Not every dividend stock has to come with a sky-high yield or tech hype. Sometimes, the best performers are the quiet giants—those that simply do the work, year after year. When you find a business that touches almost every part of the economy and still manages to grow, that’s worth a closer look. One of the most influential financial machines in the U.S. might be hiding in plain sight.

A Network that Prints Cash

Behind its brick-and-mortar branches and digital dashboards lies one of the most powerful banking machines in the U.S. Few institutions wield such widespread influence across consumer, commercial, and capital markets. Whether you’re swiping a card, applying for a mortgage, or trading equities, chances are Bank of America is somewhere in the background.

Bank of America (BAC) business model thrives on scale. It runs through four main arteries: Consumer Banking, Global Wealth & Investment Management (GWIM), Global Banking, and Global Markets. From Main Street to Wall Street, it services both everyday depositors and billion-dollar institutions. Its dominance in deposits, card usage, and wealth management builds deep, sticky client relationships. Merrill Lynch, now seamlessly integrated, brings institutional-grade firepower to its wealth arm, while digital platforms like Erica and Zelle reinforce customer stickiness in the retail world.

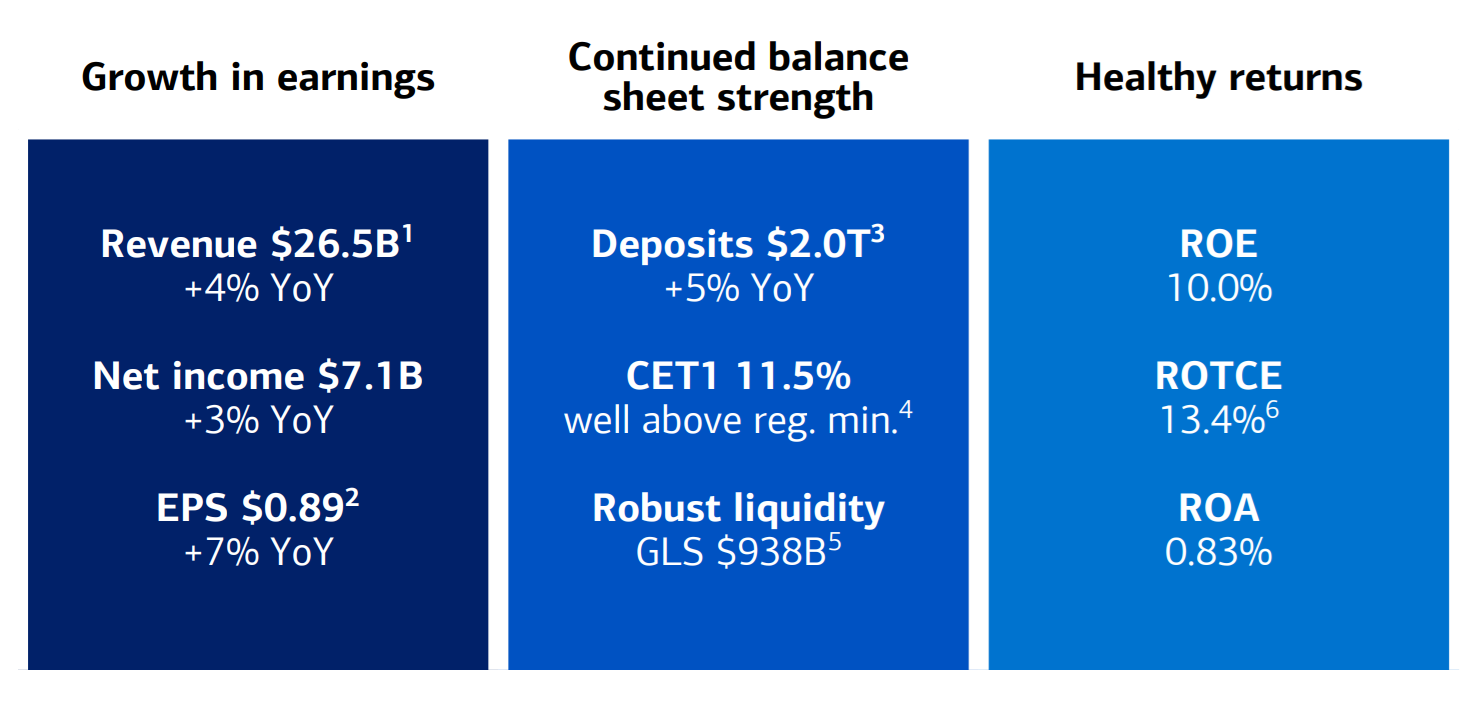

Bank of America (BAC) Q2 2025 Highlights from its presentation.

When a Scale Becomes a Superpower

Bull Case: Efficiency and Reach in a Higher-Rate World

Bank of America’s multi-segment model is designed to thrive when interest rates rise — and that’s precisely where we’ve been. With over $1.9 trillion in deposits and a disciplined loan book, BAC’s net interest income is a powerhouse. In 2025, it’s projected to grow by 6.8% year-over-year. The bank’s digital transformation has also paid off: nearly 75% of households now use digital platforms, reducing overhead and boosting margins.

Merrill Lynch provides a reliable stream of fee-based revenue, while Bank of America’s presence in fixed-income and equities trading gives it another gear in volatile markets. Wealth and Investment Management, which includes Merrill and the Private Bank, delivered an 8% YoY boost in Q1 thanks to a 15% increase in asset management fees. This combo of stability and cyclical upside is hard to beat.

Retail growth is also alive and well. BAC continues to invest in new financial centers while optimizing its branch network, ensuring both reach and cost efficiency. It has one of the largest technology budgets in the industry, further insulating its moat against fintech threats.

Bear Case: Regulatory Shadows and Competitive Tensions

For all its muscle, BAC isn’t without vulnerabilities. Over 50% of its revenue still comes from net interest income, which means falling rates or economic softness can compress earnings quickly. Additionally, as a systemically important financial institution (SIFI), the bank remains under the regulatory microscope. Compliance burdens and stress test requirements can limit flexibility.

Loan books are solid today, but a recession could change that in a flash. Consumer delinquencies are creeping upward in some segments, and charge-offs may rise if employment softens. The fintech threat is also real. While BAC is well-resourced to fight back, nimble disruptors often set the pace for customer expectations.

Finally, the competitive field is intense. JPMorgan Chase continues to be a juggernaut in both investment and consumer banking, while Wells Fargo is on a slow but steady rebound. BAC must continually defend its turf.

What’s New at BAC

The bank kicked off the year with solid performance across nearly all divisions. Here are the key takeaways from its latest quarterly report:

- Revenue rose 4% YoY, topping $26.5B.

- EPS surged 18%, outpacing analyst estimates.

- Net interest income climbed 3%, benefiting from a favorable rate environment.

- Non-interest income increased 10%, driven by asset management and trading.

- Consumer Banking gained 3% YoY, supported by strong card income and service charges.

- Global Wealth & Investment Management grew 8%, buoyed by a 15% rise in fees.

- Global Markets jumped 12%, with record equities trading revenue of $2.2B.

This kind of broad-based growth shows how BAC’s multi-cylinder engine can keep running — even if one piece slows.

The Dividend Triangle in Action: BAC’s Performance Map

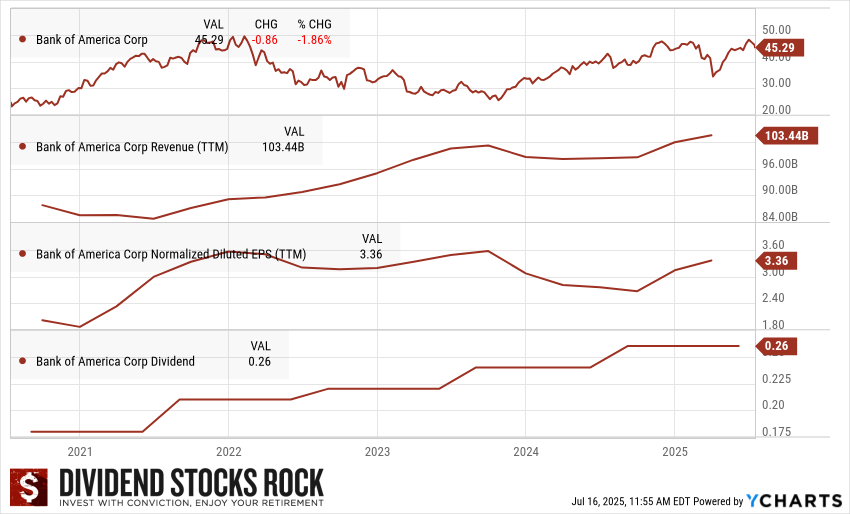

Bank of America (BAC) 5-Year Dividend Triangle.

Bank of America checks off all three elements of the Dividend Triangle — Revenue Growth, Earnings Growth, and Dividend Growth — albeit with a few caveats:

- Revenue: TTM revenue stands at $103.44B, showing solid multi-year progression.

- Earnings: EPS recovered from a dip in 2023, now reaching $3.36 TTM.

- Dividend: BAC pays a $0.26 quarterly dividend and has increased it over time, though not at a rapid pace.

The dividend isn’t flashy, but it’s backed by a mountain of cash flow. BAC’s payout ratio remains conservative, offering room for future increases — especially if rates stay firm.

Final Thoughts: Not Sexy, but Strategic

This isn’t the stock that will triple overnight. But in a world full of hype, there’s value in a stable, diversified income generator like BAC. With dependable earnings, a clear dividend strategy, and exposure to multiple growth levers, it’s the kind of stock you can quietly build a portfolio around.

More By This Author:

A Safe Place To Land: How And Where To Park Cash (Especially In Retirement)

Apple Inc.: Is The Shine Still There?

High-Yields That Won’t Let You Down

Comments

Log in or sign up to join the conversation.