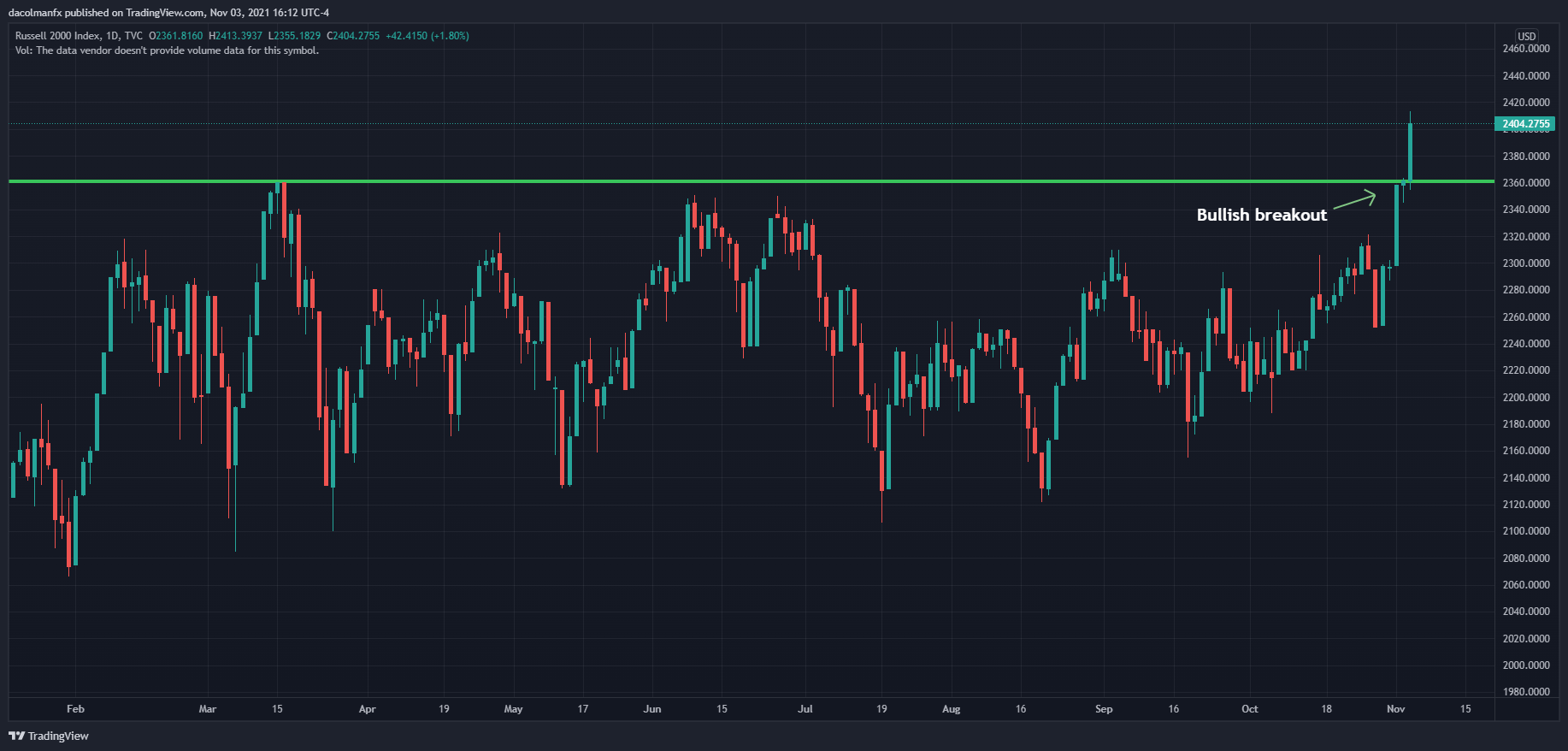

The Russell 2000 surged 1.8% to an all-time of 2,404 on Wednesday, supported by positive sentiment towards domestically oriented small and mid-caps following strong services and employment data. For context, the ISM non-manufacturing indicator rose to 66.7 in October from 61.9 in September, blowing past expectations and hitting its highest level on record, a sign that demand is accelerating in the most important sector for the economy. Labor market results also topped forecasts, with private businesses hiring 571,000 workers last month according to the ADP Research Institute, versus estimates of 370,000 new jobs.

The Russell 2000's upward momentum accelerated in the afternoon despite the Fed's decision to startdialing back on pandemic-related stimulus amid substantial progress toward its dual mandate. At the conclusion of its two-day meeting, the FOMC left the federal funds rate unchanged at 0.00% - 0.25% and announced that it will begin phasing out its $120 billion monthly asset-buying scheme beginning in mid-November, reducing total purchases by $15 billion per month to conclude the program by the middle of next year, although it noted that it is prepared to adjust the pace of balance sheet normalization should changes in the economic outlook warrant such action.

The “taper announcement” was fully discounted, so it failed to fuel any kind of turbulence or selling activity in risk assets. At the same time, the tone embraced by the central bank had a dovish tinge,so traders were encouraged to pile in to bid stocks higher in anticipation of further upside.

During the post-meeting press conference, Chairman Powell took the opportunity to reiterate that the inflationary trend is caused by pandemic dislocations and that monetary policy tools will not address supply-driven price pressures, implicitly pushing back against Wall Street bets that the liftoff will have to come faster than anticipated to address the ongoing economic challenges.

For added context, the front-end of the curve has undergone a violent repricing lately, with the 2-year U.S. Treasury yield jumping from 0.28% to 0.49% in less than 5 weeks as 2022 rate hike expectations have been firming steadily in the futures market. On balance, Powell’s message reinforced the narrative that the Fed will be patient and will not respond to transitory high inflation readings by raising rates prematurely.

The FOMC's decision not to bow to market pressure to adopt a hawkish stance, as other central banks have done recently, may be a signal that monetary policy will remain accommodative for longer, a positive outcome for equities. While some short-term profit-taking is possible, equities are likely to remain supported through the end of the year, but leadership could shift to cyclical plays as the recovery picks up traction, especially in the services sector. That said, the Russell 2000, which has traded sideways since mid-March and has just staged a bullish breakout, could run higher and command strength over the medium term.

RUSSELL 2000 DAILY CHART

(Click on image to enlarge)

Source: TradingView

Comments

Log in or sign up to join the conversation.