Image Source: Unsplash

Walmart (WMT - Free Report) and Target (TGT - Free Report) shares lost roughly a quarter of their value in response to the disappointing April-quarter results on May 17th and 18th, 2022.

Leading up to May 2022, these two stocks had performed roughly in line with each other, with Walmart slightly doing better than Target and both outperforming in the S&P 500 index.

Target shares never got their mojo back after the May 2022 beating and have actually lost ground in response to each of the following four quarterly releases. Walmart shares have had the opposite behavior, with the stock steadily gaining ground following subsequent quarterly releases.

The performance comparison of these two stocks since the beginning of May 2022 clearly tells the story, as the chart below shows. Please note that we added the S&P 500 index to the mix (the green line) to the chart.

Image Source: Zacks Investment Research

This performance context is important to keep in mind as we look ahead to the Target and Walmart quarterly results this week, the former before the market’s open on Wednesday, August 16th, and Walmart the day after on Thursday morning (August 17th).

Walmart's quarterly EPS estimates coming into this report have been very stable, with the current Zacks Consensus of $1.67 per share unchanged over the past two months. Unlike Walmart, there has been notable pressure on Target estimates, with analysts cutting their estimates on continued near-term challenges. The current Zacks Consensus EPS for Target of $1.49 is down from $1.57 a month ago, $1.58 two months ago, and $1.94 three months back.

The stability in Walmart shares makes intuitive sense, as its core business offers a high degree of defense during periods of economic instability and uncertainty. Walmart’s ‘value orientation’ allows it to gain market share as relatively better-off consumers ‘trade down’ during times of ‘economic stress.’

One key point of differentiation between these two retail giants is Walmart’s bigger grocery business which gives its results greater stability given the ‘staply’ nature of that otherwise low-margin business. The relatively low-margin nature of groceries notwithstanding, they bring in foot traffic and are also responsible for the aforementioned ‘trade down’ phenomenon that is helping Walmart gain share.

Analysts see relatively greater momentum in Walmart’s business on the back of higher average selling prices and flat traffic, gains on the e-commerce side, and better margin results relative to what they reported last on May 18th. Target is seen as suffering from weak traffic during the period, with the price trend only marginally positive.

Both companies struggled with evolving consumer behavior as the pandemic entered the rearview mirror. We saw this in their April 2022 quarterly results that we referenced at the top of this note, for which the market punished them.

While both took drastic steps to steady their floundering ships, Walmart clearly did a better job adjusting to the new environment than Target. The ‘shrinkage’ aspect of inventory was also front and center when Target put a dollar number on the phenomenon the last time around. However, market participants appreciate that this aspect of ‘inventory shrink’ is hardly restricted to Target.

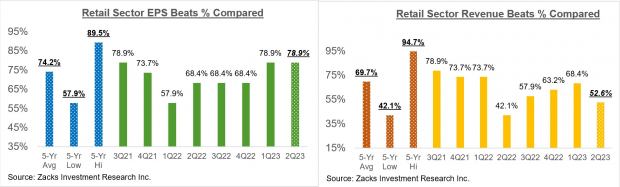

With respect to the Retail sector 2023 Q2 earnings season scorecard, we now have results from 19 of the 33 retailers in the S&P 500 index. Regular readers know that Zacks has a dedicated stand-alone economic sector for the retail space, which is unlike the placement of the realm in the Consumer Staples and Consumer Discretionary sectors in the Standard & Poor’s standard industry classification.

The Zacks Retail sector includes not only Walmart, Target, and other traditional retailers, but also online vendors like Amazon (AMZN) and restaurant players. The 19 Zacks Retail companies in the S&P 500 index that have reported Q2 results already belong to the e-commerce and restaurant industries.

Total Q2 earnings for these 19 retailers that have reported are up +49% from the same period last year on +8.3% higher revenues, with 78.9% beating EPS estimates and 52.6% beating revenue estimates.

The comparison charts below put the Q2 beats percentages for these retailers in a historical context.

Image Source: Zacks Investment Research

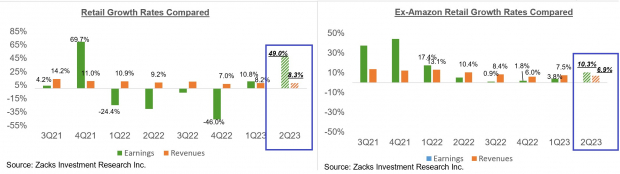

As you can see above, the online players and restaurant operators easily beat earnings expectations but struggled with beating revenue estimates.

With respect to the earnings and revenue growth rates, we like to show the group’s performance with and without Amazon, whose results are among the 19 companies that have reported already. As we know, Amazon’s Q2 earnings were up +526% on +10.8% higher revenues, beating top-and-bottom-line expectations.

As we all know, digital and brick-and-mortar operators have been converging for some time now. Amazon is now a decent-sized brick-and-mortar operator after Whole Foods, and Walmart is a growing online vendor. This long-standing trend got a huge boost from the Covid lockdowns.

The two comparison charts below show the Q2 earnings and revenue growth relative to other recent periods, both with Amazon’s results (left side chart) and without Amazon’s numbers (right side chart).

Image Source: Zacks Investment Research

One recurring theme in the Q2 earnings season has been the continued resilience and stability of the U.S. consumer. We heard this from the banks, the leisure and hospitality players, and consumer-facing digital operators.

There is undoubtedly stress at the lower end of income distribution, and one can intuitively project moderation in consumer spending as the economy further slows down under the weight of tighter monetary conditions. Inflation may be down from the multi-decade highs of a few quarters back, but it still remains a headwind, particularly for the lower end of income distribution. Other issues, like the resumption of student loan payments, are seen as weighing on spending trends. That said, the labor market remains very strong, with wages still going up.

We will hear more about that on the Walmart and Target earnings calls, likely in the context of their outlooks for the coming periods. But on the whole, consumer spending trends remained intact in 2023 Q2, and these results will reconfirm.

Q2 Earnings Scorecard

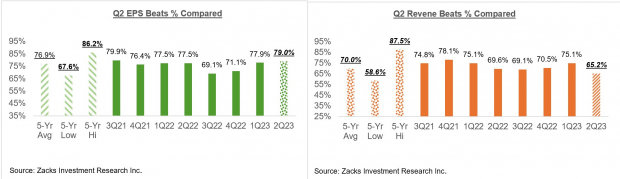

As of Friday, August 11th, we have seen Q2 results from 457 S&P 500 members, or 91.4% of the index’s total membership. The Q2 reporting cycle has now come to an end for 10 of the 16 Zacks sectors.

We have more than 300 companies reporting results this week, including 17 S&P 500 members. The notable companies reporting this week include, besides the aforementioned Walmart and Target, include Home Depot, Cisco Systems, Applied Materials, Deere & Co.

Total Q2 earnings for the 457 S&P 500 members are down -9.5% from the same period last year on +0.48% higher revenues, with 79% beating EPS estimates and 65.2% beating revenue estimates.

The comparison charts nevertheless put the Q2 results from these 457 index members with what we had seen from the same group of companies in other recent periods.

Image Source: Zacks Investment Research

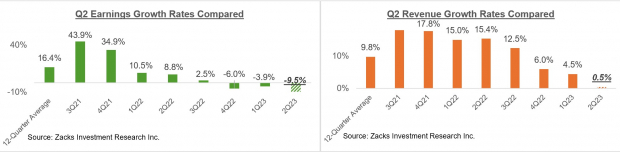

The comparison charts below put the Q2 earnings and revenue growth rates for these 457 index members in a historical context.

Image Source: Zacks Investment Research

The Earnings Big Picture

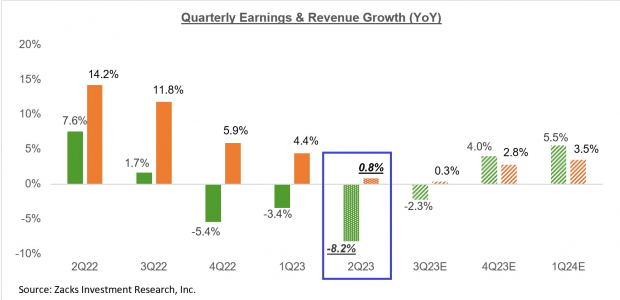

The chart below that shows current earnings and revenue growth expectations for the S&P 500 index for 2023 Q2, the following three quarters, and actual results for the preceding four quarters.

Image Source: Zacks Investment Research

Please note that the -8.2% decline for Q2 earnings on -0.2% lower revenues is the blended growth picture for the quarter, which combines the actual results that have come out with estimates for the still-to-come companies.

As you can see in this chart, Q2 is on track to be the third quarter in a row of earnings declines and the first quarter of declining revenues. As noted earlier, a big part of the earnings and revenue weakness is due to the Energy sector.

Excluding the Energy sector drag, Q2 earnings would be down -2.1% on +4.6% higher revenues.

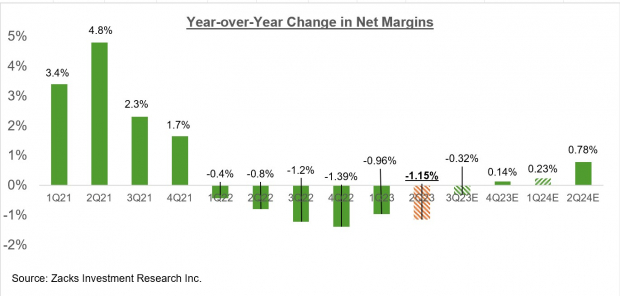

The chart below shows the year-over-year change in net income margins for the S&P 500 index.

Image Source: Zacks Investment Research

As you can see above, 2023 Q2 will be the 6th consecutive quarter of declining margins for the S&P 500 index.

Margins in Q2 are expected to be below the year-earlier level for 7 of the 16 Zacks sectors, with the biggest margin pressures expected to be in the Energy, Medical, Basic Materials, and Construction sectors.

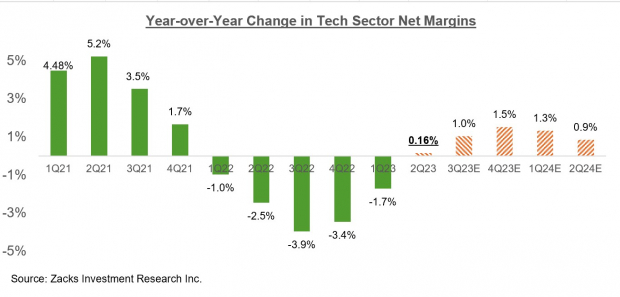

With the earnings focus lately on the Tech sector, it is instructive to see how much distance has been covered on the margins front in this key sector.

Image Source: Zacks Investment Research

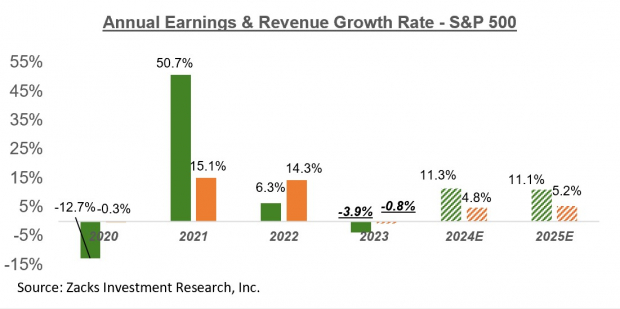

The chart below shows the earnings and revenue growth picture on an annual basis.

Image Source: Zacks Investment Research

More By This Author:

Tech Sector's Earnings Outlook Reflects Improvement

Technology Sector Market Gains Are Driven By Fundamentals

How To Make The Most Of Today's Market

Comments

Log in or sign up to join the conversation.