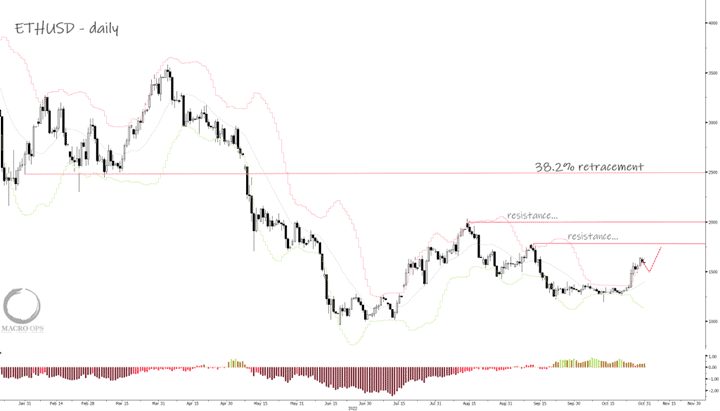

- We spent the last few weeks pounding the table on the setup in ETHUSD (a major compression regime). The pair broke out last week and ran fast. We’ll look to add to our position on pullback reversals as long as the FOMC doesn’t kill the risk-on rally this week and bonds stay bid.

- Bridgewater discussed the potential for a higher longer rate path to blindside markets a few weeks back. Here’s the link and an excerpt.

“A near-term economic downturn, an extended period of above-target inflation, and the second round of tightening is not discounted in the markets at all. What the markets are now discounting is that the first round of tightening is nearly over, that growth will not slow much, and yet inflation will quickly fall to desired levels and that this will allow a cut in interest rates in 2023 and 2024 that restores a normal risk premium in bonds. There is a lot of room for markets to be blindsided by what we see as the normal sequence of events which typically follows the conditions that exist today.”

- Tom Morgan is one of the more interesting and insightful writers on the interwebs. His most recent piece titled “At The Tipping Point” does not disappoint. It’s a high-level meta-discussion on where we are and where we may be headed. Here’s the link.

Thanks for reading.

Stay frosty and keep your head on a swivel.

More By This Author:

A BIG Trend Is Brewing

A Rare Buy Signal In Tech Stocks

Financial Conditions Are About To Get More Restrictive

Disclaimer: All statements are solely opinions and are for educational purposes only.