Legendary outlaw Robin Hood stole from the rich; his modern-day namesake, Robinhood Markets, wants them to give willingly. Having recovered from a long slump, the $18 billion online brokerage led by Vlad Tenev wants to be considered a peer to the world’s financial titans. This strategy involves fresh risk.

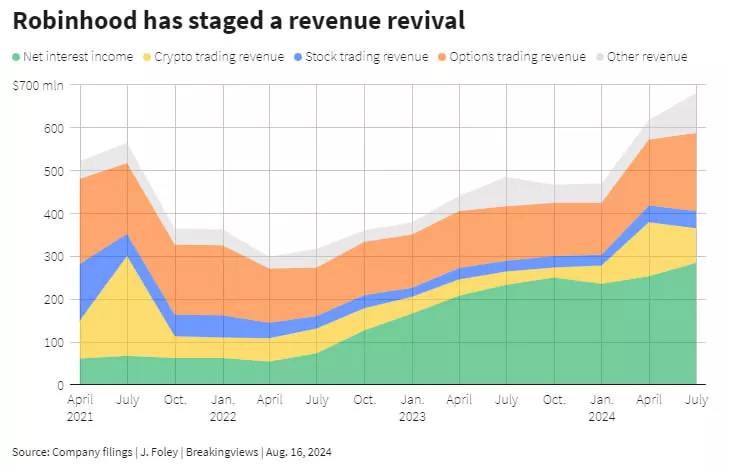

Robinhood’s market valuation collapsed after an exuberant 2021 initial public offering that rode the coattails of at-home traders during the pandemic. Rising interest rates, as well as the return of buying and selling stocks and cryptocurrencies, have powered a roughly 60% pickup in the stock price this year. Robinhood’s interest revenue, for example, has quadrupled from three years ago, even as transaction revenue has fallen.

The company looks different now, and not just because it dramatically slashed the workforce. Tenev and co-founder Baiju Bhatt are focused on “active” traders instead of recreational ones. Robinhood Gold, a member’s club that costs $5 a month, targets habitual users with perks such as 5% returns on cash. This group now makes up 8% of the customer base, but the majority of Robinhood’s revenue.

(Click on image to enlarge)

Tenev’s original gambit was to offer commission-free trading, partly funded by selling trades to market makers like Citadel. Now, it’s also to supply products subtly subsidized by Robinhood.

The company’s margin lending is the cheapest around, and its balances of $5.4 billion are already a third bigger than when it slashed its lending rate in May. Retirement assets get generous bonuses, and Robinhood’s credit card offers lavish terms such as a 3% cash reward on all spending.

Borrowing from today’s profit to buy tomorrow’s is common in technology, evidenced by the artificial intelligence mania. It’s harder to assess financially, though, when the investment comes as underpriced lending or taking credit risk onto the balance sheet. Robinhood’s IT systems may be more efficient than those of incumbents like Citigroup or JPMorgan, but they also lack decades of experience navigating economic ups and downs.

Credit cards, while just 1% of Robinhood’s revenue, are an example. The company wrote down its card loans at an annualized rate of around 20% in the latest quarter; Citi’s equivalent rate is 6%. It’s almost all tied to a credit card portfolio Robinhood bought last year, and not the new Gold card unveiled in March. But as Robinhood’s product grows – the waitlist is over 1 million long – so will the associated risks.

The reward is admittedly huge. Dying Baby Boomers should bequeath a $53 trillion pot of wealth to descendants and charities by 2045, according to financial planners Cerulli Associates.

Robinhood already has at least 12 million customers under 34, more than one-third of today’s American young adults who own stock, based on Gallup survey findings. It’s a promising start, but unlike the fictional Robin Hood who took wealth distribution into his own hands, Tenev has a longer and more uncertain wait.

Context News

On Aug. 7, 2024, Robinhood Markets reported $682 million of revenue in the second quarter of 2024, a 40% increase year-on-year. A little less than half the online brokerage’s revenue came from trading fees on equities, options, and cryptocurrencies. Total assets under custody were $145 billion at the end of July, according to a separate monthly update, 53% higher than a year earlier.

Robinhood in May cut the rates on its margin lending business, which extends credit to customers to buy securities. At the end of July, it had $5.4 billion such loans outstanding, versus $4.1 billion at the end of April.

More By This Author:

S&P 500 Earnings Dashboard 24Q2 - Friday, Aug. 23U.S. Retail Earnings Update - Thursday, Aug. 22

Russell 2000 Earnings Dashboard 24Q2 - Thursday, Aug. 22

Comments

Log in or sign up to join the conversation.